European Rearmament

| AUTHOR | Anushka Saxena |

| DATE | March 9, 2026 |

| DOCUMENT | Takshashila Discussion Document 2025-06 |

| VERSION | Version 1.0, March 2026 |

| CATEGORIES | Defence Indian Foreign Policy |

Executive Summary

This paper finds that:

Europe is shifting from reliance on the US to a “war economy” model. The €800 billion “ReArm” plan and “SAFE” loan programme utilise fiscal escape clauses to bypass deficit limits, effectively legalising immediate militarisation over traditional budgetary conservatism.

Strategic unity in the EU is under strain, as Poland builds a new eastern power pole through debt-funded procurement, while flagship Franco-German projects stall amid protectionist endeavours. This exposes the persistent rift between continental integration and national industrial interests.

Indian firms have opportunities to participate in EU-funded collaborative projects, especially in areas such as ammunition and artillery, small drones, cybersecurity review, and ground combat and soldier equipment. But, they can only contribute up to 35% of costs in a joint project.

Therefore, the paper recommends three important pillars for New Delhi to adopt in its approach to EU ReArm. Firstly, India must position its role in EU ReArm as a primary supplier of military consumables that it can produce at scale, while also seeking participation in restricted procurement domains by offering intra-EU production capabilities. Secondly, to address certain legitimate concerns of the EU, India must reiterate that its ties with Russia, which remain a bone of contention in India-EU ties, are purely government-to-government (G-2-G) and include some legacy military relations. In tandem, India must propose its ability to firewall EU-targeted defence exports from Russian influence, as part of a “trusted partner accreditation framework.”

1. Introduction

Europe is navigating an intense geopolitical transition – perhaps the most significant since its 1945 reconstruction. It primarily revolves around changes in the EU’s security architecture, which increasingly aims to focus on joint military mobilisation and the establishment of a continental defence industrial base. A definitive milestone in this trajectory has been the adoption of the ‘ReArm Europe/ Readiness 2030’ Plan of May 2025, which establishes the framework for a “once-in-a-generation surge” in collective defence1 capabilities. With this emphasis on rearmament, there is both an evident shift in European thinking around reliance on the United States for security and enhanced potential for collaboration with extra-regional partners, including India. Yet, measurable outcomes in terms of de-risking and self-reliance will be a long journey for the EU.

This discussion document assesses the motivations and precursors for the ReArm Europe Plan, highlighting the financial configurations of regulation and domestic policy, as well as differences in national priorities emergent since its launch. The document also assesses the case of German, French and Polish mobilisations in the process of ReArm planning. It concludes with an assessment of the potential for Indian participation in the EU’s new era of defence prioritisation.

1.1 What Motivates & Empowers Readiness 2030?

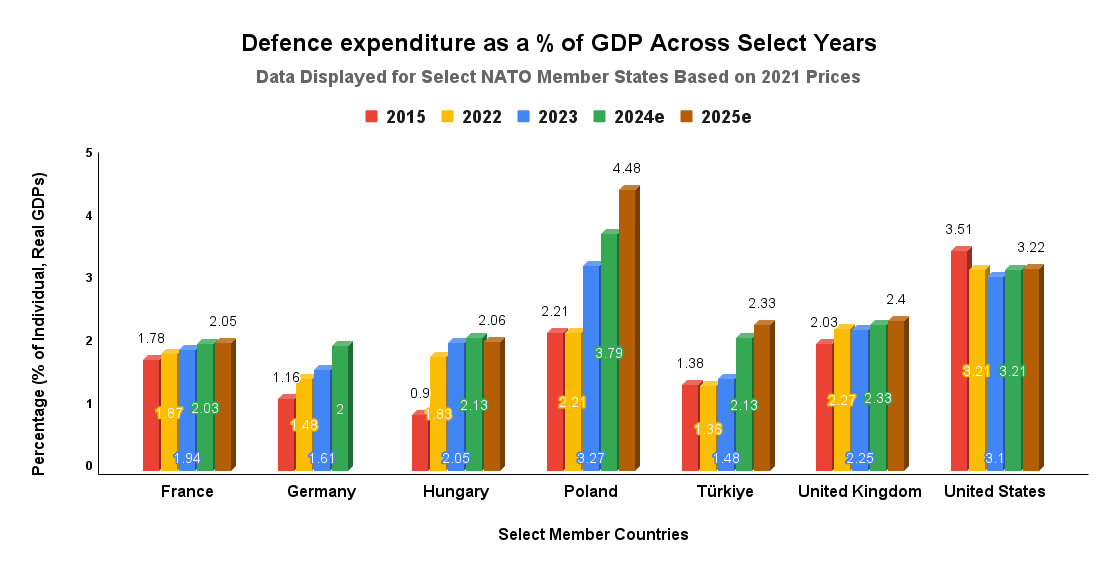

The primary motivation for the ReArm Europe Plan is a two-tiered crisis scenario. Firstly, the Plan is driven by the almost existential threat of Russian military intervention following Moscow’s full-scale invasion of Ukraine in 2022. Since the Russia-Ukraine conflict began, European intelligence agencies and analysts have increasingly warned2 that Russia may be capable of waging a conventional war against NATO members within a 3-to-5-year timeframe. This shortened horizon for a potential conflict has necessitated an immediate and massive infusion of capital to modernise3 European armed forces. It has also led certain NATO member countries to rapidly increase their defence expenditure as a percentage of their GDP (see Figure 1), to meet NATO’s 5% spending target set4 at the June 2025 Summit in The Hague. Evidently, this new limit is significantly revised upward from the initial 2% target that was formally pledged after the Russian annexation of Crimea in 2014.

