Beyond Dollar

| AUTHOR | Anisree Suresh |

| DATE | March 22, 2026 |

| DOCUMENT | Takshashila Discussion Document 2026-08. |

| VERSION | Version 1.0, March 2026. |

| CATEGORIES | Economic Policy India's Trade Policy |

Executive Summary

The US dollar remains the dominant reserve currency, with its supremacy being reinforced by liquidity and powerful network effects that no alternative currency can currently replicate. Yet, this reality now coexists with a growing unease. Repeated tariffs, the threat of sanctions and the weaponisation of international trade, along with a changing geoeconomic order, have raised the costs of exclusive reliance on the dollar for many economies. The result is not an imminent displacement of the dollar, but a gradual decoupling from the dollar system.

India’s interest in the Rupee Trade Settlement Mechanism (RTSM) must be understood in this context. The objective is not to challenge the dollar’s global role, but to expand the rupee’s use at the bilateral level.

This paper argues that India’s opportunity does not lie in sanction-driven or geopolitically forced adoption of rupee settlement, which tends to be fragile and prone to imbalances. Nor does it lie in attempting to replicate the dollar’s global role. Rather, the most sustainable pathway forward is a market-driven expansion of rupee usage among countries that have substantial-and relatively balanced-trade with India, even if they currently face low direct pressure to exit the dollar system. In these relationships, rupee settlement is feasible today, and demand can increase gradually as global trade uncertainty rises. This approach avoids the pitfalls of rupee accumulation while possibly minimising political backlash.

A structured scenario framework is used to assess where RTSM can realistically succeed. The analysis shows that India must focus less on identifying ideal partners, and more on building the institutional and financial conditions that can convert feasibility into durable demand over time.

Introduction

The global economic order is changing swiftly with emerging market economies assuming major roles in production, international trade and cross-border transactions. The emerging markets accounted for 50.8 per cent of global GDP in 2024,1 and their share in global trade increased from 32 per cent to 46 per cent between 2000 and 2019.2 The rise of new economic growth centres is not a new phenomenon. The world has seen the rise and fall of new economic growth centres capable of providing global economic stimulus through commercial and financial transactions.3 While the current system prevails-characterised as it is by the US and its western allies maintaining and issuing international reserve currencies - there have been active efforts to accommodate the new reality of the world, which is the stronger presence of emerging market economies in the international monetary system.

In this context, local currency trade settlements have been gaining momentum as currencies seek to reduce dependence on the US dollar and hedge against geopolitical and financial uncertainties. India has been exploring the Rupee Trade Settlement Mechanism (RTSM) in an effort to internationalise its currency, and facilitate its bilateral trade in Indian Rupee (INR). For the rupee to be globalised, the currency must garner demand beyond its national jurisdiction. In order to create this demand,4 the currency must be able to maintain the confidence of its value, reduce transactional costs and satisfy the role of an international currency. Even if there is an adequate supply of a particular currency-supported by domestic macroeconomic policies and institutional support-if it is not able to generate international demand, it will be unsuccessful as an international currency.

In the future of global currency dominance, the most likely scenario is that the dollar will continue to reign owing to the concept called the dollar trap.5

The dollar trap implies the existence of a “self-reinforcing” mechanism: the more widespread the dollar is used, the more liquid the markets for dollar-denominated assets become, further increasing its attractiveness. Path dependency and inertia are also at play and make switching to other currencies costly and cumbersome, as are network effects, with financial systems deeply entrenched in dollar-denominated operations. Coined by Prasad, E.S. (2014), “The Dollar Trap”, Princeton University Press.

It means that the more widespread the use of the dollar, the more liquid the markets for dollar-dominated assets become, thereby further increasing its use. This path dependency makes it difficult for countries to switch to other currencies. However, trust in the dollar can be affected by the US policy choices, such as tariff-induced uncertainties and capital restrictions for foreign investors in US assets. An alternative scenario is that the dollar gradually loses significant ground over a longer period of time, as a market mechanism.6 The survey report of the World Gold Council notes that three-quarters of the 73 central banks that responded to the survey expected their dollar-denominated reserves to be lower in the next five years compared to 62 per cent of last year, signalling the reduced importance of the dollar in central bank holdings.7 In this scenario - most likely-several reserve currencies share global status, with the dollar retaining some measure of importance.

While the US dollar will not be displaced as an international currency owing to its incumbency advantages, India can potentially benefit from rupee trade settlements at a bilateral level. This paper tries to address two critical questions: Does the current global economic order demand that India look for alternative channels for its international transactions? If so, can India pursue a Rupee-based Trade Settlement Mechanism (RTSM)? Political considerations (India’s national interest, weaponisation of the dollar, and Trump’s tariff threats), along with domestic economic factors, shape the demand for-and success of the Indian rupee. By examining the possible scenarios of RTSM adoption, ranging from geopolitically-driven necessity to market-driven expansion, this paper proposes a roadmap for India to gradually internationalise the rupee through market-driven approaches.

