Proposal for a Right-Based Seaweed Cultivation System in India

Authors

Executive Summary

India has progressed from treating seaweed as a niche livelihood activity to recognising it as part of coastal aquaculture. India’s BioE3 policy recognises seaweed as an important activity of the bioeconomy, with the Coastal Aquaculture Authority (CAA) legalising the cultivation of seaweed in India’s territorial waters. But the sector still lacks the one instrument that would unlock farmer finance and private investment at scale: a secure, exclusive, bankable lease over a defined marine area. This advisory recommends that India shift from a registration-only recognition of seaweed farming to a lease-based tenure framework for seaweed cultivation sites, administered through the CAA in collaboration with state governments and accounting for strong environmental safeguards.

Devleena Bhattacharjee is the founder of ClimaCrew. Shambhavi Naik is the chairperson of the Advanced Biology programme at the Takshashila Institution. Anupam Manur is a professor of Economics at the Takshashila Institution.

Acknowledgements The authors are thankful to Anisree Suresh for her help in the document preparation. The authors would also like to thank Nelson Vadassery, Abhiram Seth, Tanmaye Seth, Kapildev Bahl, and Swapnil Tandel for their thoughtful comments on the recommendations advanced in this paper.

Introduction

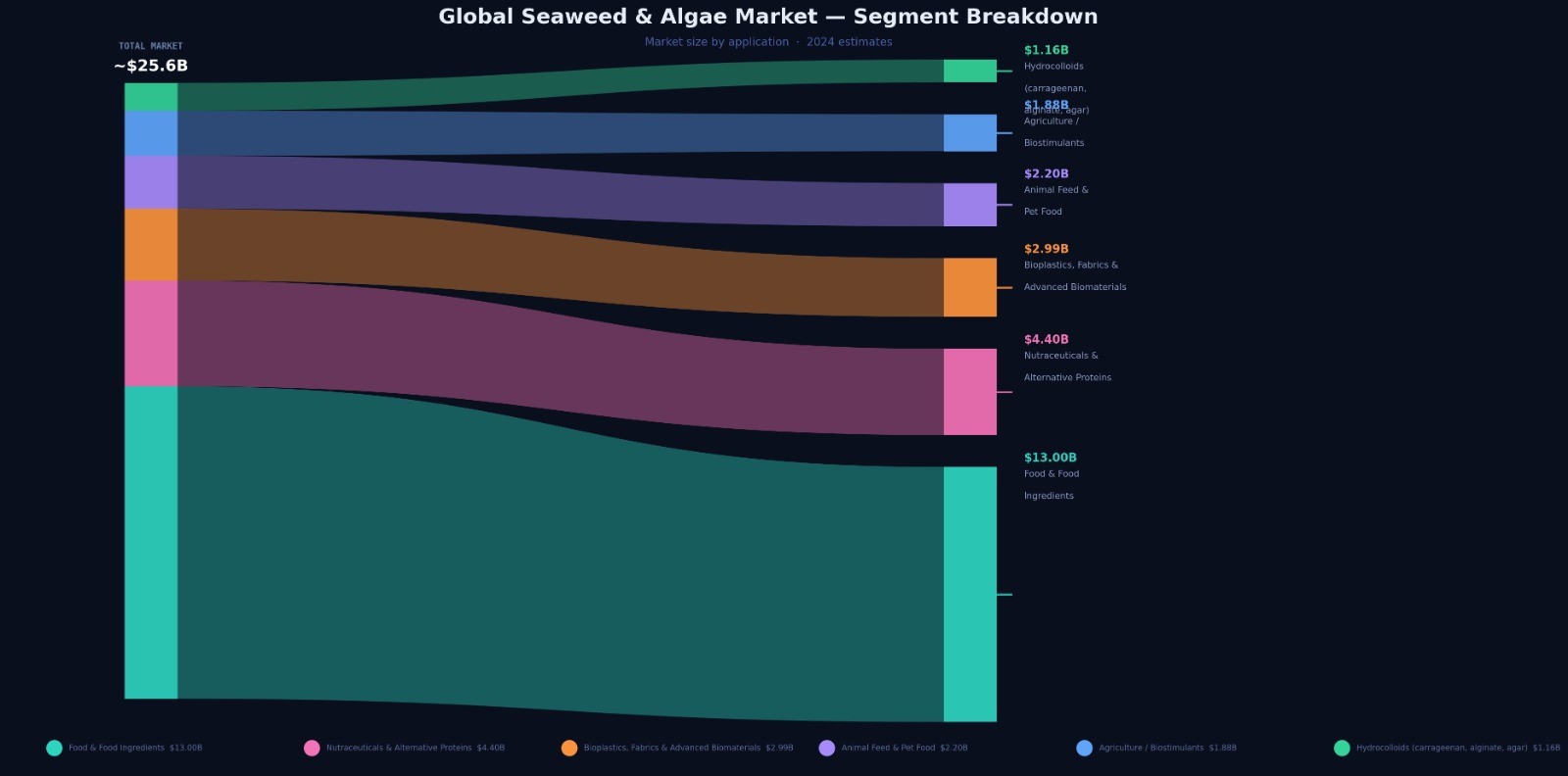

Seaweed is no longer only a coastal livelihood issue. It sits at the intersection of industrial biotechnology, climate strategy, coastal development, and import substitution. Global seaweed cultivation has expanded dramatically over the past two decades, with production increasing from roughly 11 million tonnes in 2000 to 35.2 million tonnes in 2021.1 Over the same period, the market value of the seaweed industry grew from around USD 5 billion to USD 17 billion. Forecasts suggest the industry could reach USD 97 billion by 2027.2 Seaweed-based value chains now supply food, hydrocolloids, pharmaceuticals, cosmetics, feed, and agricultural biostimulants (Figure 1). Hydrocolloids such as carrageenan, agar, and alginate are particularly important because they are basic inputs into food processing, pharmaceuticals, and industrial applications.

The primary focus currently in India is cultivating Kappaphycus alvarezii, a red algae species that produces carrageenan, a commercially important polysaccharide and bio-stimulant.3 For India, the case for investment in seaweed rests on four grounds.