Secondly, emanating from US President Donald Trump’s actions are the contours of a significant and unprecedented foreign policy in Washington. This has prompted European states to recognise that they must bear primary responsibility for their own territorial defence both in collaboration with, and outside of, the traditional NATO framework. With the threat of breakages in the transatlantic security link looming large, EU members are treating defence as a common priority.5 This involves the mobilisation of over €800 billion in public and private capital, the creation of sophisticated new financial instruments such as the Security Action for Europe (SAFE) loan programme, and a reconfiguration of the European defence technological and industrial base (EDTIB).6

The precursors to the 2025 plan were incremental but crucial in gradually establishing the EU as a self-reliant defence actor. For example, the March 2022 Versailles Summit provided the initial impetus for the politically willing. At this Summit, the Joint Communication7 concluded that EU members shall commit to increasing defence expenditures, stepping up cooperation on joint projects, and boosting innovation through civil-military “synergies.”

Initiatives preceding the Summit, such as the establishment of the European Defence Fund (EDF) in 2017 and its launch of the Multiannual Financial Framework (MAFF) 2021-2027, as well as subsequent initiatives, including the Act in Support of Ammunition Production (ASAP) in early 2023, and the European Defence Industry Reinforcement through the Common Procurement Act (EDIRPA) in September 2023, served as prototypes for joint procurement and industrial scaling.8 Most of these instruments, however, left much to be desired. For example, of the seven categories9 for which the MAFF listed commitment appropriations, defence and security was at the lowest by amount (~€13.2 billion). The EDF alone had a corpus of ~€ 8 billion.10

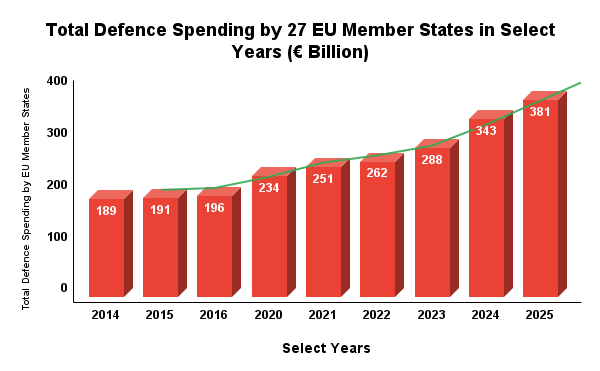

Nonetheless, the total defence spending of 27 EU Member States saw a gradual increase within the decade after the Crimean invasion – from €191 billion in 2015 to €381 billion in 2025 (see Figure 2). By early 2024, the European Commission presented the first-ever European Defence Industrial Strategy (EDIS), which moved the focus from temporary aid to Ukraine toward the long-term readiness of the European Defence Industrial Base.11 With these precursors setting the stage, Readiness 2030 took shape.

2. The Money Trail

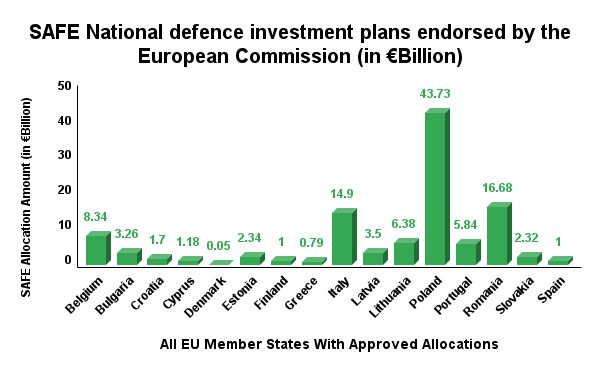

The financial cornerstone of the ReArm Europe Plan is the mobilisation of €800 billion12 through a combination of national budgetary expansions and centralised EU instruments. The most vital element of the latter is the Security Action for Europe (SAFE) instrument, proposed in March and adopted in May of 2025 as a temporary loan programme,13 providing up to €150 billion in funding to member states. Thus far, ~€ 113 billion have been approved as allocations for member states under SAFE (see Figure 3). Under this programme, the European Commission borrows from capital markets at the EU’s favourable rates – often significantly lower than the sovereign borrowing costs of states14 like Italy, Spain, or Poland – and re-lends these funds to finance common procurement of collective defence systems. While the incentive is marginal for highly rated nations like Germany and Sweden, SAFE provides some fiscal breathing room for states with higher debt-servicing costs to undertake massive modernisation programs without facing immediate sovereign debt crises.

To further expand the fiscal space, the EU has activated a ‘national escape clause’15 within the Stability and Growth Pact.16 This allows member states to increase their national defence spending by up to 1.5% of their GDP annually for four years, exempting these expenditures from the standard deficit and debt limits. This manoeuvre effectively legalises a temporary but intense militarisation of national budgets, ensuring that the pursuit of security does not trigger the EU’s excessive deficit procedures.17

To enable additional justifications, there has been a re-definition of ‘Defence’ spending under the EU Commission’s ‘Classification of the Functions of Government’ (COFOG).18 Since the March 2025 revision to the COFOG (Division 2), ‘Defence’ now includes everything from conventional procurement of weapons and the modernisation of troops to investment in dual-use civilian-sector technologies, military R&D, and even defence aid provided abroad. Additionally, the European Investment Bank (EIB) has been tasked with expanding its lending scope19 to specifically include defence and security projects, moving away from previous restrictions that prioritised environmental and social goals at the expense of military readiness.