Why the Dollar Made Sense Until Now!

When the Second World War ended, the world faced an unprecedented challenge of rebuilding the shattered economies and restoring international trade after years of conflict. In 1944, representatives from the Allied nations met at Bretton Woods to forge a new monetary order. At this time in history, the US produced a very large share of global industrial output and, importantly, held about two-thirds of the world’s official gold reserves, while the rest of the world was physically and financially exhausted by the war. In 1944, the Bretton Woods Conference laid the foundation for the USD’s reserve currency status by pegging the dollar to gold at a fixed rate of USD 35 per ounce. In the Bretton Woods system, countries linked their currencies to the dollar, which could be exchanged for gold at a fixed rate.

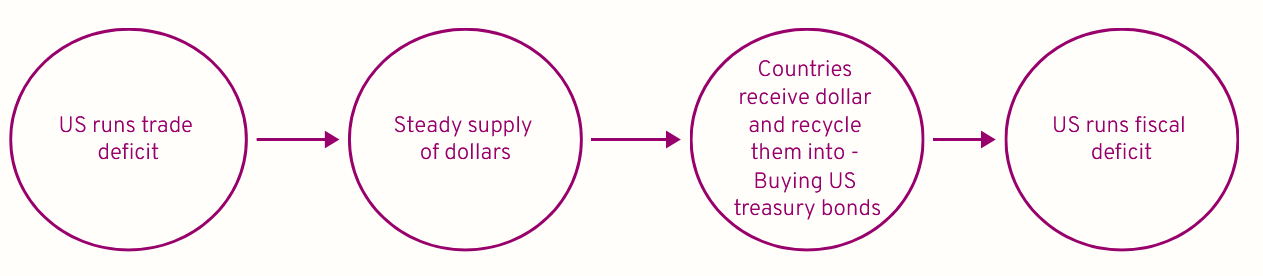

As global trade expanded, the world’s demand for dollar liquidity expanded too, and that’s where the problems started to raise their heads. As trade increased, the world needed more dollars to circulate outside the US. Robert Triffin hence argued in the 1960s8 (which later came to be known as the Triffin Dilemma), if the world wanted the dollar as its reserve currency, the US had to supply it.9

The Triffin Dilemma refers to the fundamental conflict between short-term domestic economic objectives and long-term international economic objectives for a country that issues the global reserve currency. To supply sufficient liquidity to the world, the issuing country must run persistent balance-of-payments deficits, but doing so eventually undermines confidence in the currency’s value and stability.

To supply it, the US had to run twin deficits (fiscal and trade deficits), and when the issuer country ran deficits for long enough, the promise (back then, convertibility to gold) was kept real. The dilemma herein is that domestic priorities of the currency issuer country eventually collide with the external role the currency plays. By the mid-to-late 1960s, the US had domestic policies of guns and butter to support the war in Vietnam and greater welfare programs domestically. US gold reserves,10 fell steadily over the decade, reaching about USD 11.1 billion by December 1970. At the same time, external dollar demand continued to rise. This benign neglect11 of external balance owing to the domestic political costs led to then-President Nixon closing the gold window in 1971. In the post-1971 system, the dollar became a fiat currency, backed not by gold but by the economic strength of the US and its institutional credibility. The US continued to supply global liquidity by running fiscal and external deficits, and the rest of the world continued to recycle those dollars back into US financial markets. Hence, the dollar continued to make sense because it allowed deeper markets and predictability through reliable collateral. The network effect, too, was strong as the dollar was deeply embedded in trade and banking networks.

Emerging Patterns that Challenge the Dollar System

In the post-1971 system, once the dollar became fiat, its value was formally guaranteed only by US institutions and trust. To support the supply of dollars as a global currency, the US ran persistent fiscal and current account deficits. This produced a large, continuous supply of US government debt in the form of US Treasury securities. Treasuries could be bought or sold in massive volumes, and they provided liquidity and certainty that no other bond market could offer. However, with the current Trump administration attempting to address the US trade deficit, it’s impacting the channel that supplies dollars globally, while also affecting the credibility of the US as an anchor to the global monetary system.

Weaponisation of the Dollar

While the dollar continues to be the designated main reserve currency, it has always been a concern as some countries feared the weaponisation of the US dollar against them via sanctions or seizures. These concerns escalated in the 1970s, with the first sanctions against Iran and reserve seizures,12 freezing of Libya’s assets13 in the 1980s, and the use of US anti-money-laundering and taxation policies globally. This led to the institutionalisation of the Financial Action Task Force (FATF) and the Organisation for Economic Cooperation and Development (OECD). Post 2008’s global financial crisis, these tools have been used extensively in relation to Iran, North Korea and Russia. This led to many countries,including the EU, China, and Russia, developing their own arrangements to reduce US monetary hegemony, and reap the benefits of being a reserve currency. For instance, Europe’s INSTEX14 was created to sustain some trade with Iran outside US secondary sanctions in 2019. While this was a small experiment, it symbolises how even US allies were testing bypass concepts. During 2023-2025, the yuan surpassed15 the dollar in China’s own cross-border payments, accounting for over 50 per cent of transactions, while the dollar’s share fell to around 40 per cent. China has managed it through energy and commodity trade with partners like Russia and the Gulf states, which are increasingly settling in RMB (renminbi) rather than dollars.