First, jobs and livelihoods. Commercial farming of Kappaphycus alvarezii has already shown that seaweed can generate substantial employment and cash income in coastal communities. The government estimates utilising 24,707 hectares for seaweed cultivation. Under optimal conditions, the net revenue from one hectare (400 rafts) in dry weight might reach up to Rs. 13,28,000 per year. A family of two can handle around 45 rafts, providing income opportunities.4 If the complete potential estimated by the government is realised, it can directly result in the creation of about 4.4 lakh jobs using the raft method. The actual numbers will differ from state to state: in Tamil Nadu, for example, since its shallow waters near Mandappam allow most of the cultivation to be done by walking into water, there is no need for boats or anchors, and the number of rafts that can be managed per person is high.

The employment opportunities extend beyond cultivation and are also generated at downstream activities in the supply chain, such as processing, packaging and shipping. Even a conservative multiplier of 0.3 to 0.5 would imply that an additional 1.3 to 2.2 lakh jobs would be generated. Furthermore, several case studies in the region have demonstrated that the seaweed sector may drive women’s empowerment in ocean communities.5

Second, industrial and import resilience. India’s seaweed value chain can reduce dependence on imported hydrocolloids and raw materials for food, cosmetics, agriculture and biotech applications. According to trade data, India imported about USD 2.9 million worth of seaweed in 2020, while seaweed-related exports were only about USD 773,000.6 Trade data from 2018 showed an import of approximately 252,000 kg (approximately 252 tonnes) of seaweed.7

Third, revenue and rural enterprise. NITI Aayog’s seaweed strategy estimates that bringing 24,707 hectares under cultivation could enable production of roughly 7.51 lakh tonnes of Kappaphycus alvarezii or 28.1 lakh tonnes of Gracilaria edulis, with a revenue potential of more than Rs 50 billion for either species.8

Fourth, climate and sustainability. Seaweed farming does not require arable land or freshwater, can complement coastal livelihoods, and has carbon uptake potential. Mariculture seaweeds’ estimated carbon sequestration rates amount to 57.64 tonnes CO2 per hectare per year, while pond-cultured seaweeds sequester 12.38 tonnes CO2 per hectare per year. Kappaphycus alvarezii has been estimated to sequester 19 kg of CO2 per day per tonne of dry weight, or equivalently 760 kg of CO2 per day per tonne of dry weight per hectare.9 While claims around carbon removal should be made cautiously, Indian technical literature does indicate significant CO2 sequestration potential in cultivated seaweed systems, including Kappaphycus alvarezii.

