Previewing China’s 15th Five-Year Plan

| AUTHOR | Amit Kumar, Manoj Kewalramani |

| DATE | March 4, 2026 |

| DOCUMENT | Takshashila Discussion Document 2026-05. |

| VERSION | Version 1.0, March 2026. |

| CATEGORIES | China Governance Economic Policy |

Executive Summary

This paper previews China’s 15th Five-Year Plan (2026-2030) based on a draft recommendations report presented by China’s central committee at the fourth plenum in October 2025, and subsequent explanations and interpretations offered by various Chinese officials. As the Chinese leadership prepares to assemble for its annual ‘Two Sessions’ where it will also adopt its 15th FYP, this paper picks the five key macroeconomic priorities outlined in the recommendations report according to us. These are: transitioning to a consumption-driven economy; tackling overcapacity and involution; proactive fiscal policy; achieving scientific and technological self-reliance; and building a modern industrialised system. It then evaluates China’s strengths and challenges relating to each of these five priorities.

The paper finds:

Consumption-driven economy: China’s stated plans to transition to a consumption-driven economy fall short. The half-hearted, lacklustre measures are unlikely to make any dent, except for episodic excitement.

Tackling Overcapacity and Involution: Beijing has assumed a more stricter stance on tackling the dual problem. The leadership’s actions lately have led to some encouraging signs, especially in the automobile sector. A reform of the Value Added Tax (VAT) structure, as allude to in the recommendations report, can have significant impact on addressing the two evils. Proactive Fiscal Policy: China’s fiscal problems are aplenty. Eleven successive quarters of deflation and subdued domestic consumption warrants a expansionary fiscal policy. However, China’s struggle with declining revenue growth and balooning debt limits Beijing’s capacity.

Achieving Scientific and Technological Self-reliance: China’s system underpinned by political and fiscal centralisation, state-guided allocation of capital, massive pool of investible capital, ability to quickly scale and early identification of emerging, strategic and future industries offers its advantage in its technological competition with the US-led West.

Building Modernised Industrial System: China is prepared to retain its current share of manufacturing as a percentage of its GDP. Chinese leadership seems committed to protecting its presence and dominance in traditional industries. While there is a focus on moving into new and emerging industries and high-tech manufacturing, the thinking is that capturing the higher end of the value chain need not come at the expense of traditional industries and lower-end manufacturing.

1. Introduction

The Chinese leadership is set to assemble for its annual ‘Two Sessions’—the gathering of its top legislature, the National People’s Congress (NPC), and the top-most political advisory body, the Chinese People’s Political Consultative Conference (CPPCC), on March 5, 2026. From an economic standpoint, this annual gathering assumes significance as the leadership announces the national GDP target for the year, alongside presenting two of the most important reports: the Government Work Report (GWR) and the Budget Execution Report.

The 2026 annual gathering is, however, important for another reason. At the NPC session, the government is slated to unveil its 15th Five-Year Plan (FYP), spanning from 2026 to 2030.

2. What is special about the 15th FYP?

The 15th FYP assumes significance in the light of China’s second centenary goal. When Xi Jinping assumed the leadership of the CPC at the 18th Party Congress in November 2012, the meeting also outlined two centenary goals. The first goal entailed building a ‘moderately prosperous society’ by 2021, the year CPC was to celebrate a hundred years of its existence. The second centenary goal involved building China into a ‘Great Modern Socialist’ country by 2049, which marks 100 years of communist rule in China.

In 2021, the leadership announced that it had successfully achieved the first centenary goal, i.e., of building a moderately prosperous society. What this implied was eliminating absolute poverty, establishing a large middle-income group, and securing basic living standards for the population. World Bank data attests that under Xi, China pulled about 100 million people out of extreme poverty—defined as people living on less than US$ 1.9 a day—thereby eradicating extreme poverty. Additionally, by 2020, the middle-class—estimated as those earning US$ 10-50 a day—constituted over 50 per cent of China’s population.

The second centenary goal, to be achieved by 2049, is still about a quarter of a century away. Yet, the 15th Five-Year Plan (FYP) spanning 2026-2030, to be adopted in a few days, assumes significance. This is because the second centenary goal involves an ‘intermediate goal’ of ‘basic socialist modernisation’ of China by 2035, a transitory stage inserted at the 19th party congress. The 15th FYP will mark the beginning of the decade that will culminate in the cut-off year of 2035 set for China’s basic socialist modernisation. The plan is expected to outline the policy direction and priorities for achieving basic socialist modernisation.

The recommendations published after the Fourth Plenum in October 2025, along with the explanation offered by Xi Jinping, provide the guiding framework for the 15th FYP. The FYP draft recommendations list pressing challenges, broad priorities for the country, directives for central and local governments, and action plans to realise major objectives, offering a sneak peek into Xi’s vision of China’s basic socialist modernisation.

3. Challenging times, but Opportunities await

In his explanatory note that was issued with the Fourth Plenum recommendations, Xi Jinping underscored that for China, the current period is one in which opportunities and risks and challenges coexist. This framing was first outlined in his speech to the 20th Party Congress. It marked a significant shift in the Chinese leadership’s assessment of the country’s development environment from the previous Party Congress. At the 19th Party Congress in 2017, Xi had assessed that China was “still in an important period of strategic opportunity for development”, despite “severe challenges.” On the international situation, Xi argued that rising geopolitical conflicts, power politics, unilateralism, hegemonism, and protectionism pose greater threats to China. More importantly, he noted that the attack on the international economic and trade order posed a grave challenge to China’s development. However, he underlined that the shift in the international balance of power, technological revolution and industrial transformation have “created positive factors enabling China to make proactive moves in the international arena and shape a favourable external environment.” On the domestic front, there was a clear acknowledgement of formidable economic challenges in the form of sluggish effective demand, rising unemployment, and stagnant income growth. This, from Xi’s perspective, underscored the significance to transition to new growth drivers.

That said, in his note, Xi acknowledged the economy’s solid foundation and resilience, certainly bolstered by China’s economic performance in the wake of rising tariffs and sanctions. He identified China’s enormous market, comprehensive industrial system, and abundant human resources as its strengths.

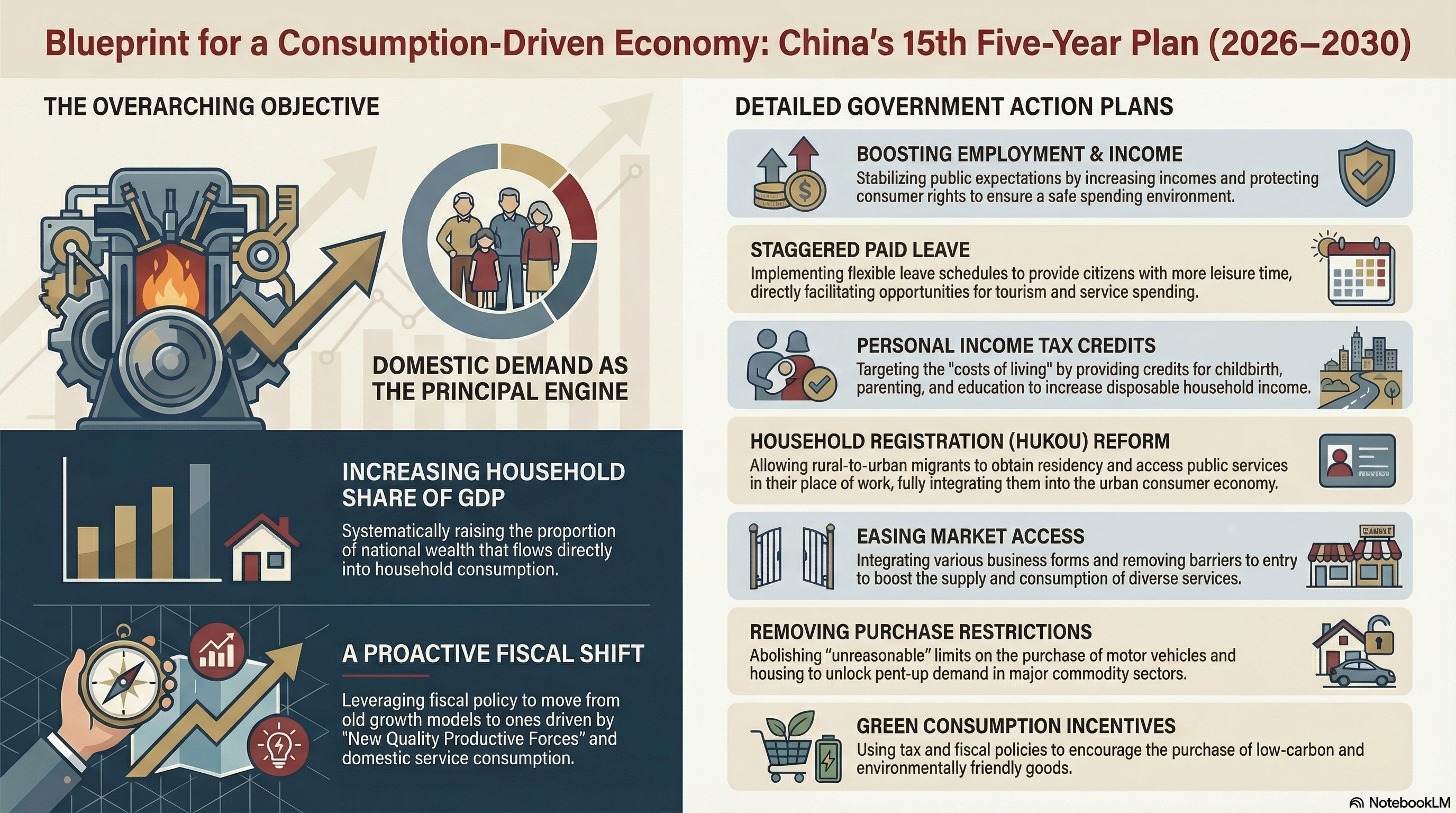

4. Consumption-driven economy

The idea of a consumption-driven economy isn’t new. The Party leadership has been reiterating the need for China’s economy to pivot towards a new development model that is centred on high-quality development. Boosting domestic demand, alongside supporting the development of new quality productive forces, is the central pillar of this philosophy.