The Classification of Functions of Government (COFOG) was developed in its current version in 1999 by the Organisation for Economic Co-operation and Development (OECD) and published by the United Nations Statistical Division as a standard classifying the purposes of government activities. The classification has three levels of detail: divisions, groups and classes. The EU has adopted COFOG for its operations, and has even published Manuals on ‘sources and methods for the compilation of COFOG statistics’ for member countries to follow, the latest of which came out in 2019. As per the 2019 Manual, there are 10 divisions in EU COFOG, on aspects such as Defence (Division 2), Public Order & Safety (Division 3), Economic Affairs (Division 4), and Social Protection (Division 10).

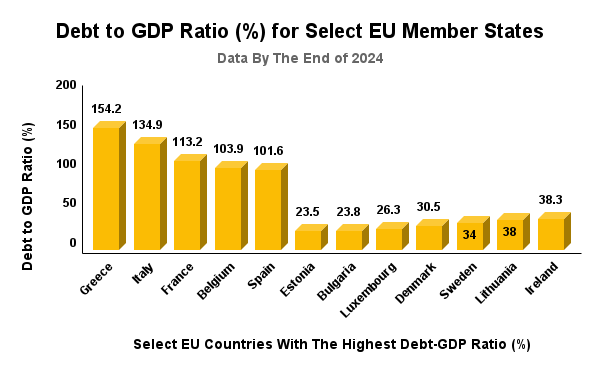

The sustainability of this funding model is a subject of intense debate. Analysts have noted,20 for example, that the efficacy of SAFE depends on stable investment demand and the creditworthiness of a handful of vital European players, such as Germany, the Netherlands, and Denmark, who collectively guarantee the EU’s AAA rating. However, as these member states themselves take on new debt to enhance domestic defence capabilities, the cost of borrowing for the entire Union may rise, potentially diminishing the public backing that makes SAFE attractive. Not to mention, even as there is a temporary surge in military spending and, to some extent, capacity, the threat of a future debt overhang21 looms large, especially for countries like Greece and Italy (see Figure 4), whose debt-to-GDP ratios are above 100%.

Bond Credit Ratings such as AAA (highest), AA (second-highest), C (lowest) are issued by credit rating agencies to describe the creditworthiness and financial stability of a country/ entity like the EU. A high rating demonstrates the bond market’s trust in the entity, allowing it to sustainably raise its debt with the belief that the entity can simultaneously also increase its resources and investment. In the case of the EU, the AAA rating, as Fitch Ratings has explained, is dependent on the ability of 5 AAA-rated Member States – Sweden, Germany, the Netherlands, Luxembourg and Denmark – to contribute more funding to the EU in case the entity finds itself unable to pay its collective debt.

It is also noteworthy that funding processes are complicated by dual-ambition, as EU Member States that are also NATO members face a diverse set of targets and regulations. NATO remains the primary organisation for operational planning and collective defence under Articles 4 and 5 of the Washington Treaty. The concept of a European pillar of NATO has emerged to connect22 the EU’s ReArm with the transatlantic link. Under this framework, EU initiatives such as the Permanent Structured Cooperation (PESCO) and the European Defence Fund (EDF) are relevant mechanisms to equip Europeans with the capabilities they need to assume a greater share of the burden within the Alliance.

Nonetheless, in the past year, in particular, with even NATO setting higher contributory expectations, burden-sharing responsibilities for members of both the EU and the Alliance have escalated significantly. Following the NATO summit in The Hague, the 5% target has sparked debate over fiscal sustainability, particularly in the eurozone. While the national escape clause provides temporary relief, the long-term requirement for such high levels of spending will necessitate23 either a fundamental revision of EU fiscal rules or the creation of permanent common funding mechanisms.

3. Continental Industrial Policy: EDIS and EDIP

The technical implementation of the rearmament plan is governed by the European Defence Industrial Strategy (EDIS) and its operational vehicle, the European Defence Industry Programme (EDIP).24 The primary objective of EDIS is to transform the EDTIB into a more resilient, competitive, and integrated market. In the past, the European defence industry has been characterised by intense fragmentation, with national governments protecting “national champions”25 and maintaining separate procurement processes. This is evident from the fact that as of 2024, 82% of funding26 for defence programmes and procurement was allocated nationally. This has led to a situation where armed forces across the EU operate a variety of incompatible systems, significantly increasing maintenance costs and reducing interoperability.27

In this regard, the primary legal tool hindering the creation of a unified European defence market is Article 346 of the Treaty on the Functioning of the European Union (TFEU). This clause allows member states to bypass EU internal market and procurement rules for “essential interests of security”28 related to arms production. Governments can invoke this article to award contracts to domestic firms, effectively fragmenting the EDTIB through protectionism.29