India’s Seaweed Cultivation and Governance Landscape

The Department of Fisheries has made seaweed a priority activity under the Pradhan Mantri Matsya Sampada Yojana, approved about Rs 197 crore worth of seaweed-related projects during 2020–25, supported a Multipurpose Seaweed Park in Tamil Nadu with an approved investment of Rs 127 crore, designated Lakshadweep as a Seaweed Cluster, and notified the Mandapam Regional Centre of ICAR-CMFRI as a Centre of Excellence.10,11 The government has also issued germplasm import guidelines and set up inter-ministerial and technical coordination mechanisms. In response to these incentives, seaweed production has increased from 18,890 tonnes in 2015 to 74,083 tonnes in 2024.12

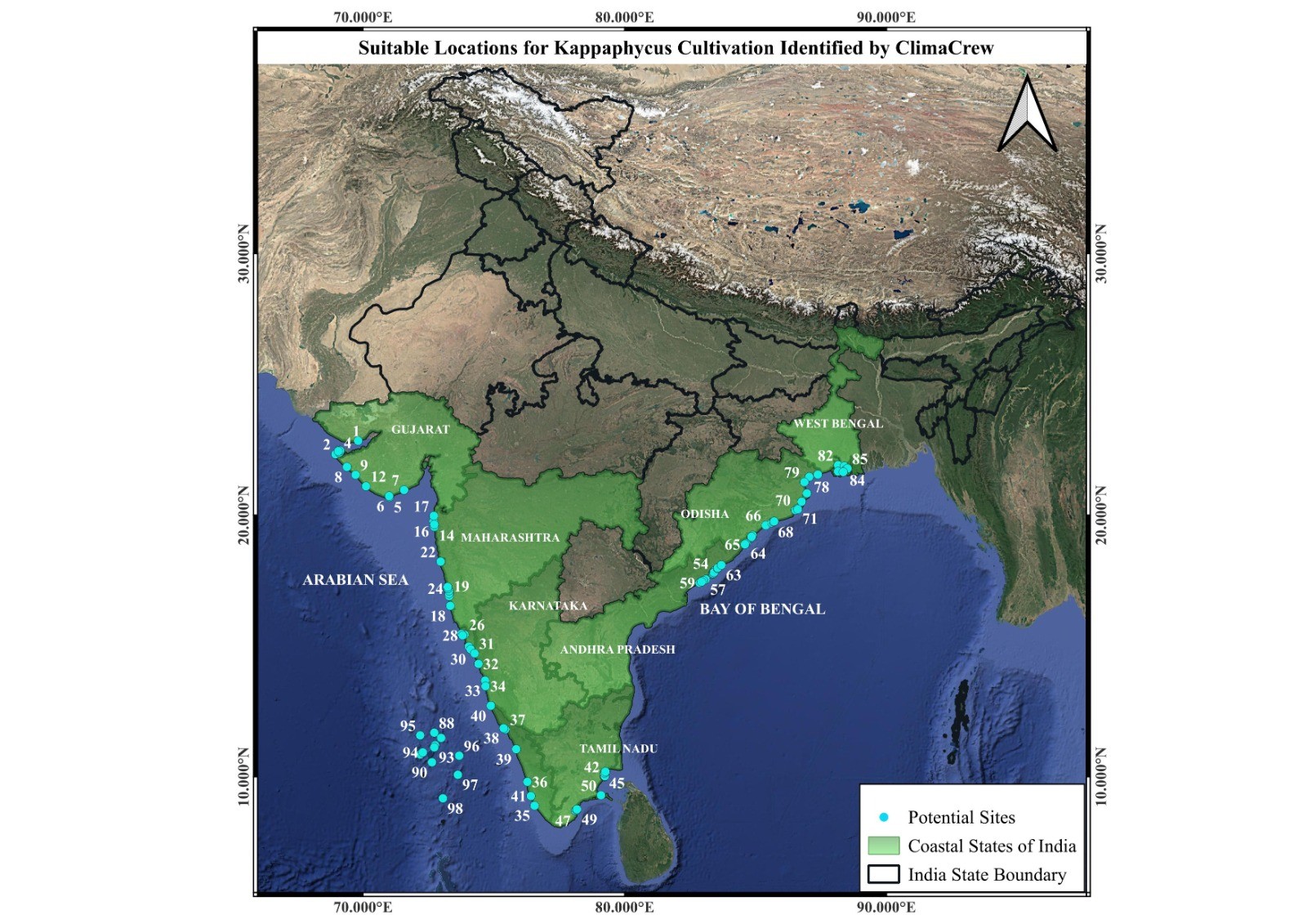

Research institutions, including ICAR - Central Marine Fisheries Research Institute (CMFRI) and CSIR - Central Salt and Marine Chemicals Research Institute (CSMCRI) have identified 384 sites across the coastline covering 24,707 hectares as suitable for seaweed cultivation (Appendix II).13 Gujarat, Tamil Nadu, Maharashtra, Odisha, Andhra Pradesh and island territories together provide a broad national base rather than a single-state opportunity.

Yet India’s seaweed economy remains well below its potential. Recent policy reforms have eased restrictions on the import and cultivation of seaweed and provided financial support through government grants and targeted programmes. While these measures have helped catalyse pilot projects and early adoption, they are insufficient to drive large-scale expansion of the sector. For seaweed cultivation to grow meaningfully, the industry will need to attract private investment. This, in turn, requires the creation of bankable and secure rights over cultivation areas that farmers and enterprises can use to raise capital, invest in infrastructure, and scale production.

The next section argues that the absence of a clear legal framework that makes seaweed cultivation a fungible and financeable asset is likely preventing its wider integration into coastal economic activities.

The Policy Gap: Legal Recognition without Bankability

The amendments to the Coastal Aquaculture Authority Act (CAA) in 2023 brought seaweed explicitly into the statutory definition of “coastal aquaculture” and “farm.” The amended law now covers the cultivation of seaweed in saline or brackish coastal areas under controlled conditions via a registration process.

The registration allows the farmer to grow seaweed legally through a regulated approval process. However, it does not ensure exclusive possession of a defined patch of ocean, the ability to exclude encroachers, or the ability to offer the cultivation right as collateral to a lender. For seaweed, where the productive asset is not merely the raft or line but the site itself, the ambiguity of property rights associated with the cultivation site may be commercially crippling.