Emphasising the need for new drivers of growth, the recommendations document sets an expectation on domestic demand to play “an increasingly greater role as the principal engine of economic growth.” It adds that the Chinese economy must achieve “a notable increase in the household consumption share of GDP.” Elaborating on the action plan, the document lists measures, such as coordinated moves to boost employment and increase incomes. Beyond these broad guidelines, however, the document does not flesh out any substantive measures, such as putting cash in the hands of people, tax cuts, and raising households’ share of income at the expense of industrial profits to raise consumption, as suggested by several economists.

4.1 Government’s Action Plan

4.2 Assessment

Despite the rhetorical call for boosting demand, several factors complicate the decision-making for Chinese leaders. In so far as welfarism and fiscal stimulus are concerned, the leadership has been averse to the idea for two reasons primarily: ideological and economic.

The Party’s ideological opposition to welfare measures to boost consumption is well known. Xi has, on several occasions, warned against welfarism breeding laziness. For instance, in August 2019, while addressing the 10th meeting of the Central Committee for Financial and Economic Affairs, Xi said:

“Even if we become more developed and financially stronger in the future, we should not set excessively high goals and provide excessive guarantees, in order not to fall into the trap of “welfarism” that encourages laziness.”

Even Chinese economists remain divided over a large-scale fiscal stimulus. Two broad camps have weighed in on the issue: pro-stimulus and anti-stimulus. Proponents of fiscal expansion argue that weak domestic demand lies at the core of China’s economic malaise. To restore growth, the leadership must adopt counter-cyclical fiscal measures, particularly direct cash transfers to households to boost consumption. They contend that stimulus should be paired with structural reforms, especially in the hukou system and pensions, to strengthen household confidence and spending power.

Opponents, meanwhile, caution against premature fiscal expansion. As economist Xu Gao notes, this camp fears exhausting policy “ammunition” and maintains that large-scale stimulus should be a last resort. In their view, the economy has not yet reached a point warranting such drastic intervention, reflecting a broader “live within your means” philosophy.

Their resistance also rests on fiscal constraints. With cumulative fiscal deficit (inclusive of all four budgets) surpassing six per cent of the GDP in 2024, Beijing’s room for manoeuvre is limited. Local governments face mounting debt and shrinking revenues, compounded by liquidity stress and a faltering property sector. Furthermore, China’s tax-to-GDP ratio has fallen from 18.5 per cent in 2014 to 14.4 per cent in 2023. A stimulus proportionate to China’s economic size could further strain macroeconomic stability.

There’s another factor that may have been inhibiting the central government’s recourse to fiscal stimulus. Beijing is locked in a geopolitical competition with the US-led West, underpinned by the race for technological superiority. The commitment to pursue scientific and technological self-reliance requires China to not only sustain existing expenditure on research and development, but also increase capital allocation towards basic research and innovation. This is especially critical given that China doesn’t have the luxury to share costs and burden as the West does with its allies and partners.

The other plausible way for China to substantially boost consumption is to elevate households’ share of income as a share of national income. Currently, enterprises in China retain a higher share of national income than the global norm. While household income has grown over the years, there are two issues of concern: One, the share of household income in national income has been declining. Two, the rate of increase in household income has failed to outpace the growth in GDP—a necessary condition to expand consumption’s share of GDP. And the government’s policy deliberately maintains this status quo to ensure higher investment in the economy.

This explains the central leadership’s half-hearted, lacklustre measures that are unlikely to make any dent, except for episodic excitement. For instance, the recommendations document calls for developing high-profile new consumption scenarios with broad appeal and creating international consumption centres and inbound consumption. The plan that seems to be on the table, as discussed above, is evidently underwhelming.

5. Overcapacity and Involution

Overcapacity and involution are both products of China’s investment-heavy approach to economic growth. Not only have they had an adverse impact on China’s domestic economy, but they have also strained Beijing’s trade relations with its major trading partners. Accordingly, addressing the twin issues emerges as major priorities for the leadership.

5.1 Government’s Action Plan

5.2 Assessment

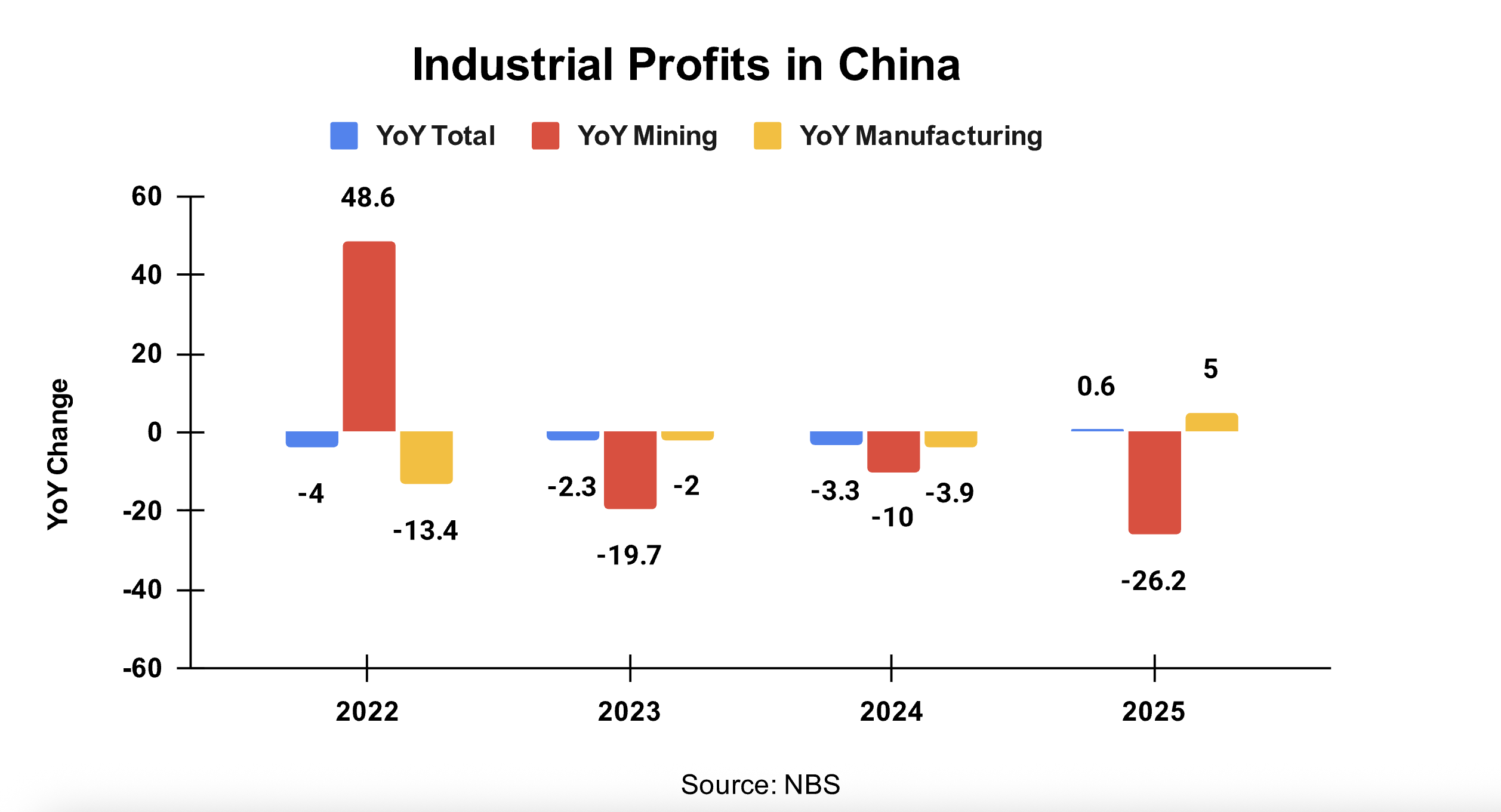

China has just recorded its longest deflationary streak in over 30 years. The last quarter of 2025 witnessed China’s 11th consecutive instance of recording a negative GDP deflator. Weak domestic demand, industrial overcapacity, and price wars emerge as key underlying causes. The fact that the economy is battling the twin problems of overcapacity and involution is evident in the downward trend in the country’s industrial profits.

To begin with, part of the solution lies in dialling back on investment that can arrest overcapacity and aligning production with overall consumption in the economy. The recommendations document, accordingly, calls for maintaining “appropriate growth in investment” and raising “returns on investment.” This is perhaps a sign of caution. There is a definite concern with respect to wasteful investment impacting the overall rate of return on growth.