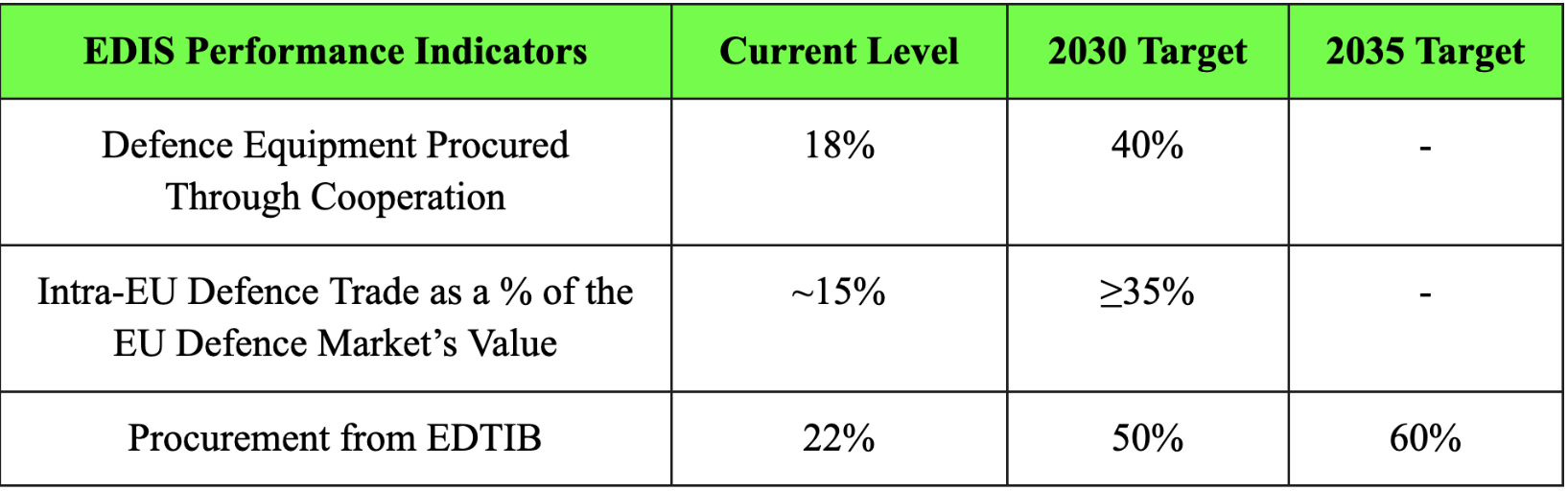

EDIS addresses some of this by setting non-binding but zealous goals, such as by 2030, at least 40% of defence equipment should be acquired jointly, and member states should aim to spend 50% of their procurement budget on European products (see Figure 5).

The EDIP framework provides the regulatory and financial incentives to reach these goals, introducing the ‘Structure for European Armament’ (SEAP)30 as a new legal framework to facilitate long-term cooperation throughout the lifecycle of defence equipment. This includes temporary VAT exemptions for common procurement contracts and streamlined procedures for certifying31 interoperable hardware. Furthermore, the ‘Defence Omnibus Simplification Proposal’ of June 2025 aims to simplify regulations and harmonise export controls, allowing companies to scale production across the single market more easily. These policies aim to move the EU toward an “intelligent European preference,” under which purchasing from non-EU providers is warranted only when domestic solutions are unavailable or cannot be delivered within the required timeframe.

The implementation of these strategies faces significant resistance from established industrial interests and national defence ministries. Analysts note,32 for example, that despite an array of new regulations, procurement may remain fundamentally nationally focused, driven by local political priorities and industrial lobbying. The switching cost of moving away from established systems – many of which are American – remains a major barrier to the adoption of common European standards. Additionally, the exclusion of key non-EU partners, such as the United Kingdom, from early versions of these programmes has been criticised as strategically shortsighted, as it forces the duplication33 of capabilities that could be shared more effectively across a broader European industrial base.

4. Case Studies: Germany’s Zeitenwende and Poland’s Tarcza Wschód

The success of the European rearmament plan ultimately depends on the fiscal and political decisions made by participating Member States. Particularly, decisions made in the political corridors of Berlin and Warsaw will likely emerge as critical drivers of land power on the continent.

Germany’s “Zeitenwende”34 has evolved from a reactive 2022 announcement into a sustained, long-term modernisation programme. On November 28, 2025, the German Bundestag approved a consolidated defence budget of €108.2 billion for FY 2026, which includes the regular Einzelplan 14 and the dedicated Special Fund (Sondervermögen). This funding is directed toward making the German Bundeswehr (armed forces) the “strongest conventional army in Europe,”35 with massive investments36 in heavy armour, integrated air and missile defence (IAMD), and cyber capabilities. A critical legislative milestone37 is the “Bundeswehr Planning and Procurement Acceleration Act” (BwPBBG), which aims to reduce the bureaucratic delays that have historically plagued German military acquisition.

In the German federal budget, Einzenplan refers to the defence budget, which includes the financing of the German Armed Forces and the Federal Ministry of Defense (BMVg). It is one of the largest departments in Berlin, and includes expenditures for personnel, operations, procurement, and research & development.

Poland, meanwhile, has emerged as the alliance’s eastern military hub, with a defence budget reaching 4.7% of GDP in 2025 (see Figure 1) and a target of 5% by 2026.38 Warsaw’s strategy is characterised by an unprecedented scale of procurement outside of traditional European channels, most notably through massive contracts with South Korea39 for K2 tanks and K9 howitzers. Poland’s “East Shield” (Tarcza Wschód) project, a €2.6 billion initiative to fortify the border with Russia and Belarus, represents its commitment to rearmament. For fulfilling such requirements, Warsaw has also received the largest allocation of SAFE financing among EU member states (see Figure 3).

Poland’s massive buildup is likely creating a new power pole in Europe, as the country’s land forces are projected40 to surpass those of Germany, France, and the UK combined by 2030. However, this rapid expansion relies heavily on debt and EU financing, including through an additional Armed Forces Support Fund, an extra-budgetary mechanism41 established to enable quick and massive procurement outside of standard fiscal constraints. Further, even though rearmament and increased defence spending themselves may be supported by Poles, they do not necessarily wish to actively engage in warfighting, as evidenced by declining support for conscription, especially among younger populations.

As per a survey conducted by Security Radar (a vertical of the German Friedrich Ebert Stiftung foundation) in 2025, 75% of the surveyed Polish population supports higher defence spending by the government. At the same time, a survey by the Polish newspaper Rzeczpospolita reveals that less than 40% of the surveyed Polish population supports mandatory conscription. The sentiment of opposition is especially high among groups that are highly likely to be called up, such as individuals in their 30s (59%) and Generation Z (58%).