Another area of coastal aquaculture where a regulatory framework has successfully supported industry development is shrimp farming. The CAA’s shrimp guidelines helped formalise the sector by making farm registration mandatory and establishing a compliance architecture covering farms, hatcheries, and input suppliers. However, shrimp farming typically takes place in ponds or on land. Farmers usually already control the underlying parcel through ownership or a land lease. Registration, therefore, operates on top of an existing tenure base.

Seaweed cultivation, by contrast, lacks such a foundation. Farmers operating in open waters may own cultivation equipment such as rafts, ropes, and seedlings, but they do not possess secure rights over the water surface where cultivation takes place. These coastal waters are often shared spaces used by multiple stakeholders, including fisherfolk, the Coast Guard, the Navy, and other maritime users. This overlapping use creates uncertainty over access and control.

As a result, the right to cultivate seaweed along the coast remains poorly defined and lacks the characteristics of a bankable property right. This leads to two key challenges. First, the absence of clear lease agreements increases operational risk for seaweed farmers, who may face disputes or displacement from cultivation sites. Second, without a secure and transferable tenure right, farmers are unable to use their cultivation sites as collateral or demonstrate long-term control over production areas, significantly limiting their ability to raise start-up capital from financial institutions.

The gap between India’s current registration regime and a commercially functional tenure system can be made precise using the property rights framework developed by Ostrom and Schlager (1996). In this framework, property rights are seen as a complex system where rights are bundled instead of a binary arrangement. They distinguish five types of property rights: access, withdrawal, management, exclusion, and alienation, and classify resource users based on which bundle of rights they hold.

An “authorised user” holds only access and withdrawal rights; an “owner” holds the full bundle. Table 1 applies this framework to India’s seaweed sector. It shows that India’s current registration system confers only the first two rights, leaving the farmer as an authorised user rather than a proprietor or owner. By reforming the sector and adding to the bundle of rights, farmers would benefit and the industry would grow. The Seaweed Ocean Lease (SOL) proposed later in this paper is designed to close this gap.

