Turbulence Ahead for the Indian Airline Industry

| AUTHOR | Anupam Manur |

| DATE | March 27, 2026 |

| DOCUMENT | Takshashila Issue Brief 2026-09. |

| VERSION | Version 1.0, March 2026. |

| CATEGORIES | Economic Policy West Asia |

Introduction

The Indian aviation sector is hit particularly hard due to the ongoing US-Israel strikes on Iran and the subsequent retaliation and closures of the air space around the war zone. The aviation industry, which was recently rocked by IndiGo’s massive flight-scheduling disruptions, is now poised for a long, arduous journey ahead, with multiple, interconnected channels affecting its operations and profitability.

The Union Government had put a price cap on domestic air fares on 6th December 2025 during the IndiGo crisis. Since operational costs for airlines have increased significantly due to the war, and the airlines have not received any relief from union or state taxes, the airline companies asked the government to remove the airfare price cap, and the government complied. The price cap was removed on 23 March 2026; however, with the caveat that “excessive or unjustified surge in fares during periods of peak demand, disruptions, or exigencies, will be viewed seriously” and that fare caps can be reintroduced “if required in public interest.”1

Compounding Operational Costs

ATF Price Increase and Compounding Taxes

Jet fuel prices have already doubled from around USD 85–90 per barrel before the attack on Iran, to between USD 150 and USD 200. Aviation Turbine Fuel (ATF) accounts for roughly 35–40 per cent of an Indian airline’s operating costs, so this is devastating. Even a USD 1 per barrel increase in crude prices can add around ₹300 crore to IndiGo’s annual fuel bill alone.