For instance, to ensure effective investment, the document suggests greater coordination among all types of government investment funds. Expressing a hint of concern, it underlines that the process of government investment should be better managed.

There seems to be an acknowledgement on the part of the central leadership regarding imprudent or unwarranted investment. There is a sentiment that the national investment priorities outlined by the centre are not being communicated effectively to local governments. The document stresses the need to reform the investment review and approval system and clarify the directions and priorities of central and local government investment.

Further weighing in on the twin problems of overcapacity and involution, the leadership seems to believe that the solution lies in “eliminating bottlenecks and obstacles hindering the development of a unified national market.”

During the July 2024 Politburo meeting, the leadership referred to ‘vicious involution’ as a serious problem, for the first time at any high-level meeting. At that time, the party had instructed the industry to self-regulate and self-discipline to avoid a rat-race. The tone became serious at the annual Central Economic Work Conference (CEWC) held in December 2024. The meeting underscored the need to address “rat-race irrational competition and regulating behaviours of local governments and enterprises.” Important to note is that the central leadership held local governments equally responsible for the crisis. Soon after, in January 2025, China’s National Development and Reform Commission (NDRC) issued a guideline for building a unified national market and encouraging all localities and government departments to accelerate their integration into the unified national market. In the press conference, an NDRC official stated:

“The guideline aims to tackle these challenges by drawing firm ‘red lines’ to eliminate local protectionism, regional barriers, and unfair practices in market access, bidding and government procurement.”

The leadership views local protectionism, market segmentation and unfair competition fuelling monopolies as roadblocks in addressing involution. This sentiment was expressed in the 2025 Government Work Report, which noted:

“We will eliminate local protectionism and market segmentation, remove bottlenecks and obstacles such as those impeding economic flows in terms of market access and exit as well as allocation of production factors, and take comprehensive steps to address rat race competition.”

In July 2025, in his remarks to the Central Commission for Financial and Economic Affairs (CCFEA), Xi said:

“Efforts must be made to regulate enterprises’ disorderly price competition in accordance with laws and regulations, standardize government procurement as well as tendering and bidding processes, regulate local governments’ investment attraction practices, and facilitate sales of export-oriented products at domestic market.”

Hence, there is an inclination to “regulate the economic promotion activities of local governments” to eliminate these obstacles, which was reiterated in the 15th FYP draft recommendations. The aim is to “create a market order where good quality commands good prices and healthy competition prevails.”

One key intervention the draft recommendations report discusses, which could bear on the overcapacity problem, is to improve the taxation system. For long, China’s tax structure, especially the Value Added Tax (VAT), has been identified as a key driver of investment-heavy and production-centric policies of local governments. Given the fact that VAT—the largest source of tax revenue for local governments—is collected at the source of production, incentivises local officials to attract more enterprises, which bring revenue for them. Accordingly, the local governments’ expenditure caters to providing services to enterprises rather than on public welfare or social security measures, which, in turn, limits consumption.

Perhaps, to address the imbalance arising from the existing structure, the recommendations document stresses the need “to ensure equitable profit-sharing between places of production and consumption.” A tax reform in this regard could have a substantial impact on not only raising consumption but also checking wasteful expenditure and duplication across the country.

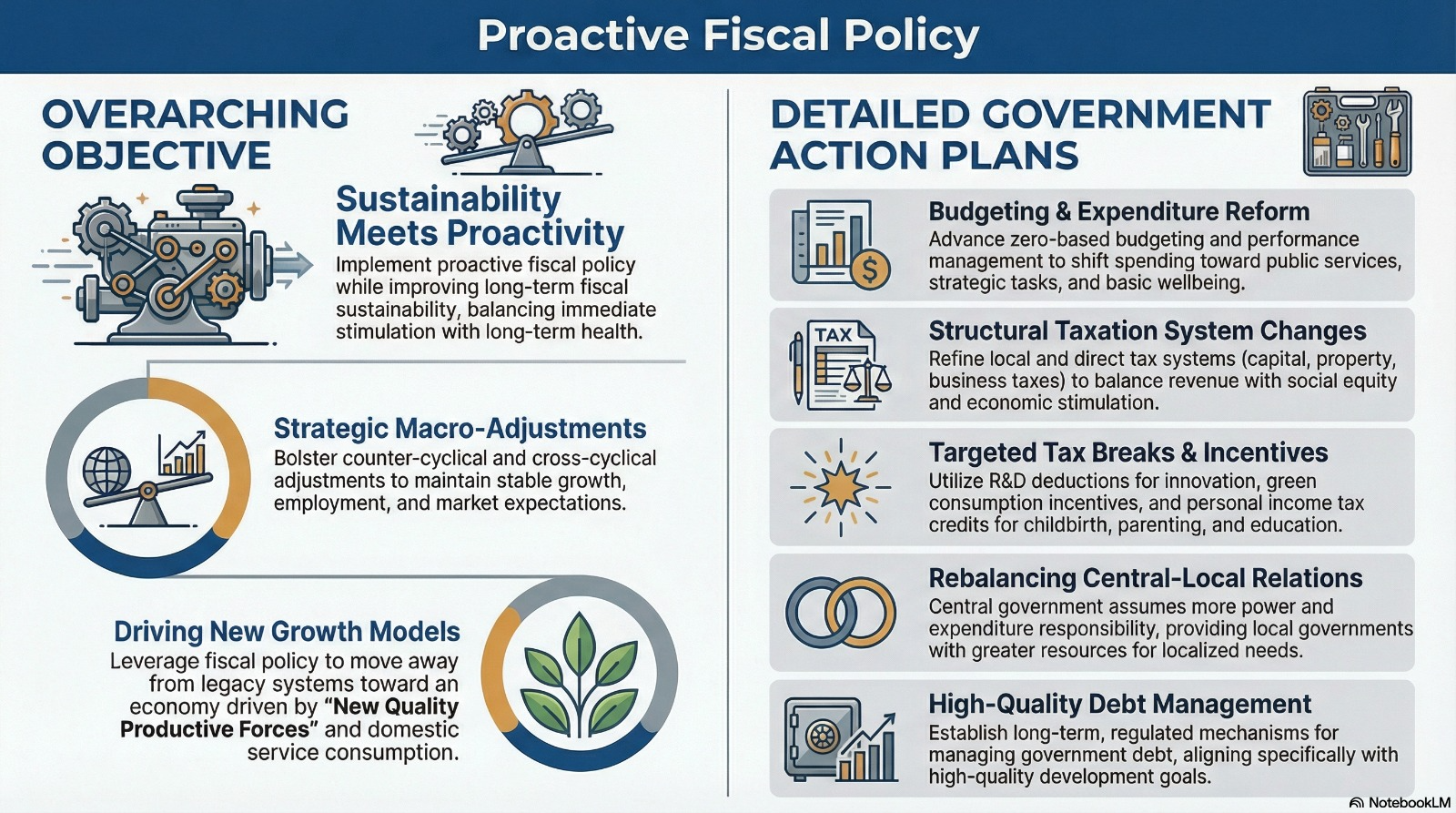

6. Proactive Fiscal Policy

China has decided to stick to a proactive fiscal policy, regarding it as vital for maintaining macroeconomic stability and improving long-term fiscal sustainability. Through the 15th Five-Year Plan, the government intends to fund major national strategic tasks, boost basic public wellbeing, and drive consumption-led economic growth. It also aims to reform budgeting, balance central-local resources, and manage debt.

6.1 Government’s Action Plan

6.2 Assessment

The recommendations document underlined that China will continue to stick to a “proactive fiscal policy in an effective manner to support the country’s high-quality development during the 15th FYP period.” While it suggests fiscal expansion, there’s also a hint of caution, reflecting China’s fiscal policy dilemma.

On one hand, China is battling 11 consecutive quarters of deflation and sluggish demand. The recommendations document underscores the need for a fiscal policy that fosters an economic model led by domestic demand and consumption and creates a self-generating momentum. China’s Finance Minister Lan Fo’an, while explaining the priorities of the 15th FYP, stated that the international environment remains challenging and the “world economy lacks growth momentum.” Therefore, the plan is to “bolster counter- and cross-cyclical adjustments and implement more proactive macro policies to keep growth, employment, and expectations stable.”