Table 1: Property Rights Bundle for Seaweed Cultivation in India

Applying the Ostrom–Schlager (1996) framework to India’s current registration regime and proposed marine tenure reform

| Right | Description (Ostrom & Schlager) | India: Current Status | India: Proposed Reform | Economic Implication |

|---|---|---|---|---|

| Access | Right to enter and be present in a defined marine area | Exists. Registration under CRZ and state fisheries rules permits the farmer to enter designated coastal waters for seaweed cultivation. | Retained, with spatial specificity. Access rights should attach to a georeferenced plot, not a general coastal zone. | Farmers gain certainty about where they can operate, reducing overlap with fishing, shipping, and tourism uses. |

| Withdrawal | Right to harvest products (seaweed biomass) from the site | Exists. The registration implicitly authorises harvesting of cultivated seaweed from permitted areas. | Retained and formalised. The harvest right should be explicitly stated in the tenure instrument, including permitted species. | Provides legal basis for farmers to defend harvests against encroachment or theft; supports crop insurance eligibility. |

| Management | Right to regulate use patterns, improve the site, and make operational decisions | Absent or ambiguous. No formal instrument empowers the farmer to decide cultivation methods, invest in site improvement, or set seasonal use patterns for a specific plot. | Granted. The tenure instrument should allow the farmer to choose cultivation methods, invest in site infrastructure (anchoring, nursery), and set seasonal schedules. | Enables long-term investment in site productivity; supports adoption of better seed stock, monitoring technology, and multi-species cultivation. |

| Exclusion | Right to determine who may access and use the site, and to deny entry to others | Absent. Registration does not confer exclusive possession of a defined ocean patch. Other users, like fishers, other farmers, and tourism operators cannot be legally excluded. | Granted, within defined boundaries. The farmer or farmer group should have the right to exclude unauthorised users from the demarcated cultivation plot for the tenure period. | The critical missing right. Without exclusion, farmers cannot protect their crop, justify investment, or prevent spatial conflict with competing ocean users. |

| Alienation | Right to transfer the cultivation right—by sale, lease, inheritance, or pledge as collateral | Absent. The registration is a personal permission; it cannot be sold, leased, inherited, or offered as security for a loan. | Granted, with safeguards. The tenure right should be transferable (within the coastal community), and mortgageable - subject to a ceiling on accumulation. | Unlocks access to formal credit (banks can lend against a pledgeable asset); allows efficient reallocation of sites to more productive users. |

| User status (Ostrom) | — | Authorised user – holds access and withdrawal rights only. Cannot manage, exclude, or transfer. | Owner — holds full bundle of rights: access, withdrawal, management, exclusion, and alienation. | The shift from authorised user to owner is what converts a dead asset into bankable capital. |

Why Leases Matter

A well-designed leasing mechanism could solve both these problems because it changes the legal character of the farmer’s right.

A permit removes a prohibition. A licence authorises an activity. A lease confers exclusive use over a defined area for a defined period. That makes the right secure, transferable, and potentially bankable. In practical terms, that means a seaweed farmer or enterprise can do three things that registration alone does not guarantee:

- raise institutional credit against a tenure-backed cultivation right;

- justify multi-year investments in moorings, seedbanks, nursery systems and processing links;

- and legally defend the site against encroachment.

Without a title, assets cannot be used as collateral, cannot be traded in liquid markets, cannot attract outside investment, and cannot be leveraged to build enterprises. Equally important is that the lack of excludability creates disincentives to the seaweed farmer. Improvement and investment come when there is potential for profitability, which follows excludability of the land - the ability to keep others outside of their patch. Further, sophisticated instruments that could both safeguard the farmer and ensure outside investments, such as crop insurance or forward contracts with processors, cannot come about without an underlying right.