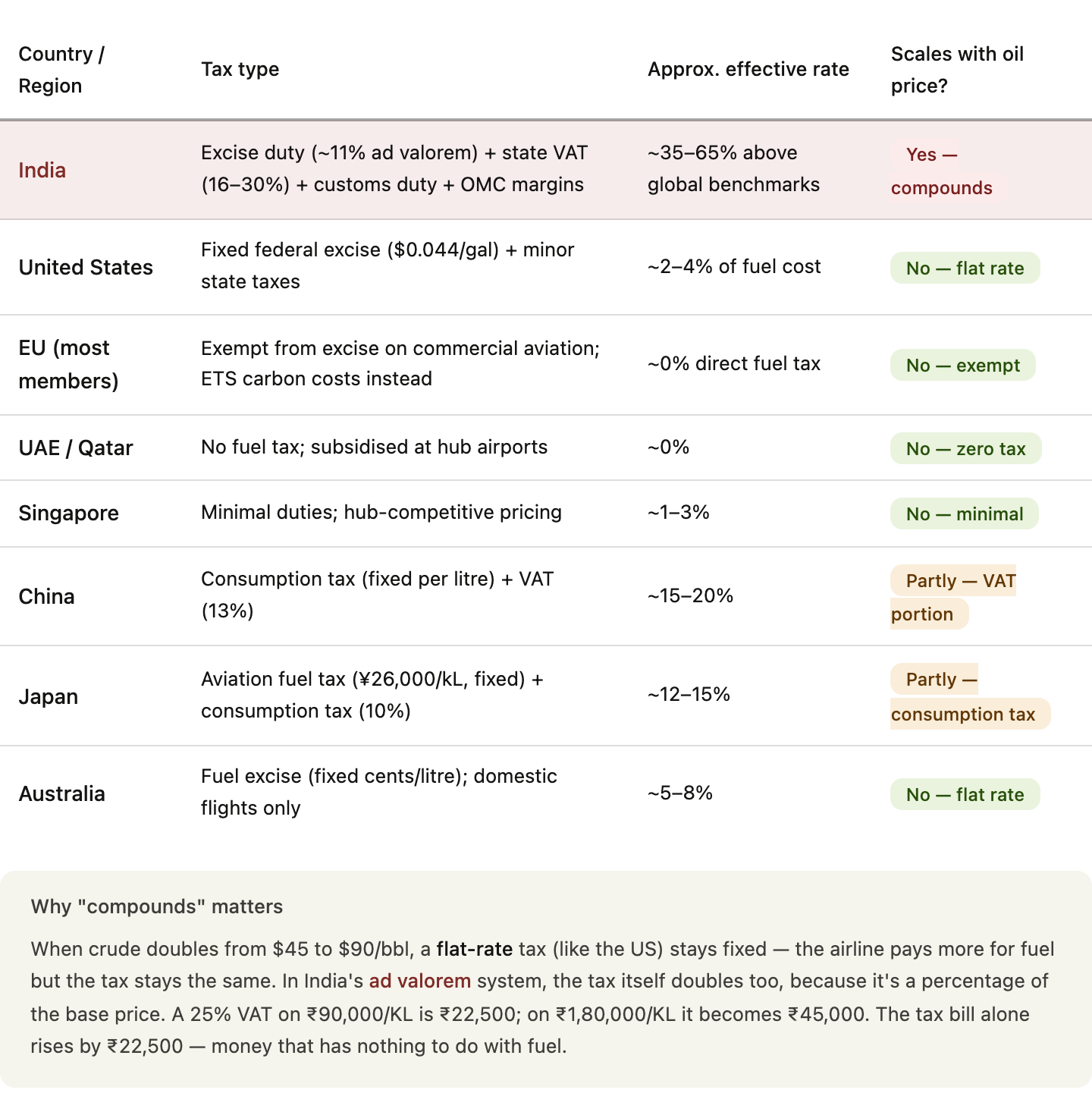

The bane of compounding taxes: India’s unique tax structure amplifies the pain. Central excise duty and state-level VAT on ATF are levied as a percentage of the base price, with VAT rates in hubs like Delhi often in the 20–25 per cent range. Given that the base price has risen dramatically, the absolute tax has risen proportionately as well, which affects Indian carriers more than in other countries.

In most other countries, taxes on ATF are a flat rate per gallon instead of the ad valorem (percentage of price) taxes in India. In the US, for instance, the federal excise tax on jet fuel is a fixed cents-per-gallon amount, so when crude prices spike, the tax portion stays constant. Many other countries, such as the Gulf states, Singapore and, to some extent, even the EU, have zero taxes on ATF.

As a side note, it is also no coincidence that big transport hubs have zero taxes on ATF and India cannot dream of becoming one with the current tax structure. ATF also remains outside the scope of India’s GST regime, which means each state charges its own VAT rate, creating price disparities across airports. In Delhi, ATF currently costs ₹96,638 per kilolitre, while in Chennai it is over ₹1,00,280 — a difference of nearly ₹4,000 per KL because of varying state taxes.2

India is one of the few major aviation markets where nearly every layer of fuel taxation is percentage-based. Indian carriers pay around 65 per cent more for ATF than their global counterparts, and the gap widens during price spikes because the tax structure amplifies rather than absorbs volatility.3

Airspace Closures

The Pakistan airspace has been closed for Indian aircraft for nearly a year now, since 24 April 2025. Industry reports submitted to the Ministry of Civil Aviation estimate a consolidated annual loss of ₹7,000 crore (roughly USD 800 million) for Indian airlines, stemming from extended flight paths, higher fuel expenses, and cancellations. Air India alone could lose USD 591 million due to this closure. To put this in context, Air India reported a net loss of USD 520 million in fiscal 2023–2024.

A 16-hour flight to North America now takes an additional 1.5 hours, adding around ₹29 lakh in extra operating costs per trip. Flights to Europe face similar delays, costing about ₹22.5 lakh extra per trip. Even Middle East-bound flights see roughly 45 minutes of additional flying time, costing about ₹5 lakh per flight.4

What makes the current moment uniquely painful is that the Pakistan closure and the Iran war have shut down both of India’s western air corridors simultaneously. After Pakistan, the closure of Gulf airspace means the loss of a second western corridor, with around 800 weekly flights on long-haul and mid-to long-haul routes affected.5 Gulf markets are a key contributor to India’s aviation sector, accounting for nearly 50 per cent of total international passenger traffic to and from India.

Rupee Depreciation Adds to the Burden

The Indian rupee depreciated by nearly 9 per cent in FY26, increasing the financial burden on airlines since 35–50 per cent of operating expenses — including aircraft leases, maintenance, spare parts, and crew salaries — are denominated in dollars. As of 26 March 2026, the USD/INR exchange rate hit a new low of ₹94.03 per dollar.

Rough estimates suggest that the additional loss to the Indian aviation industry could be ₹4,700 crores plus or minus 30 per cent. This estimate accounts for flight cancellations, fuel cost increases, rerouting, insurance, crew costs, refunds, lost cargo revenue, and forex impact across Indian carriers over the first four weeks of the conflict.

The Response

Of the 92,000 flights scheduled in and out of the Middle East between February 28 and March 12, over 49,000 were cancelled. Ticket prices from India to the Gulf states have risen dramatically (by 233 per cent). Similarly, ticket prices to the United States are 250 per cent more expensive.