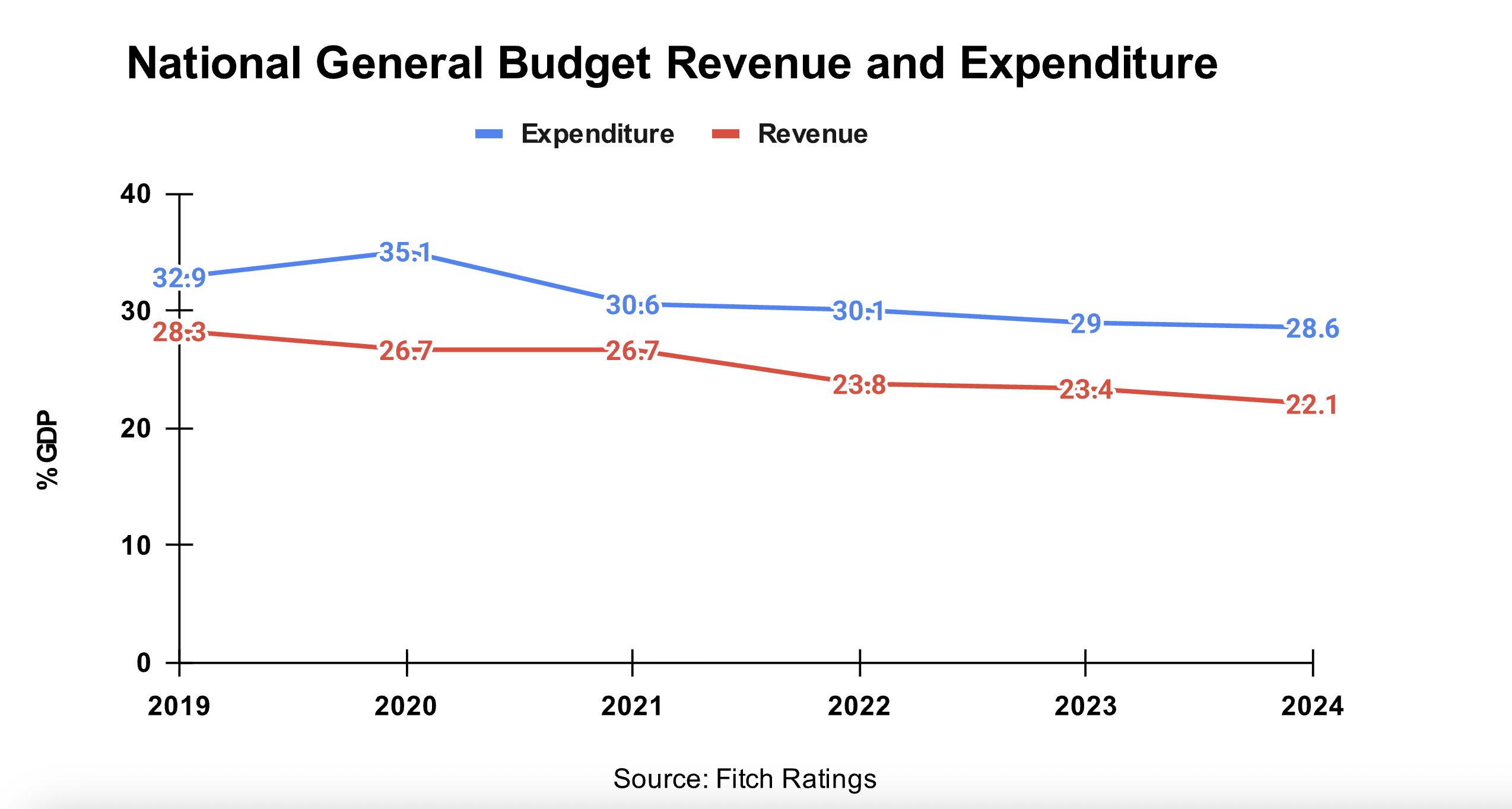

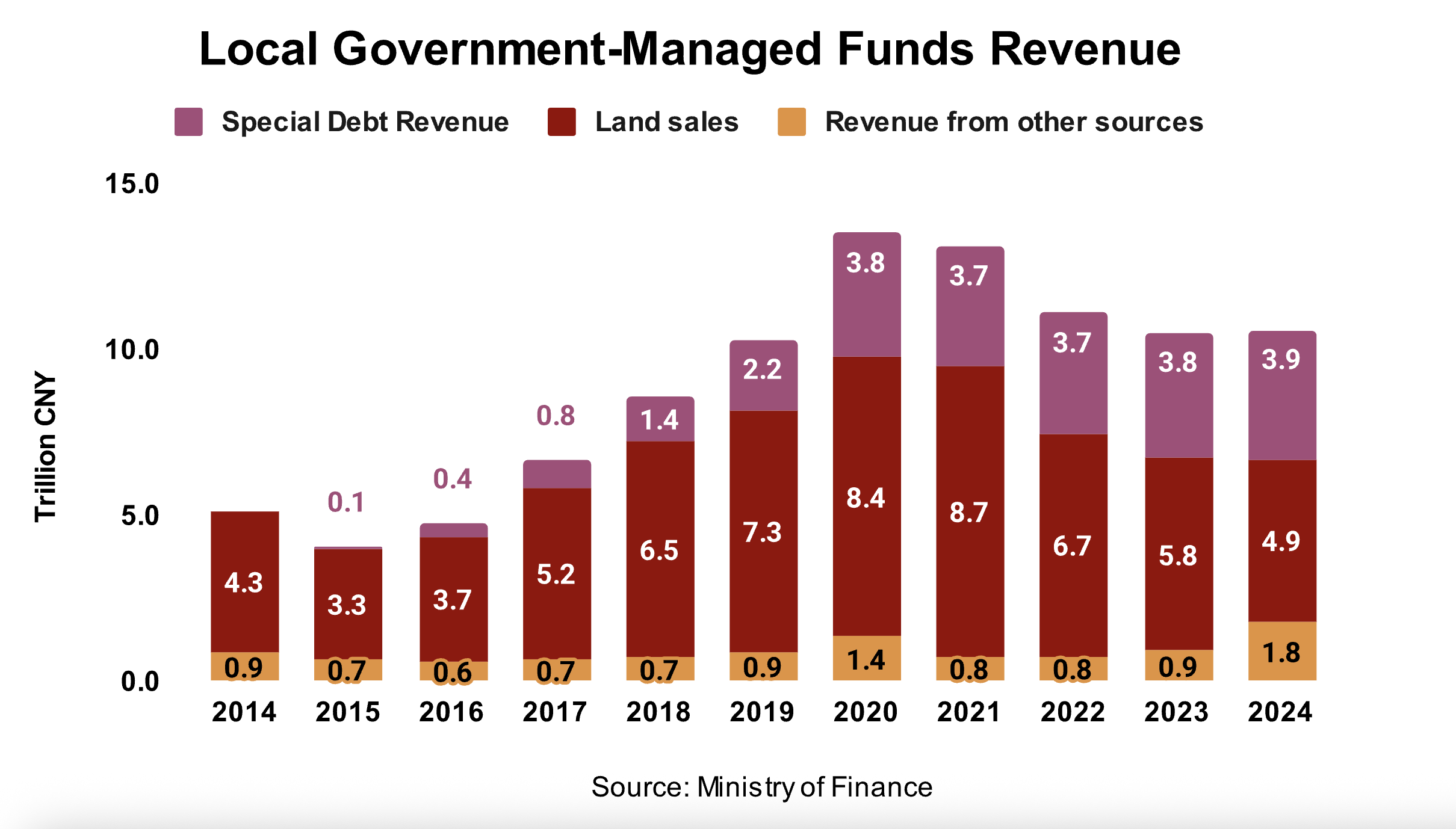

On the other hand, China’s fiscal challenges are aplenty. To begin with, its year-on-year growth in general budget revenue—the main national budget—has witnessed a declining trend over the past five years. Even the cumulative revenue from all four budgets—general budget, managed fund budget, state capital operations, and social insurance fund budget—as a percentage of GDP has consistently declined. On the contrary, the expenditure has continued to expand, exerting pressure on government coffers. Part of the reason for this is the decline in local government revenue from the sale of land use rights, which has crashed after the central government crackdown on the property sector in 2020.