International practice broadly also points in this direction. South Korea’s aquaculture business rights,14 the Philippines’ fishpond lease model,15 and Scotland’s two-stage seabed tenure system16 are examples where leasing rights have been created to allow the growth of seaweed cultivation responsibly, taking into account other stakeholders and also environmental damage. Table 2 outlines key details of the lease mechanism in these countries.

| Dimension | South Korea | Philippines | Scotland | Norway |

|---|---|---|---|---|

| Core instrument | Aquaculture Business Right | Fishpond Lease | Seabed Lease + Option Agreement | Aquaculture Licence |

| Property right strength | Highest (Real Right) | High (genuine lease) | High (seabed lease) | Medium (licence) |

| Tenure | 10+10 years | 25+25 years | Ongoing (reviewed) | No fixed term |

| Bankable / mortgageable | Yes | Yes | Yes | Partial |

| Pre-application site security | No | No | Yes — Lease Option | No |

| Community protection | Strong (statutory preference) | Weak in practice | Medium (consultation) | Weak |

The case of Indonesia is a useful case study of how ambiguity in property rights can lead to both horizontal and vertical conflicts, which can deter production and economic value addition. A paper by Satria et al. showcases these conflicts in Indonesia.17 In the Karimunjawa region, the conflict was vertical: farmers versus the national park authority, as the Marine Aquaculture Zone boundaries did not match where seaweed actually grows well, and farmers expanded beyond the designated zone. In Rote Ndao, conflict was horizontal: seaweed farmers versus tourism operators, because both claimed overlapping areas and there was no clear system for adjudicating competing spatial claims. This has implications for India as well.

The Main Recommendation: Create a Seaweed Ocean Lease

India should create a Seaweed Ocean Lease (SOL) as a way to drive seaweed cultivation growth.

The purpose of the SOL would be to convert seaweed cultivation from a subsidised activity into an investible enterprise. The lease should be issued over a mapped and approved marine area and confer exclusive cultivation rights over the relevant water column and seabed footprint for the lease term.

Suggested Features of the SOL

The design should include the following elements.

The mechanism for allowing seaweed cultivation should be a genuine lease, not merely a registration add-on. The lessee should hold exclusive cultivation rights over a defined marine polygon for the term of the lease, subject to environmental and community conditions. An initial term of 25 years, renewable for another 25 years on compliance, would be long enough to support credit, farmer aggregation, and investment in nurseries, seedbanks and local processing.

India could borrow Scotland’s strongest idea: a short site-reservation or pre-lease option phase, perhaps 12 to 18 months, to let applicants secure a site while they obtain environmental, navigational and local clearances.

Leases should be assignable, inheritable, and mortgageable, subject to CAA approval and compliance checks. This is central to bankability. All leases should be recorded in a digital national registry linked to geo-referenced maps. That reduces disputes and allows lenders, insurers and regulators to verify rights.

Lease fees should be based on area or installed cultivation capacity.

Fisher cooperatives, SHGs, FPOs and coastal community institutions should receive a first-right or preferential window for nearby lease zones. Large operators should not displace traditional users without safeguards. Norway, for instance, solves this problem by imposing capacity caps, such that no single entity can hold beyond a certain share of total production capacity. To prevent speculative accumulation and ensure equitable access, India could impose area ceilings at individual, cooperative and industrial levels. For any individual unit (family-run), the cap could be at 5 hectares, which allows for significant expansion for families, yet is a relatively small portion of the overall cultivable area. For cooperatives like Farmer Producer Organisations, the limit could be set at a higher ceiling of 25 hectares, which could provide employment to 220 families. For companies, instead of an absolute number, it could be set as a percentage (5 per cent) of the total notified seaweed cultivation area within any single state. These limits should be reviewed periodically as the sector matures, with the initial emphasis on ensuring that the community-preference window is not rendered meaningless by corporate first-movers.

Any tenure reform must be paired with ecological guardrails. A lease should be granted only in notified zones and only for approved species and cultivation systems, with clear rules on exotic germplasm, disease management, biosecurity and ecosystem monitoring.

India’s own evidence suggests that environmental risks can be managed with proper site selection and monitoring. A study of Kappaphycus alvarezii cultivation around the Gulf of Mannar found no significant difference in diversity indices between islands near and far from cultivation sites, supporting the case for evidence-based regulation rather than blanket prohibition. At the same time, the authors stress the need for ongoing policy vigilance.18

That means the SOL framework should include:

- mandatory zoning based on ecological sensitivity;

- exclusion of no-go areas and critical habitats;

- approved-species lists and rules for exotic germplasm;

- periodic environmental audits and biomass monitoring;

- a distinction between cultivated seaweed and wild harvest, with separate controls for the latter;

- and clear revocation conditions for non-compliance.