4.1 FCAS and MGCS Impasse

Another area where member states may limit European defence cooperation is differences over co-production standards and requirements. A case in point is the ongoing struggles of the major Franco-German twinned weapon programme – the Future Combat Air System (FCAS) and the Main Ground Combat System (MGCS). These projects, intended to represent a major pillar of the emergent European Defence Union, have been plagued by42 disputes over workshare, intellectual property (IP), and conflicting military requirements.

By late 2025, the FCAS project, a €100 billion initiative to develop a sixth-generation fighter jet, had reached a critical impasse. France, led by Dassault, advocates43 for a model of strict leadership where the lead contractor maintains total control over subcontractors and IP, whereas Germany and its lead contractor, Airbus, seek a more collaborative model to ensure the development of their own industrial base.

Technical specifications have also created a divide. France requires44 a lighter aircraft, and one that is capable of operating from its aircraft carriers to support its nuclear warheads. Germany, on the other hand, favours45 a system with a larger airframe and a longer range without necessarily requiring aircraft carrier interoperability. Speculation46 in early 2026 suggests a potential decoupling of the project, with the three partners (France, Germany, and Spain) developing separate fighter jets while maintaining joint development of an AI Cloud47 as part of the Future Combat Air System (FCAS), as well as autonomous drone swarms.

Similarly, the MGCS tank project has stalled as German industrial strategy, recently bolstered by the national Leopard 3 programme, clashes with French logic48 regarding strategic autonomy. These difficulties underscore a fundamental dilemma, which is that while rearmament is funded at the European level, the incentive structures for industrial and economic interests remain purely national, making the compromises necessary for true integration too costly for many capitals.49

5. ReArm Creates Potential for Economic Troubles

As part of ReArm, EU member states must prepare for an intense surge in military spending to realise the goal of building a European Defence and Technological Industrial Base (EDTIB), and rely on it for continental defence. Let’s assume that the idea is for member states to reach a defence spending of 5% of GDP by 2035. Here, the SAFE financial instrument and the national escape clause – which allow member states to surge defence spending by up to 1.5% of GDP for four years without triggering the EU’s excessive debt and deficit restrictions – can provide immediate fiscal support for military modernisation.

Yet, it is important to note50 that in 2024, the EU’s total defence spending as a percentage of its GDP stood at 1.9%. On average, to even get to 5% as a bloc, the consistently required compounded annual growth rate for defence expenditure stands at ~9.87% of EU GDP. This may be doable, given that in the past FY, y-o-y growth rate has stood at ~46% (from 1.3% to 1.9% in 2023-24 period). However, a low base rate, regional differences, and dull years may lead to a lack of consistency.

Further, as many as 12 EU member states have a debt-to-GDP ratio higher than 60% (as of 2024), while the EU as a whole, too, has breached the 80% mark. Given that the SAFE programme is a loan, allocations to member states must be repaid with interest. Of course, the rates are subsidised and stand at around 3-3.3%, and the maturity can take as long as 45 years. Urgent military modernisation under these programmes, however, can create a negative debt overhang, given that it essentially borrows from future generations.

For Poland, which is on war footing and has received the highest allocation from the SAFE programme (~€ 44 billion), the rate of economic growth exceeds the rate of interest (3.2%51 real GDP growth in 2025, versus 3% expected52 interest rate for SAFE). But for economies like Italy, which has received ~€ 15 billion from SAFE, the likely interest rate far exceeds the current growth rate (0.4%53 in 2025). Even if inflation accounts for ~2% and the real SAFE interest rate stands at 1%, it may still supersede the real GDP growth rate for certain EU economies.

In this regard, the EU needs a defence partner that is not only investing a greater amount of money in its own military modernisation and defence industrial base than ever before, but that can also meet the EU’s demands as a trusted ally. India can be that partner.

6. Impact and Opportunities for India

The rearmament effort has created a historic opening for India to emerge as a critical partner in the EU’s novel security dynamics. On January 27, 2026, India and the EU signed a landmark Security and Defence Partnership54 in New Delhi, simultaneously with the conclusion of a comprehensive Free Trade Agreement. This Partnership agreement represents an important recalibration in European thinking, moving from a model of dependence on traditional suppliers to one of diversification through collaboration with capable manufacturing powers beyond the Atlantic. Driven by the need to de-risk its supply chains and address production bottlenecks, the EU is now viewing India not just as a market for arms, but as a potential manufacturing hub 55 capable of delivering defence capabilities at scale and competitive cost.

It is important to note that the key areas of cooperation listed in the EU-India Security & Defence Partnership include not just maritime, cyber and non-traditional security issues, but also defence industry-related matters, situational awareness and “exchange of information,” and training and education.

Though there is no clarity on India’s eligibility to participate in the SAFE regulation and other EU financial instruments, if such a participation indeed materialises, it would allow Indian defence firms to establish production facilities collaboratively with the EU or to engage in joint ventures with European companies, using subsidised EU funding. However, participation would be subject56 to the rule that procurement contracts must ensure no more than 35% of component costs originate from outside the EU, EEA-EFTA, or Ukraine. This could put India on par with the United Kingdom, enabling a level of industrial integration previously unavailable to non-EU nations.