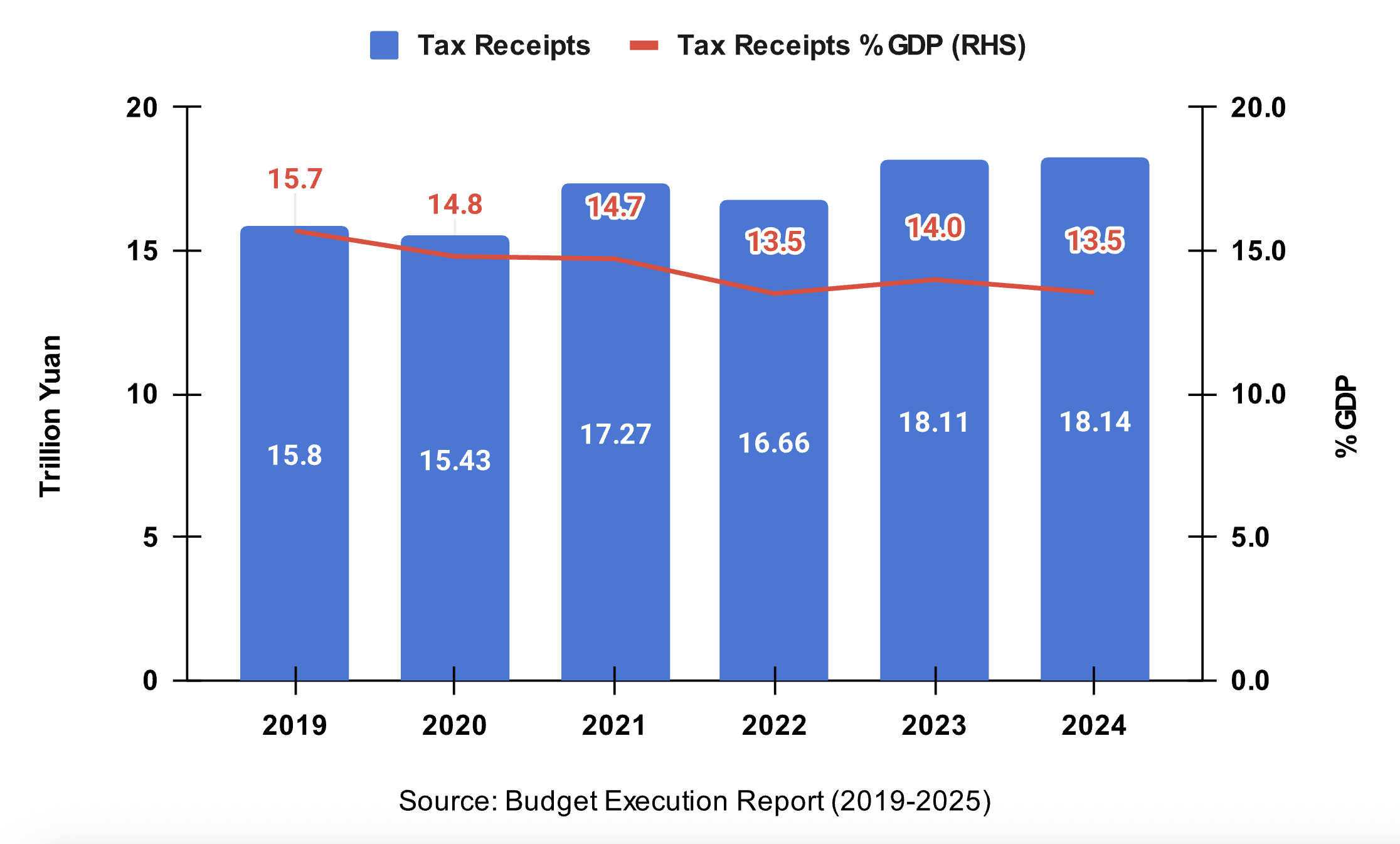

However, even more concerning is that China’s tax receipts, which do not include land-use rights sales revenue, have been declining as a percentage of GDP, too.

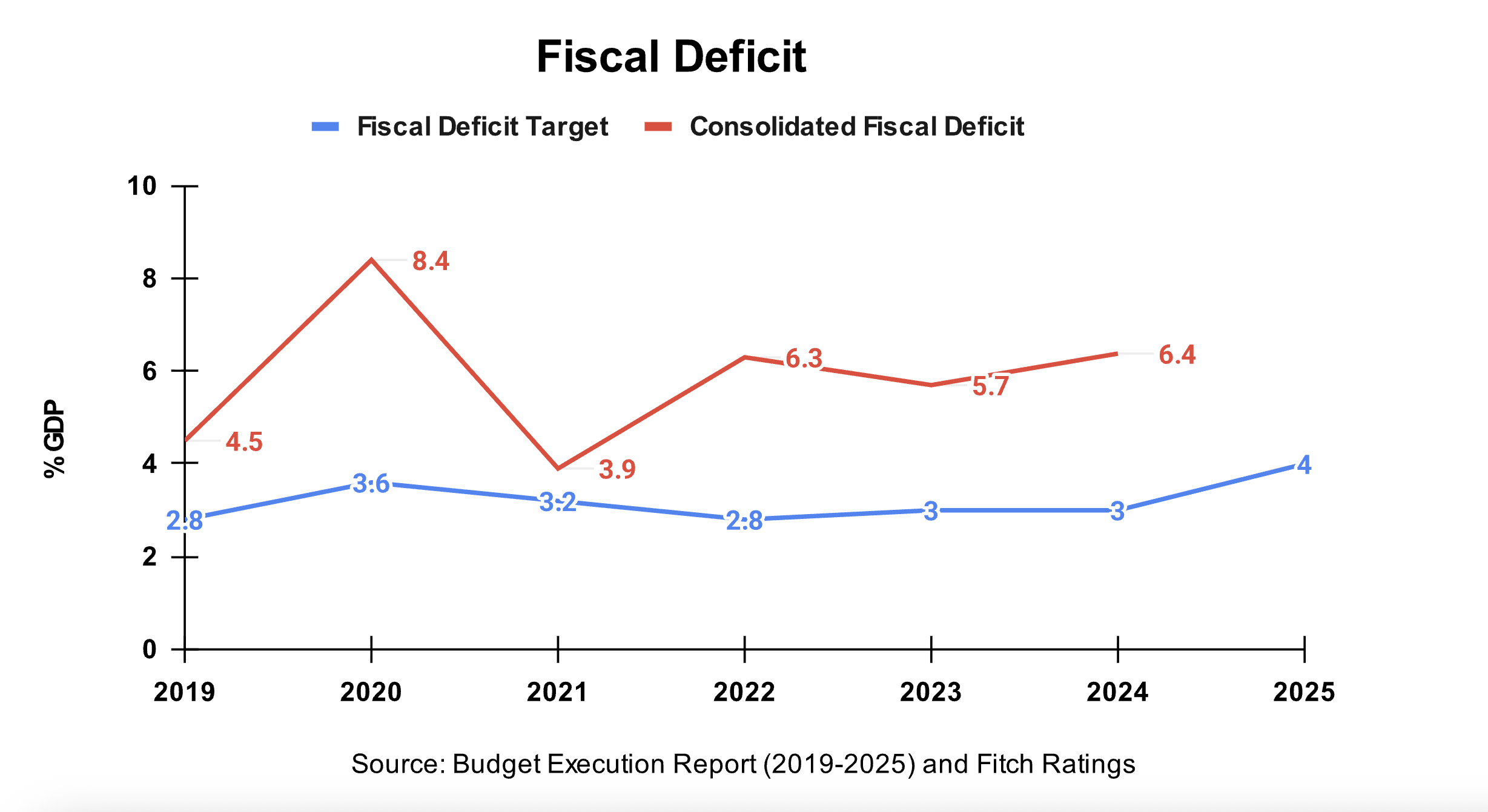

As revenue struggles to expand as a percentage of GDP, while expenditure continues to rise, the governments are forced to borrow. Consequently, China’s consolidated fiscal deficit has soared to 6.4 per cent in 2024.

China desperately needs tax receipts to increase and local government resources to expand without worsening the local government’s debt problem. Consequently, the recommendations document directs the government to keep the “overall tax burden at an appropriate level” and improve the “taxation policies on income generated from business operations, capital, and property.” Understandably, it also urges the government to better regulate tax breaks.

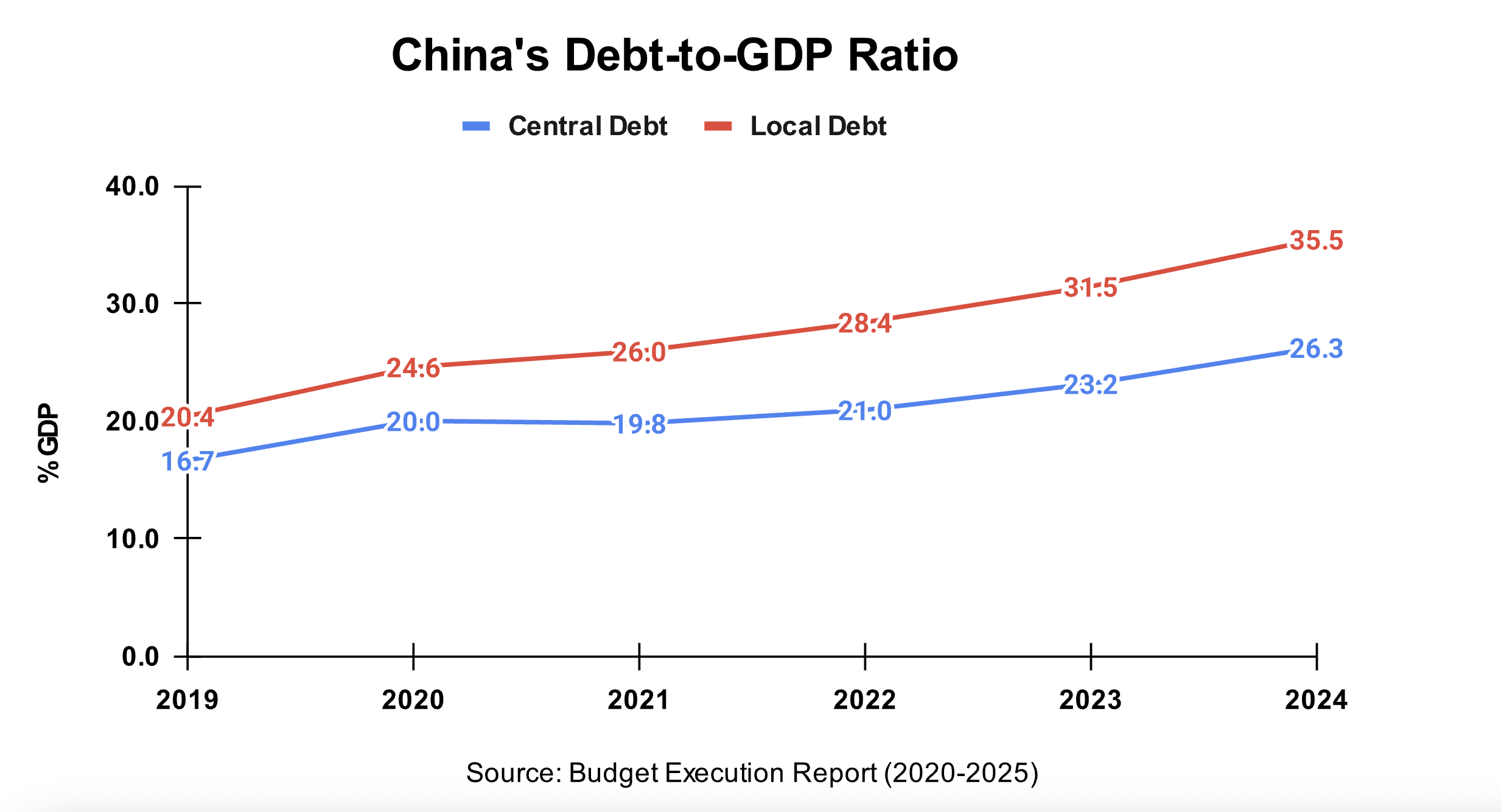

Local government debt continues to be a source of concern. The official debt may not be as big a problem, but hidden debt is. Independent studies highlight that outstanding Local Governments Financial Vehicle (LGFV) debt alone was as high as 45 per cent of the GDP by 2024.