Seaweeds cannot be forced into a regulatory frame designed primarily for shrimp or finfish. Regulations such as effluent release, which are applicable to shrimp or finfish, are not applicable to seaweeds. Hence, seaweed-specific rules are necessary because the ecological footprint, risks, and benefits differ materially.

Proposed Structure for the Leasing Mechanism

Role of State Governments

State governments, through their fisheries departments or designated coastal authorities, should take the lead in issuing and administering seaweed leases within their territorial waters.

State responsibilities would include: - identifying suitable cultivation zones in consultation with research institutions such as ICAR-CMFRI and CSIR-CSMCRI and CAA’s cultivation atlas; - issuing Seaweed Ocean Leases for defined marine areas to individuals, cooperatives, SHGs, FPOs, or companies; conducting stakeholder consultations, particularly with traditional fishing communities, before approving lease areas; - monitoring operational compliance with environmental and cultivation standards; - and resolving local disputes relating to overlapping marine uses.

This state-led leasing approach recognises that coastal waters are multi-use spaces where local governance, community engagement, and environmental monitoring are essential. Further guidance on how states can incorporate various priorities while centering on local communities has been previously published.19

This model balances national coordination with state-level flexibility. It avoids excessive centralisation while ensuring that leases remain standardised and credible for investors. By combining state-issued leases with a nationally maintained registry and regulatory framework, India can create a tenure system that is both administratively practical and financially bankable.

Such a framework would allow seaweed cultivation to transition from small-scale pilot projects to a scalable coastal bioeconomy activity, unlocking investment, improving farmer incomes, and strengthening India’s emerging marine biotechnology ecosystem.

Conclusion

India has already recognised seaweed as an important contributor to the bioeconomy. But the full realisation of this potential will depend on providing incentives for seaweed cultivation that go beyond grants and legalisation. India already has a downstream industry that utilises seaweed, providing a domestic market for seaweed, in addition to the available export opportunity. A leasing mechanism that can be used to raise capital and investor/farmer confidence in investing in seaweed cultivation would catalyse this sector’s growth.

Appendix I

| Category | Global Market Size | Basis |

|---|---|---|

| Food & food ingredients | ~USD 12.4–13.6 billion | Derived as roughly 80 per cent of the USD 15.5–17 billion global seaweed market, based on the FAO/World Bank use split of 40 per cent direct human consumption + 40 per cent processed food use. |

| Hydrocolloids (carrageenan, alginate, agar) | ~USD 1.16 billion | Historical consolidated benchmark from the World Bank table for hydrocolloids: agar USD 191 million + alginate USD 339 million + carrageenan USD 626 million. This is older and conservative, but still one of the few validated consolidated figures. |

| Agriculture / biostimulants | ~USD 1.88 billion | World Bank potential market size for seaweed biostimulants. The same report notes seaweed extracts in the broader biostimulants market were about USD 935 million in 2021. |

| Animal feed additives & pet food | ~USD 2.20 billion | Combined World Bank potential market size of animal feed additives USD 1.08 billion + pet food USD 1.12 billion. |

| Nutraceuticals & alternative proteins | ~USD 4.40 billion | Combined World Bank potential market size of nutraceuticals USD 3.95 billion + alternative proteins USD 0.45 billion. |

| Bioplastics, fabrics & other advanced biomaterials | ~USD 2.99 billion | Combined World Bank potential market size of bioplastics USD 0.73 billion + fabrics USD 0.86 billion + construction materials USD 1.40 billion. |

Appendix II

| State | No. of Sites (ICAR-CMFRI) | No. of Sites (CSIR-CSMCRI) | Potential Area (hectares) |

|---|---|---|---|

| Andhra Pradesh | 37 | 3 | 1355 |

| Diu | 2 | — | 404.47 |

| Goa | 4 | 3 | 62.84 |

| Gujarat | 13 | 7 | 10704.13 |

| Karnataka | 11 | 3 | 1280.05 |

| Kerala | 7 | 1 | 79.67 |

| Lakshadweep | 11 | — | 212.80 |

| Maharashtra | 10 | 3 | 2871.31 |

| Odisha | 14 | — | 1483.76 |

| Puducherry | 23 | — | 382.53 |

| Tamil Nadu | 196 | 24 | 5332.24 |

| West Bengal | 5 | — | 448.84 |

| Andaman and Nicobar | — | 7 | 16.5 |

Footnotes

United Nations Conference on Trade and Development, “An Ocean of Opportunities: The Potential of Seaweed to Advance Food, Environmental and Gender Dimensions of the SDGs,” UNCTAD, 2024. Link↩︎