6.1 Solving for the Russia Divergence

To achieve closer ties in the defence domain, a fundamental source of contention between India and the EU must be addressed. A major motivator for ReArm is Russian aggression, and Europe has legitimate concerns around India’s relations with Russia. New Delhi and Moscow remain long-standing partners in the military domain. Further, for India, it is strategically imprudent in the near term to decouple from Russia, given that 60-70% of India’s military inventory is of Russian origin. And yet, the India-EU partnership is vital enough for both sides to be able to compartmentalise.

This can be facilitated by recognising that India-Russia ties – particularly the defence relationship – largely revolve around the G-2-G vertical and the Indian Armed Forces’ legacy systems. India’s rapidly growing private defence sector, on the other hand, is largely de-linked from ties with Russia, with several of them already working with European partners. For example, major Indian companies, including57 Tata Advanced Systems, Bharat Forge, and Mahindra, are already dealing with European giants like Dassault, Airbus, and Rheinmetall. Specifically, the C-295 transport aircraft assembly line58 in Vadodara, Gujarat, established jointly by Airbus and TATA, serves as a durable production link between Indian factories and European supply chains.

The two sides can, therefore, proactively agree upon a “trusted supplier accreditation” framework, modelled on existing mechanisms. The US, for example, uses the ‘FOCI’ (Foreign Ownership, Control and Influence)59 framework to assess the extent to which firms in the American military-industrial complex (MIC) cooperate with US allies or adversaries. While FOCI legislation allows healthy investment by foreign firms in the domestic MIC, it also provides training materials to small American businesses to avoid undue influence from near-peer competitors in the space.

A similar framework for Indian private firms could include independent security audits, supply chain transparency requirements, technology transfer safeguards, and on-site rights for European inspections. The key is to make the accreditation entity-specific based on auditable evidence. The recently signed Security & Defence Partnership (SDP) between India and the EU can provide a foundation for further enhancing G-2-G trust. From India’s perspective, this approach yields the dual dividend of encouraging private participation in the defence sector and opening up export possibilities for Indian DIB products.

The trusted accreditation framework, while government-initiated, is designed to function analogously to a bilateral trade agreement or a defence acquisition procedure — once concluded between New Delhi and Brussels, its primary beneficiaries would be private sector entities. The Indian government’s role is catalytic rather than operational; it establishes the enabling architecture, after which private firms engage independently. This is precisely why the paper emphasises the G-2-G nature of India-Russia ties — the private defence sector remains largely de-linked from that relationship. The governmental incentive to facilitate this framework stems from the EU’s growing strategic salience for India, which provides sufficient political will to negotiate without necessarily implicating the Russia relationship.

6.2 At Scale

In March 2023, the EU committed to providing Ukraine with 1 million 155-mm artillery shells within a year. By March 2024, only 300,00060 of the total committed number had been supplied to Kyiv. The massive shortfall clarified that European manufacturers are scaling up, but even optimistic projections suggest that the EDTIB is not prepared for immediate mobilisation.

Further, as evident from the category 161 list of urgent procurement requirements under SAFE, the appetite for cooperation in Europe is high for lower-end capability needs, such as ammunition and unmanned systems. These are domains in which Indian manufacturing scale can mitigate the delivery delays currently facing European manufacturers. Artillery shells, tank rounds, small arms ammunition, propellants and explosives are areas Indian firms have the ability to service at scale.

From an Indian perspective, the partnership with the EU can directly complement the Indian government’s Atmanirbhar Bharat vision in several ways. First, a deep linkage to the European market can create incentives to boost India’s defence industrial scale, which can in turn help meet its own wartime needs. Additionally, partnerships with European defence firms can facilitate access to advanced European R&D and manufacturing standards for Indian entities.

In this regard, New Delhi’s pitch to Europe as a key provider of such armament must rest on three pillars. Firstly, India has existing production lines that can ramp faster than greenfield European capacity. Secondly, Indian ammunition runs at an estimated 40-60% of European unit costs. And thirdly, ammunition is a consumable, not a platform, which means that buying Indian shells doesn’t necessarily create vulnerability for Europe.

6.3 Finding Pathways for Creative Adaptations of Existing Mechanisms

To operationalise this partnership, India and the EU must chart a pathway for an agreement in which the former’s supply of defence components to the EU becomes part of the latter’s goal of ensuring that 65% of component costs in any defence venture originate from within its territorial ambit. As discussed above, the SAFE programme’s rules stipulate that only 35% of the component costs in any defence venture may originate from abroad. The remaining 65% must originate in the EU, EEU-EFTA area, or Ukraine. New Delhi could make a case for Indian suppliers to be excluded from this restriction. To this end, the above-mentioned trusted supplier/ accreditation framework can be a game-changer.

Indian defence firms could either enter into JVs with European firms and produce defence components in India, even as the products themselves could be branded European. That could effectively fulfill the 35% requirement, ensure high-quality goods for European buyers and enable joint capability development. But to also allow Indian firms to play a role in the remaining 65% of component costs reserved for the EU and Ukraine, New Delhi could enable its offshoots to operate in European economies, pay European taxes, and meet the intra-EU component of both SAFE procurement funding and EDTIB targets.

The paper’s proposal is agnostic to the specific mode of production – whether Indian-held firms manufacture EU technology within Europe, or supply indigenous products. The SAFE programme’s 35% cost threshold encompasses both manufacturing and IP costs without explicit differentiation. Hence, the recommendations in the paper are explicitly geared towards enabling Indian participation in the remaining 65% of eligible project costs, regardless of whether the contribution involves indigenous technology or EU-licensed production capabilities.