The government removed temporary fare caps on March 23, 2026, which had been in place since December 2025 following IndiGo’s mass cancellation crisis. This means airlines now have full pricing freedom just as fuel costs are at their highest, and analysts expect domestic fares to rise significantly, especially on peak routes and last-minute bookings.

Airline carriers in India have implemented a fuel surcharge per ticket starting 12 March on both domestic and international routes.

The steeper prices are bound to hit domestic demand. The Indian domestic aviation market is highly price-sensitive. When ATF prices rise and fares follow, passenger demand often drops, particularly among leisure travellers.

Airlines might cut unprofitable routes from their portfolio: marginal routes that made sense at lower ATF prices may not be worth running. Fewer flights might again constrict supply and increase the demand for existing flights between major routes, pushing up prices even higher.

Potential Solutions

Though the crisis is global in nature and some of the structural problems are outside India’s direct control (Pakistan airspace closure), there are still a few policy levers that can be used.

Immediate Responses

Tax relief on ATF: The immediate measure that the government must undertake is to give relief on taxes on aviation fuel. The Union government can reduce customs and excise duty and coordinate state-level VAT reductions on ATF.

Resist the urge to cap fares: Though the government has removed air fare caps for now, they have threatened to bring it back if prices increase too much. Price caps never work and should not be considered as a policy option.

Use India’s Strategic Petroleum Reserve (SPR): If the situation gets really dire, India can release a portion of its SPR, though airline fuel would be low on the priority for usage.

Alternative airspace negotiations: The government is exploring northern flight paths that would bypass Pakistan and Afghanistan entirely, routing aircraft from Delhi to Leh, over the Hindu Kush into Kyrgyzstan and Tajikistan, then onward to Europe — but this requires diplomatic approval from China for airspace access.

Structural Responses

Bringing ATF under GST: This is the single most impactful structural reform that could be made. It would standardise ATF taxation nationally, eliminate the wildly varying state VAT rates, and likely bring the effective tax rate below the current 35–65 per cent premium over global benchmarks.

Rationalising airport charges: The bidding and concession structure for Indian airports are designed in such a way that guarantees high downstream costs for passengers. The reforms to this process are beyond the remit of this paper, but this is a structural reform worth examining.

Breaking the OMC oligopoly in ATF supply: Allowing private and international fuel suppliers broader access to supply ATF at Indian airports would introduce competition and pressure on marketing margins. Currently, the three state-owned companies face no meaningful competitive discipline.6

Fuel hedging: Unlike European carriers that hedge significant portions of their fuel exposure, Indian airlines largely fly unhedged. This makes the passenger much more vulnerable to fuel price shocks. Given that the OMCs are largely government owned and that India imports most of its oil and is therefore vulnerable to global oil shocks, airline companies should be encouraged to hedge oil prices.

Most of the meaningful and impactful responses, such as bringing ATF under GST and building hedging mechanisms, will take time and cannot address the current situation. The best option now is to allow the market to price tickets based on value of travel, which can cut down on discretionary travel. Summer vacations will become more expensive in the short run.

The biggest tool for the government is to give tax relief on ATF. A concrete first step could look something like this: halving central excise on ATF from 11 per cent to 5.5 per cent and coordinating a 10-percentage-point reduction in state VAT at major airports would save the industry approximately ₹300 crore per week, offsetting roughly a quarter of the estimated crisis-related losses, which were estimated at ₹1,200 crores per week. This would cost the government roughly an annual fiscal loss of ₹7,500–8,000 crore.

Footnotes

“Govt Removes Domestic Fare Caps as Airline Operating Costs Skyrocket; Flying to Cost More,” The Economic Times, March 23, 2026. Link.↩︎

“ATF Price Hike: OMCs Revise Rates in March 2026 Ahead of Travel Season,” Zee Business, March 2026. Link.↩︎

“India’s ATF Tax Burden on Airlines,” SP’s AirBuz, 2026. Link.↩︎

“How Air India, IndiGo and the Modi Government Are Dealing with Pakistan’s Airspace Closure,” Outlook Business, 2025. Link.↩︎

“Gulf Airspace Closure to Impact Air India, IndiGo Earnings,” Business Today, March 1, 2026. Link.↩︎

The marketing spread in markets such as Dubai, London, or Singapore is typically USD 15–30 per metric tonne (roughly ₹1–2 per litre), compared to India’s ₹15 per litre — so the margin difference is real, perhaps 7–10 times higher in India. However, this needs context: some of that difference reflects India’s higher distribution costs, infrastructure investment, and the fact that Indian airports often have less efficient fuelling logistics than Singapore or Dubai.↩︎