Consequently, central government scrutiny over illegal debt and debt management will further tighten. Finance Minister Lan warned that local governments should observe the “iron discipline” of not adding any new illegal debt. Further, they should desist from repaying old loans by incurring new loans. And lastly, he stated that local governments are prohibited from establishing or creating distorted financial platforms. Accordingly, the leadership seeks to centralise more fiscal powers to exercise greater scrutiny over local finances and increase its share of expenditure.

Thus, China faces a difficult choice as it considers whether to sustain or expand the current deficit-to-GDP ratio amid limited fiscal resources. The macroeconomic situation, along with the need to invest in science and technology, requires China to pursue fiscal expansion, but its capacity to do so is constrained by dismal revenue growth and a burgeoning national debt.

The Finance Minister Lan, accordingly, underlined that the deficit-to-GDP ratio and the scale of government borrowing will be kept in line with evolving conditions. In the upcoming budget, China is likely to retain the 4 per cent fiscal deficit target.

7. Scientific and Technological Self-reliance

Self-reliance and self-strengthening in science and technology have been a recurring theme and a national project under Xi. Undoubtedly, it is one of the foundational pillars and features of China’s socialist modernisation. One can distil the goals, in this context, as follows.

7.1 Goverment’s Action Plan

7.2 Assessment

Six broad things stand out from the government’s plan. First, the mandate is to boost innovation and strengthen capacity for basic research, original innovation, and breakthroughs in core technologies. The recommendations document outlines an ambition to maintain the lead in innovation in tech domains wherever possible and to continue accelerating in other domains. To that end, it calls for mobilising resources nationwide and adopting unconventional measures to drive decisive breakthroughs in key core technologies. Beijing also plans to set up multiple major national science and technology programs to meet the country’s strategic needs. There is a lot of emphasis on “original” and “disruptive” innovation in scientific research and technological development.

Second, China will see greater devolution of funds and increased total R&D spending to support long-term and stable efforts in basic research. China’s total R&D expenditure stands at US$ 780 billion, compared to US$ 820 billion for the US. Yu Hong, Director of the Department of Finance at the Ministry of Finance, has underscored the role of government investment funds, and the National Venture Capital Guidance Fund will be leveraged to “invest early, invest small, invest for the long term, and invest in hard technology.”

Third, and perhaps the most interesting of all measures, the document recognises the roles of applications, consumers, and the market in sustaining innovation and achieving breakthroughs. The document and Xi’s note repeatedly argue that Chinese enterprises must find new consumer applications for new technological breakthroughs and innovation. For instance, the document recommends achieving full integration between technological and industrial innovation. It states that major scientific and technological advances should enter practical applications quickly and efficiently. It continues, we should build more proof-of-concept and pilot-scale testing platforms, work harder to develop application scenarios and strengthen IP rights. Insofar as the strategy to spur innovation goes, there’s hardly any fault with the strategy. What good is technology if it cannot be monetised and commercialised?

Fourth, the Chinese leadership regards enterprises as the principal drivers of technological innovation. It calls for directing resources toward enterprises to encourage them to invest in basic research. To support leading technology firms, the recommendations document proposes raising tax deductions for enterprise R&D expenses and increasing government procurement of “homegrown innovative products”. Yu reiterated that to strengthen enterprises’ principal position in scientific and technological innovation, structural tax and fee reduction policies will be implemented. Moreover, incentives and subsidies will be outlined for the development of specialised, refined, distinctive, and innovative “little giant” enterprises to support S&T innovation and manufacturing development. And finally, Yu stated that the National SME Development Fund will continue to cultivate more specialised and innovative enterprises, single-champion enterprises, gazelle enterprises, and unicorn enterprises.”

Fifth, in its pursuit of self-reliance, China doesn’t discount international exchanges and cooperation. In fact, it recommends fostering innovation by establishing “an immigration system for highly skilled personnel to attract and cultivate talent from the world.” Furthermore, it emphasises cooperation between higher education institutions, research institutions and enterprises.

Lastly, the document reiterates the importance of data as a key factor of production, besides land, labour, capital, entrepreneur, and technology. The underlying idea is that data has become indispensable in training AI models and driving digital technologies. Thus, the document calls for creating an integrated national data market that is open, shareable, and secure to allow the utilisation of data resources. While the objective with respect to AI is to achieve diffusion, there is an emphasis on gaining an edge in AI industrial applications.

However, the fundamental limit to China’s self-reliance strategy lies in the structural disadvantage of achieving solitary vertical integration. For instance, while the US-led ecosystem distributes the immense capital, talent, and technical risks of innovation across a network of high-income allies—where each may specialise in a niche technology—China faces the difficult mandate of achieving sophistication in every segment simultaneously using finite domestic resources.

Nevertheless, China’s system has certain strengths, and its centralised polity is among them. China’s highly centralised government machinery means that decisions on long-term national goals are deliberated exclusively at the central level. After clearly outlining the overarching strategic goals, the central leadership ensures strict adherence by local governments at all levels, from provinces to townships. The party-state parallel structure of governance, coupled with the underlying incentive structure for cadre promotion, allows the mobilisation of resources that is unmatched in scale anywhere else.

This political oversight has been traditionally backed by fiscal oversight, which has tightened even further under Xi. For more than 30 years, China’s central leadership has exercised tight control over the local finances. The Tax Sharing System of 1994 took away the fiscal autonomy of the local governments. Today, China’s local governments are responsible for about 85 per cent of the national general budget expenditure. But they raise only half of their total general budget expenditure. The local government’s dependence on the central government has become even more acute after the property sector crisis. This has further strengthened the central leadership’s ability to guide local governments’ investments. This top-down, centralised governance structure also combines the decentralised spirit, fuelled by competitiveness among local governments, to enable quality at scale. While this ecosystem poses challenges related to duplication and overcapacity, it also promotes process innovation.

Another strength of China is its pool of investable capital. Its underlying economic structure, which rests on an investment-heavy approach, allows China to sustain investment levels comparable to the combined investment of the US, Germany, and Japan. Furthermore, the fact that China’s system allows the state, rather than the market, to guide the flow of capital to select sectors deemed strategic can enable a focused, directed approach.

However, the danger of wasteful expenditure persists in a system where the state takes precedence over the market in allocating capital. The Chinese leadership seeks to counter it by narrowing down the scope of innovation to only such technologies that can be commercialised and find applications soon. Thus, there is tremendous emphasis from the leadership on quickly achieving commercialisation and pursuing innovation that can be applied and scaled. And the Chinese leadership believes that identifying the strategic and future industries first will give them a first-mover advantage, similar to how it unfolded for the EV, solar and battery industry.

8. Modernised Industrial System

A feature of the Chinese economy that has remained mired in controversy over the past couple of years is its manufacturing capacity and dominance in global supply chains. China, understandably, plans to double down on its strengths.

8.1 Government’s Action Plan

8.2 Assessment

China views a modernised industrial system as the material and technological foundation for Chinese socialist modernisation. A few observations stand out.

First, the Chinese leadership is committed to maintaining an appropriate share of manufacturing in the national economy. While the party has refrained from defining what this level is, currently, the share of manufacturing is 25%. One can assume that the appropriate levels will remain around this number.

Second, the Chinese leadership seems committed to protecting its presence and dominance in traditional industries. While there is a focus on moving into new and emerging industries and high-tech manufacturing, the thinking is that capturing the higher end of the value chain need not come at the expense of traditional industries and lower-end manufacturing. Accordingly, in conjunction with upgrading traditional industries, the recommendations document calls to consolidate and enhance the position and competitiveness in mining, metallurgy, the chemical industry, light industries, textiles, machinery, vessels, and construction. Hardly any major sector is excluded. It suggests that the government is committed to retaining its share in even the most traditional industries.

Third, the leadership wants China’s industrial supply chains to become increasingly “self-supporting” and “risk-resilient.” This could only mean one thing: the indigenisation of entire supply chains. This has an implication for China’s imports as well.

Fourth, the recommendations document identifies two distinct classes of industries—strategic & emerging and future industries—where China must focus. The strategic and emerging industries identified are new energy, new materials, aviation and aerospace, and the low-altitude economy. The instructions, in this context, are clear, i.e., accelerate the development of industrial clusters in these areas and achieve scale quickly. The EV industry, which was listed as a ‘strategic and emerging’ industry in the last three FYPs, has been left out for the first time in 15 years. The government plans to phase out all subsidies to the EV sector by 2027. The future industries include quantum technology, biomanufacturing, hydrogen and nuclear fusion power, brain-computer interfaces, embodied AI, and 6G mobile communications. The Chinese leadership is looking to build a first-mover advantage in these sectors. The document calls upon the government to develop venture capital investment and establish mechanisms to increase funding and share risks in future industries. The document calls for “forward-looking plans” to be put in place for them. The plan is to explore diverse technology roadmaps, typical application scenarios, and feasible business models in these sectors.