Of course, for such an ambitious proposal to materialise, the EU and India must create space for greater mutual trust at the G-2-G level. It would help if the ‘trusted partner’ framework and the 35% JVs were still in place before India could discuss participating in ReArm by being in Europe. The SDP and the India-EU FTA have opened the Overton Window, and there is solid ground for the two sides to pursue mutual benefit and closer ties by expanding their defence partnership.

7. Going forward

While the 2025 ReArm Europe Plan is a significant political signal, its long-term impact will depend62 on industrial speed and sustained political commitment. There is consensus that Europe must replace approximately63 US $1 trillion in conventional capabilities previously provided by the US to achieve true autonomous deterrence in the ‘Euro-Atlantic Theater’. This demands a structural shift in how defence ministries operate, including hiring more staff to handle larger budgets and streamlining the complex administrative procedures that currently stifle innovation.

The war economy model proposed is viewed by critics as a pragmatic but high-risk strategy. While it drives industrial growth and fulfills NATO targets, it also risks creating a new arms race and diverting resources from the long-term challenges of climate change and demographic ageing. Furthermore, the prospect of a more unified European army remains a distant goal that would require the surrender of significant national sovereignty – a step many member states are still reluctant to take.

The future of European rearmament will likely be defined by a multi-speed approach, in which a core group64 of willing states, led by Poland and Germany, drives integration, while others remain more focused on national priorities. The proposed creation of a European Defence Mechanism (EDM), an intergovernmental institution modelled on the European Stability Mechanism, could provide a more stable, long-term alternative to temporary loan schemes like SAFE. As Europe enters this era of rearmament, the goal of a true European Defence Union remains the ultimate objective, albeit one that is still being forged in the heat of an urgent security crisis and the complex politics of industrial sovereignty.

The Indo-European dimension of this strategy is expected to intensify as both sides seek to safeguard the rules-based international order. The January 2026 summit has established the political, economic, and institutional scaffolding for a defining partnership of the 21st century, potentially blending65 Europe’s technological prowess with India’s manufacturing scale and strategic location. If executed effectively, this partnership could mark the moment when India’s military-industrial complex achieves permanent integration with one of the world’s most advanced defence ecosystems, fulfilling both India’s ambition for self-reliance and Europe’s need for a resilient, diversified defence foundation.

7.1 Acknowledgements

This paper has benefitted greatly from discussions at the Takshashila Institution with Nitin Pai, Manoj Kewalramani and Pranay Kotasthane. Their ideas and research guidance are gratefully acknowledged.

Footnotes

“ReArm Europe Plan/Readiness 2030,” European Parliament, 2025. Link.↩︎

Simon Saradzhyan, “Would Russia Attack NATO and, If So, When?,” Harvard Kennedy School: Belfer Center, June 2025. Link.↩︎

Guntram B. Wolff et al., “The governance and funding of European rearmament,” Bruegel, April 2025. Link.↩︎

“Defence expenditures and NATO’s 5% commitment,” NATO, December 2025. Link.↩︎

Nicole Koenig, “From Soft Talk to Hard Power: Ten To-Dos for the European Defence Union,” Munich Security Conference, September 2024. Link.↩︎

“ReArm Europe Plan/Readiness 2030,” European Parliament, 2025. Link.↩︎

“JOINT COMMUNICATION TO THE EUROPEAN PARLIAMENT, THE EUROPEAN COUNCIL, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS on the Defence Investment Gaps Analysis and Way Forward,” EUR-Lex: European Parliament, 2022. Link.↩︎

“European defence industrial strategy,” European Parliament, March 2024. Link.↩︎

“Council Regulation (EU, Euratom) 2020/2093 of 17 December 2020 laying down the multiannual financial framework for the years 2021 to 2027,” EUR-Lex: European Parliament, 2020. Link.↩︎

“European defence industrial strategy,” European Parliament, March 2024. Link.↩︎

“ReArm Europe Plan/Readiness 2030,” European Parliament, 2025. Link.↩︎

“Proposal for a COUNCIL REGULATION establishing the Security Action for Europe (SAFE) through the reinforcement of European defence industry Instrument,” European Commission, March 2025. Link.↩︎

Guntram B. Wolff et al., “The governance and funding of European rearmament,” Bruegel, April 2025. Link.↩︎

“ReArm Europe Plan/Readiness 2030,” European Parliament, 2025. Link.↩︎

“Stability and Growth Pact,” European Commission, n.d. Link.↩︎

Aleena Im, “Europe’s Re-Armament Plan: An Emerging War Economy,” New Eastern Outlook Journal, December 2025. Link.↩︎

“Manual on sources and methods for the compilation of COFOG statistics — Classification of the Functions of Government (COFOG) — 2019 edition,” Eurostat, 2019. Link.↩︎

Alice Tidey and Marta Pacheco, “EIB spending on security and defence quadrupled to €4bn in 2025,” Euronews, January 2026. Link.↩︎

Linus Terhorst, “SAFE Alone Won’t Rearm Europe: Benefits and Challenges of the Instrument,” RUSI, June 2025. Link.↩︎

Willi Semmler and Brigitte Young, “Threats of sovereign debt overhang in the EU, the new fiscal rules and the perils of policy drift,” Economia Politica, November 2023. DOI.↩︎

Thierry Tardy, “The European pillar of NATO: What French Leadership?,” Institut Jacques Delores, January 2025. Link.↩︎

Linus Terhorst, “SAFE Alone Won’t Rearm Europe: Benefits and Challenges of the Instrument,” RUSI, June 2025. Link.↩︎

“European defence industrial strategy,” European Parliament, March 2024. Link.↩︎

Guntram B. Wolff et al., “The governance and funding of European rearmament,” Bruegel, April 2025. Link.↩︎