Global Market Insights, “Commercial Seaweed Market Size, Share, and Growth Forecast,” GMI, 2023. Link↩︎

Khanjan Trivedi, Vijay Anand Gopalakrishnan, Vaghela Pradipkumar, Alan Critchley, Pushp Shukla, and Arup Ghosh, “A Review of the Current Status of Kappaphycus alvarezii Based Biostimulants in Sustainable Agriculture,” Journal of Applied Phycology 35 (2023). Link↩︎

Vaibhav Mantri, Karuppanan Eswaran, Shanmugam Munisamy, Ganesan Meenakshisundaram, Veeragurunathan Veeraprakasam, Sangaiya Thiruppathi, CRK Reddy, and Abhiram Seth, “An Appraisal on Commercial Farming of Kappaphycus alvarezii in India: Success in Diversification of Livelihood and Prospects,” Journal of Applied Phycology 29 (2017). Link↩︎

F. E. Msuya and A. Q. Hurtado, “The Role of Women in Seaweed Aquaculture in the Western Indian Ocean and South-East Asia,” European Journal of Phycology 52, no. 4 (2017): 482–494. Link↩︎

United Nations Conference on Trade and Development, “An Ocean of Opportunities: The Potential of Seaweed to Advance Food, Environmental and Gender Dimensions of the SDGs,” UNCTAD, 2024. Link↩︎

CEIC Data, “India Imports Volume: HS 12122110: Seaweeds,” CEIC, accessed March 2026. Link↩︎

NITI Aayog, “Strategy for the Development of Seaweed Value Chain Fostering Diversified Livelihoods,” NITI Aayog, 2024. Link↩︎

B. Johnson, G. Tamilmani, D. Divu, Suresh Kumar Mojjada, Sekar Megarajan, Shubhadeep Ghosh, Mohammed Koya, M. Muktha, Boby Ignatius, and A. Gopalakrishnan, Good Management Practices in Seaweed Farming, CMFRI Special Publication No. 148 (Kochi: ICAR-Central Marine Fisheries Research Institute, 2023).↩︎

Press Information Bureau, “Pradhan Mantri Matsya Sampada Yojana: Seaweed Development,” Ministry of Fisheries, Animal Husbandry and Dairying, Government of India, 2026. Link↩︎

Press Information Bureau, “Seaweed Cluster in Lakshadweep and Centre of Excellence at ICAR-CMFRI,” Ministry of Fisheries, Animal Husbandry and Dairying, Government of India. Link↩︎

Press Information Bureau, “Seaweed Production Statistics 2024,” Ministry of Fisheries, Animal Husbandry and Dairying, Government of India, 2024. Link↩︎

Press Information Bureau, “Seaweed Cultivation Sites Identified by ICAR-CMFRI and CSIR-CSMCRI,” Ministry of Fisheries, Animal Husbandry and Dairying, Government of India, 2026. Link↩︎

Korea Legislation Research Institute, “Aquaculture Industry Development Act (South Korea),” KLRI, accessed March 2026. Link↩︎

Republic of the Philippines, “Republic Act No. 8550: The Philippine Fisheries Code of 1998,” Official Gazette of the Philippines, 1998. Link↩︎

Crown Estate Scotland, “Aquaculture Leasing: Seabed Tenure in Scotland,” Crown Estate Scotland, accessed March 2026. Link↩︎

Arif Satria et al., “Property Rights and Conflicts in Seaweed Farming in Indonesia,” Ocean & Coastal Management (2018). Link↩︎

Veera Gurunathan, Vaibhav Mantri, Karuppanan Eswaran, and Malar J. M., “Influence of Commercial Farming of Kappaphycus alvarezii (Rhodophyta) on Native Seaweeds of Gulf of Mannar, India: Evidence for Policy and Management Recommendation,” Journal of Coastal Conservation 25 (2021): 1–12. Link↩︎

KapilDev Bhal, “Coastal Communities: Sustainable Livelihood Opportunities,” Marine Engineers Review (India) 18, no. 5 (2024): 31–36.↩︎