Fifth, there is an emphasis on the creation and promotion of small and medium-sized enterprises (SMEs) that rely on specialised technologies to produce novel and unique products. These SMEs, also referred to as ‘little giants’, occupy a central place in China’s efforts to promote a modern industrial system. In the 14th FYP, China planned to cultivate 10,000 of these enterprises. Available official data reveals that the centre has so far incubated more than 12,000 little giants.

Sixth, while manufacturing garners a lot of attention as China remains committed to retaining an “appropriate” share of manufacturing in the economy, the services industry isn’t neglected. The aim for the services sector is to become more specialised, digitalised and intelligentised to move up the value chain. The goal is to also integrate modern services with advanced manufacturing and modern agriculture. Perhaps the underlying thinking is that if the two industries are interlinked, they can drive each other’s growth.

Lastly, a modernised industrial system entails a modernised infrastructure system that includes ICT, computing network, S&T infrastructure, modern integrated transportation, and multimodal integration. The goal is to also develop dual-use infrastructure that can accommodate emergency needs in the city.

9. Conclusion

The five priorities outlined in the paper emerge as key economic priorities for China. How Beijing chooses to pursue these objectives will not only have an implication for its domestic economy, but also for the world economy.

Acknowledgements: The authors would like to express their sincere gratitude to Bhumika Sevkani for her research support.

10. Annexure

10.1 Government’s Action Plan on Boosting Consumption

Overarching Objective: Boosting consumption is centred on making domestic demand the principal engine of economic growth by increasing household consumption as a share of the GDP.

Increasing Spending Power & Support

- Boost employment, increase incomes, and keep expectations stable.

- Staggering paid leave to allow for more leisure and spending opportunities.

- Better protecting consumer rights and interests.

Utilising Taxation and Wealth Redistribution

- Using personal income tax credits to bring down the costs of childbirth, parenting, and education, thereby freeing up disposable income for households.

- Promoting further redistribution by means of taxation, social security, and transfer payments to steadily enlarge the middle-income group and adjust excessive incomes.

Leveraging Household Registration

- Implementing systems that allow people who move from rural areas to obtain household registration and access basic public services in their place of permanent residence, thereby integrating more residents into the urban consumer economy.

Macroeconomic and Fiscal Coordination

- Leveraging a proactive fiscal policy to create economic growth models that are led by domestic demand and driven by consumption.

- Appropriately increasing the share of fiscal expenditure that goes toward public services and basic public wellbeing initiatives to directly boost people’s purchasing power.

Expanding Supply and Upgrading Goods & Services

- Easing market access and integrating various business forms to boost the consumption of services.

- Building leading brands, raising standards, and applying new technologies to expand and upgrade the consumption of goods.

Creating New Hubs and Scenarios

- Developing a batch of high-profile, broadly appealing new consumption scenarios.

- Developing more cities into international consumption centres.

- Expanding inbound consumption from overseas visitors.

Removing Purchasing Barriers

- Abolishing unreasonable restrictions on the purchase of motor vehicles and housing.

Promoting Green Consumption

- Pursuing fiscal and tax policies to incentivise green and low-carbon consumption.

10.2 Government’s Action Plan on Tackling Overcapacity and Involution

Overarching Objective: Maintain appropriate growth in investment and raise the returns it delivers

Optimising the structure of government investment:

- Allocate a larger portion of its investment to public wellbeing initiatives, major national strategies, and bolstering security capacity in key areas.

Investing in human capital

- In response to structural demographic shifts, the government will boost investment in human resources development and well-rounded personal development, alongside improving the layouts of infrastructure and public facilities.

Reforming investment management

- Better manage the process of government investment and reform the investment review and approval system

- Clarify the specific directions and priorities for central versus local government investment.

Spurring private investment

- Improve long-term mechanisms that allow private enterprises to participate in major projects.

- Leverage the guiding role of government investment funds to spur private investment and increase its overall share.

Developing venture capital

- To support “industries of the future,” the government plans to develop venture capital investment and establish mechanisms to increase funding and share risks.

Expanding two-way international investment

- Attract foreign investment by ensuring easy market access, shortening the negative list, and facilitating reinvestments by foreign-funded enterprises.

- Effectively manage outbound investment and guide the overseas distribution of industrial chains in a rational manner.

Involution

- Regulate the economic promotion activities of local governments and “address rat race competition through holistic measures”.

- Develop a unified national market and eliminate local protectionism and market segmentation, removing barriers related to production factor access, public bidding, and government procurement.

- Enhancing efforts to tackle monopolies and unfair competition

- Create an economic order where “good quality commands good prices

- Foster healthy competition.

Dealing with Wastage

- Implementing zero-based budgeting and tightening performance-based budget management.

- Repurposing idle assets and infrastructure instead of perpetually building new projects. Improve merger, bankruptcy, and replacement policies to put underused land, idle state-owned assets, vacant housing, and idle infrastructure to better use.

- Cost-effective military spending through diligence.

- Cutting administrative waste by curbing pointless formalities

10.3 Government’s Action Plan on Proactive Fiscal Policy

Overarching Objective:

- The government plans to implement a proactive fiscal policy while focusing on improving long-term fiscal sustainability.

- Bolstering counter- and cross-cyclical adjustments to keep economic growth, expectations, and employment stable.

Budgeting and Expenditure

- Efforts will be made to advance zero-based budgeting reform, optimise spending structures, and tighten performance-based budget management.

- Appropriately increase the share of fiscal expenditure directed toward public services, major national strategic tasks, and basic public wellbeing.

Taxation System

- Introduce structural changes to the tax system to balance revenue generation, economic stimulation, and social equity

- Ensuring that the overall tax burden is kept at an appropriate level.

- Improving local and direct tax systems and refining tax policies on capital, property, and business operations.

Tax Breaks

- Tax break policies will be placed under tighter regulation.

- Utilise specific targeted incentives, such as raising the additional tax deductions for enterprises’ R&D expenses to spur innovation, and using fiscal and tax policies to drive green and low-carbon development.

- Utilise personal income tax credits to reduce the costs of childbirth, parenting, and education.

Central-Local Fiscal Relations

- The central government is to assume more fiscal powers and accordingly increase its proportion of overall expenditure.

- Place greater fiscal resources at the disposal of local governments to support their needs

Debt Management

- Establish long-term mechanisms for managing government debt in a way that aligns with high-quality development goals.