“European defence industrial strategy,” European Parliament, March 2024. Link.↩︎

Peter Becker and Ronja Kempin, “Strengthening Europe’s Defence Capabilities through Clear Tasks and Objectives,” SWP-Berlin, 2025. Link.↩︎

Wout de Cock et al., “Article 346(1) TFEU and Strategic Autonomy: A Possible Loophole to Grant State Aid in the Context of Geopolitical Struggles?,” Vrije Universiteit Brussel, 2023. DOI.↩︎

Guntram B. Wolff et al., “The governance and funding of European rearmament,” Bruegel, April 2025. Link.↩︎

Peter Becker and Ronja Kempin, “Strengthening Europe’s Defence Capabilities through Clear Tasks and Objectives,” SWP-Berlin, 2025. Link.↩︎

“The summary of the ReArm Europe Plan/Readiness 2030,” Bird & Bird, March 2025. Link.↩︎

“Chapter 4: Transforming European Defence Procurement and Industry,” IISS, 2025. Link.↩︎

Linus Terhorst, “SAFE Alone Won’t Rearm Europe: Benefits and Challenges of the Instrument,” RUSI, June 2025. Link.↩︎

Levente Bartha, “Germany’s Path to Kriegstüchtigkeit: The 2026 Defence Budget,” Atlas Institute for International Affairs, December 2025. Link.↩︎

“Germany wants to double its defense spending. Where should the money go?,” Atlantic Council, August 2025. Link.↩︎

Johan Holmlund, “Germany’s record defence modernisation drive (as of 22 October 2025),” Business Sweden, November 2025. Link.↩︎

Levente Bartha, “Germany’s Path to Kriegstüchtigkeit: The 2026 Defence Budget,” Atlas Institute for International Affairs, December 2025. Link.↩︎

Aldona Kowalczyk, “Polish Defence Investments – Gateway for International Contractors,” Global Law Experts, 2025. Link.↩︎

“Polish foreign minister calls for creation of “European legion”,” Notes From Poland, January 2026. Link.↩︎

“Poland becomes NATO’s eastern military hub with 5% GDP defense spending,” Yeni Şafak, January 2026. Link.↩︎

Simone Chiusa, “K2 Tank Arms Deal: Poland’s Rearmament Kicks into Overdrive,” Geopolitical Monitor, August 2025. Link.↩︎

Johanna Möhring, “Troubled Twins: The FCAS and MGCS Weapon Systems and Franco-German Co-operation,” Etudes L’Ifri, December 2023. Link.↩︎

Ulrike Franke, “The trouble with FCAS: Why Europe’s fighter jet project is not taking off,” European Council on Foreign Relations, December 2025. Link.↩︎

“FCAS fighter jet ‘very unlikely’ after ministers’ talks, source says,” Global Banking & Finance Review, December 2025. Link.↩︎

“FCAS fighter jet ‘very unlikely’ after ministers’ talks, source says,” Reuters, December 2025. Link.↩︎

Chris Lunday et al., “France and Germany’s next-generation fighter jet project is ‘dead’,” Politico, February 2026. Link.↩︎

Kjeld Neubert, “Merz expects decision on struggling FCAS jet project in ‘next few weeks’,” Euractiv, January 2026. [Link]https://www.euractiv.com/news/merz-expects-decision-on-struggling-fcas-jet-project-in-next-few-weeks/).↩︎

Fabrice Wolf, “From SCAF to MGCS, why is Franco-German industrial cooperation at an impasse?,” Meta Defense, January 2026. Link.↩︎

Ulrike Franke, “The trouble with FCAS: Why Europe’s fighter jet project is not taking off,” European Council on Foreign Relations, December 2025. Link.↩︎

“Structure of government debt,” Eurostat, December 2025. Link.↩︎

“Economic forecast for Poland,” European Commission, November 2025. Link.↩︎

Marianna Fakhurdinova et al., “Can SAFE make Ukraine safer? Insights into the new European financial instrument,” Transatlantic Dialogue Center, September 2025. Link.↩︎

“Economic forecast for Italy,” European Commission, November 2025. Link.↩︎

“Security and Defence: EU and India sign security & defence partnership,” European Union External Action, January 2026. Link.↩︎

“Guns, tech and trust: EU’s defence reset is India’s big moment,” Economic Times, January 2026. Link.↩︎

“SAFE | Security Action for Europe,” European Commission, n.d. Link.↩︎

“Guns, Trade and Trust: India, EU Head Toward Strategic Reset,” United News of India, January 2026. Link.↩︎

“Prime Minister Shri Narendra Modi and Prime Minister of Spain Mr Pedro Sanchez jointly inaugurate TATA Aircraft Complex for manufacturing C-295 aircraft in Vadodara, Gujarat,” Press Information Bureau, Government of India, October 2024. Link.↩︎

“Trainings and Educational Materials,” Office of Industrial Base Growth, US Department of War, n.d. Link (https://business.defense.gov/Resources/Training-Materials/).↩︎

“Question Time: State of Play – Ammunition Plan for Ukraine,” European Parliament, November 2023. Link.↩︎

“SAFE | Security Action for Europe,” European Commission, n.d. Link.↩︎

“Chapter 4: Transforming European Defence Procurement and Industry,” IISS, 2025. Link.↩︎

“Introduction,” IISS Strategic Dossier, September 2025. Link.↩︎

Guntram B. Wolff et al., “The governance and funding of European rearmament,” Bruegel, April 2025. Link.↩︎

“India And EU Forge Security Pact And FTA Push At Pivotal Summit, Strengthening Indo-Pacific Ties,” Indian Defense News, January 2026. Link.↩︎