10.4 Government’s Action Plan on Achieving Scientific and Technological Self-reliance

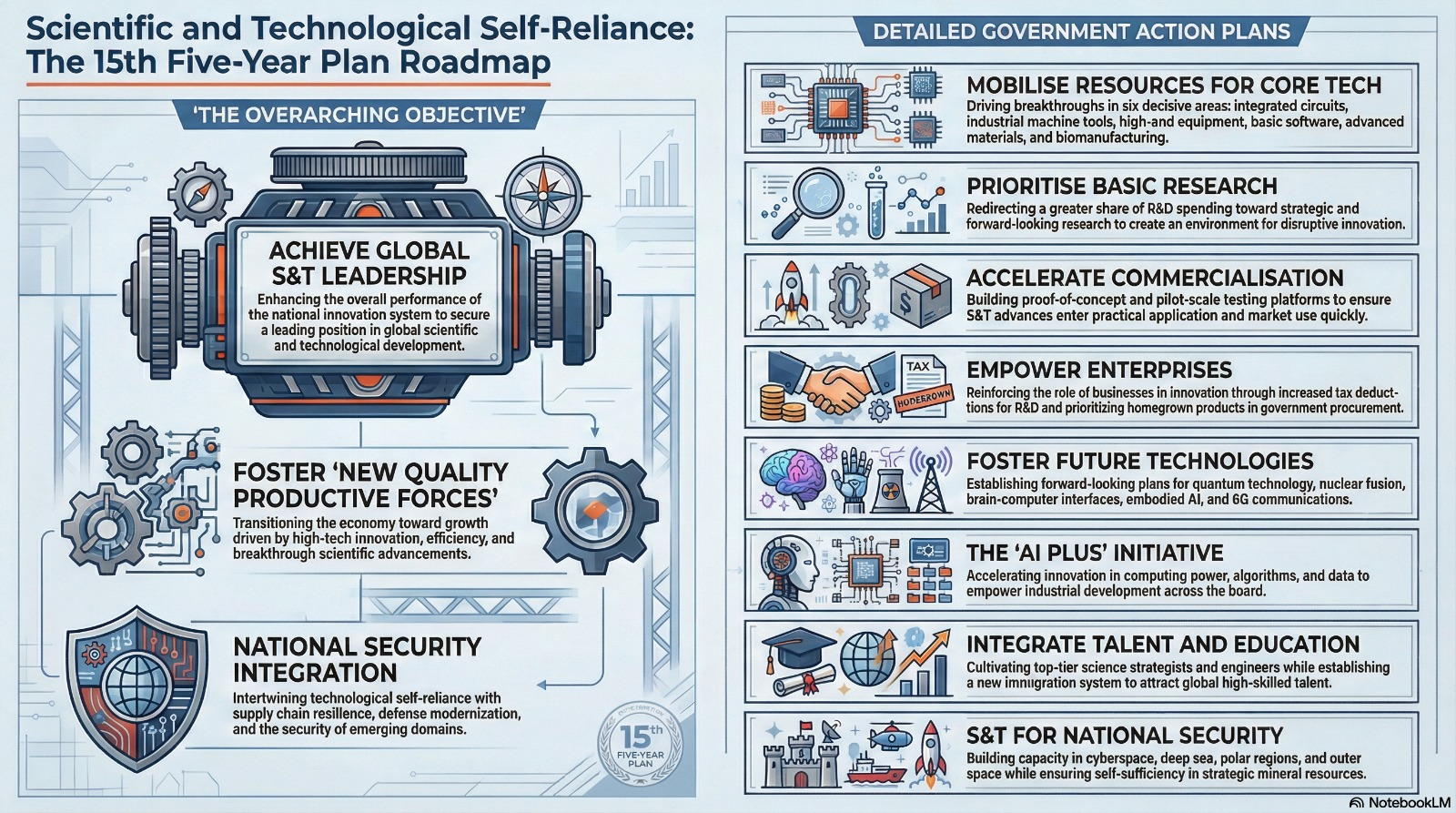

Overarching Objective: Achieve a leading position in scientific and technological development by enhancing the overall performance of China’s innovation system and fostering new quality productive forces.

Mobilising Resources for Core Tech

- Improve the “new system for mobilising resources nationwide” and adopt unconventional measures to drive decisive breakthroughs across entire chains in six core technologies—integrated circuits, industrial machine tools, high-end equipment, basic software, advanced materials, and biomanufacturing.

Prioritising Basic Research

- A greater share of total R&D spending will be directed toward basic, strategic, and forward-looking research. The plan emphasises creating an optimal environment for original and disruptive innovation.

Accelerating Commercialisation

- To ensure S&T advances enter practical application quickly and efficiently, the government plans to build more proof-of-concept and pilot-scale testing platforms, make application scenarios more accessible, and strengthen the protection and application of intellectual property rights.

Empowering Enterprises

- The principal role of enterprises in technological innovation will be reinforced.

- Raise the additional tax deductions for enterprises’ R&D expenses

- Increase government procurement of homegrown innovative products.

Fostering Future Technologies

- Forward-looking plans to be set for ‘industries of the future’ - quantum technology, hydrogen and nuclear fusion power, brain-computer interfaces, embodied AI, and 6G mobile communications.

- To establish new mechanisms for venture capital investment and risk-sharing

Advancing the Digital China and “AI Plus” Initiatives

- Accelerate innovation in digital and intelligent technologies, focusing on computing power, algorithms, and data.

- Advance AI Plus Initiative across the board and empower industrial development.

Integrating Talent and Education

- Integrated development of education, S&T, and human resources.

- Cultivating top-tier innovators, science strategists, and outstanding engineers, while establishing an immigration system for highly-skilled personnel to attract global talent.

- Reform evaluation systems to give greater weight to innovation capability and outcomes.

Scientific and Technological Self-Reliance as a National Security Priority

- Scientific and technological self-reliance is heavily intertwined with national security, supply chain resilience, and defence modernisation. The specific plans envisaged in this context include:

- Securing Emerging Domains: Building up national security capacity in emerging technological domains, including cyberspace, data, AI, biology, ecology, nuclear energy, outer space, the deep sea, the polar regions, and low-altitude airspace.

- Supply Chain Resilience: Ensuring the security and self-sufficiency of key industrial and supply chains, major infrastructure, and strategic mineral resources.

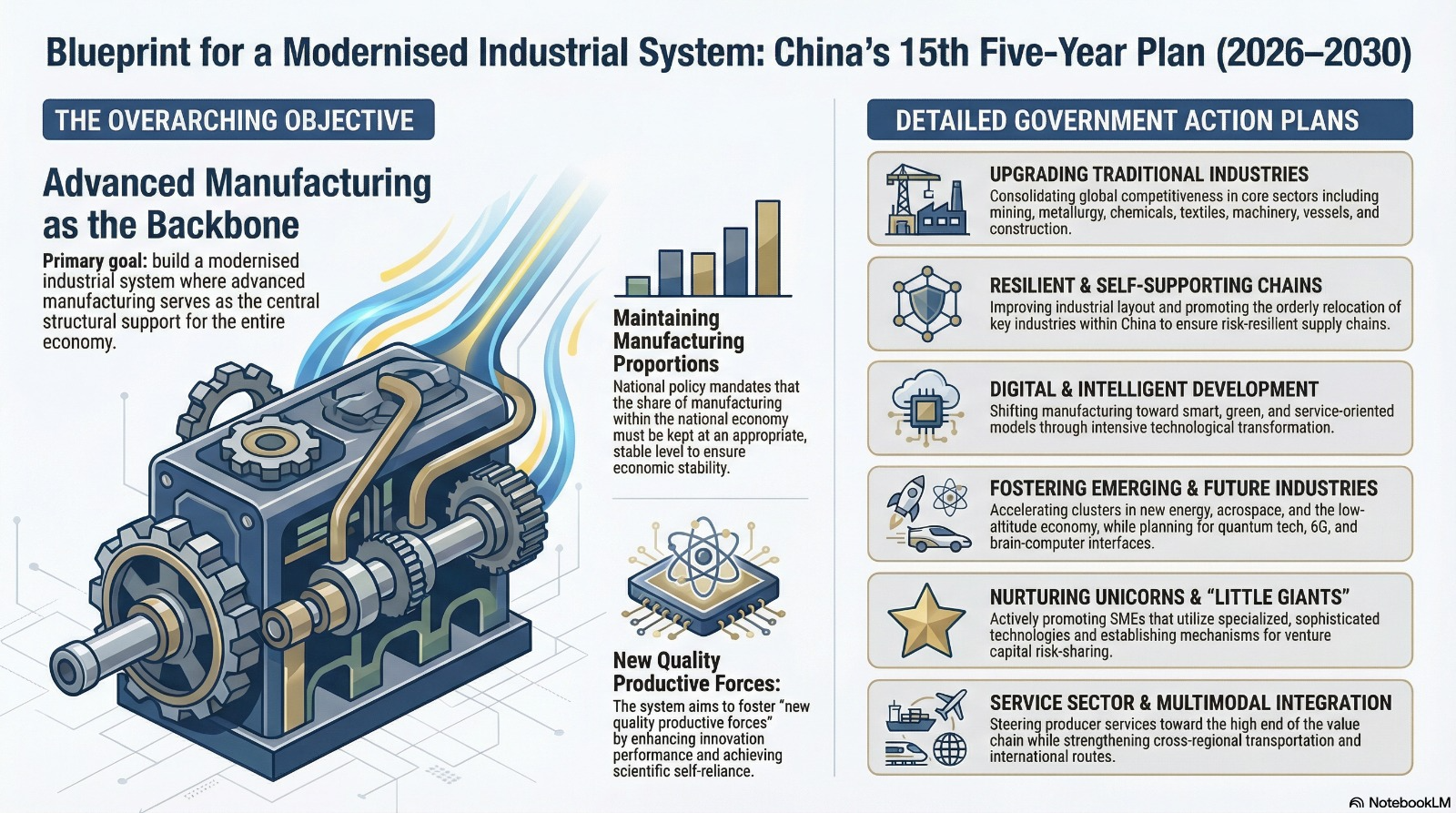

10.5 Government’s Action Plan on Building Modernised Industrial System

Overarching Objective

- Share of manufacturing in the national economy should be kept at an appropriate level

- Build a modernised industrial system with advanced manufacturing as the backbone

Upgrading Traditional Industries

- Upgrade key industries and consolidate China’s global competitiveness in mining, metallurgy, chemicals, light industries, textiles, machinery, vessels, and construction.

Self-supporting and risk-resilient industrial chains

- Improving industrial layout and promoting the orderly relocation of key industries within China

Digital and Intelligent development

- Promote technological transformation to shift the manufacturing sector toward digital and intelligent development, fostering smart, green, and service-oriented manufacturing models

Fostering Emerging and Future Industries

- Accelerate the development of industrial clusters in strategic and emerging industries such as new energy, new materials, aviation and aerospace, and the low-altitude economy.

- Forward-looking plans to be set for ‘industries of the future’ - quantum technology, hydrogen and nuclear fusion power, brain-computer interfaces, embodied AI, and 6G mobile communications.

- Establish new mechanisms for venture capital investment and risk-sharing

Unicorn and Little Giants

- Promote the growth of small and medium-sized enterprises (SMEs) that use specialised and sophisticated technologies, and actively nurture unicorn companies.

Developing the Service Sector

- Capacity and quality upgrades of the service sector by opening it to wider, deepening regulatory reform, and refining support policies to create quality market entities.

- Steering producer services toward greater specialisation and the higher end of the value chain

Multimodal Integration

- Integrate the transportation system and strengthen cross-regional coordination, promoting multimodal integration, and enhancing links in remote areas and international routes.

Optimise Energy Layout

Modern water network

- To enhance flood prevention, water resource allocation, and urban/rural water supply

Dual-use Public infrastructure

- To accommodate emergency needs in cities