Russia’s invasion of Ukraine in 2022 has brought attention to how currencies and payments are affected in conflicts. The weaponisation of finance was possible through a digitised global monetary and payment system, coupled with the US dollar as the dominant currency. In response to the Russian invasion of Ukraine, the US and EU, along with other countries, imposed wide-reaching sanctions on Russia - including cutting Russian banks off from SWIFT and restricting exports to and from Russia. Russia’s central bank’s currency reserves, worth USD 300 billion, were frozen. Since the September 11, 2001 attacks, the US has repeatedly used economic and financial actions as a first resort tool against its adversarial countries. In mid-2025, the US imposed sanctions on several Indian companies16 for their involvement in trading Iranian petroleum and petrochemical products, and has also threatened secondary sanctions on India over its Russian oil purchases. This has increased the cost of using the dollar system, especially when it’s against the country’s energy strategies.

Central Bank Reserve Diversification

Though the US dollar remains dominant, its share has gradually declined over the past two decades. In 1999, the dollar’s share of global reserve currency17 stood at 71 per cent, which fell to 57 per cent in 2025. However, the lost share did not move to a single rival currency; it dispersed across multiple currencies and assets-with the euro holding roughly 20 per cent of the share, the yen 5-6 per cent, and the Chinese yuan around 2 per cent. A major central banks’ reserve diversification is towards increasing gold holdings. Central banks globally purchased over 1000 tonnes of gold annually, the highest pace in decades, in 2022-2024.

Reduction in Dollar-Denominated Sovereign Debt

Historically, many developing economies borrowed heavily in dollars. Over the past two decades, however, there has been a structural shift toward domestic - currency debt and local bond markets - significantly reducing reliance on dollar borrowing. It was mainly due to investors’ lack of interest in local currencies that the domestic financial markets were shallow, with inflation histories reducing credibility for these developing economies. For instance, before the Asian financial crisis of 1999, over 60-70 per cent of external debt in many Asian economies was denominated in dollars. Local-currency government bond markets18 in emerging economies expanded from roughly USD 1 trillion in the early 2000s to over USD 12 trillion by the early 2020s. China has one of the lowest levels of foreign-currency sovereign borrowing among major economies, with over 95 per cent of Chinese government debt denominated in RMB.

Technology-Driven Currencies

Bitcoin was launched in January 2009 as the first decentralised digital currency, and the first non-permissioned blockchain application. It was introduced as a challenge to the fiat currency19 model, which was seen as central to the 2008 crisis. However, it has failed to emerge as a major challenge to the principal fiat currencies, or dollar hegemony, so far. It’s been used, though, by a few developing countries with weak monetary and financial systems where Bitcoin offers an alternative monetary instrument and payment system. The Facebook announcement of rolling out its own cryptocurrency in 2019, called Libra, forced central banks to reconsider their monetary offerings to better meet the needs of the economy and financial system, called Central Bank Digital Currencies (CBDC).

A fiat currency is a type of money that has no intrinsic value but is declared legal tender by a government. Its value is derived from the public’s trust and confidence in the issuing government and the stability of the economy. Unlike currencies backed by a physical commodity like gold, fiat money is not redeemable for anything of intrinsic value.

In October 2019, China announced it would launch its digital currency/electronic payment, which is now labelled as the eCNY. Work on global CBDCs has been progressing steadily, with the 2022 Bank of International Settlements (BIS) report20 indicating that the share of central banks engaged in some form of CBDC work rose to 93 per cent, with half at the stage of experimenting or pilots. The COVID-19 digitalisation has given rise to presence-less payments, and central banks across the world are considering whether they can-and should-develop and implement their own CBDCs. While at present it remains within the domestic jurisdiction of each country, the current geopolitical situation is driving the possibility of a restructuring away from the dominance of a single currency. If China successfully develops eCNY for use in international trade transactions, it might be beyond the reach of US sanctions.21 In the longer term, the digitalisation of interactions in the economy and the spread of digital currencies-public and private-increases the likelihood of disruption in the global currency order because of their potential to override existing network effects.

The Trump Effect on (De)Dollarisation

Under Trump’s administration, the argument of exorbitant privilege that the US enjoys owing to the dollar’s international reserve currency status takes a back step to more of a rigged bargain. Even during its first term, the Trump administration used delegated tariff authorities at scale22, such as Section 201 safeguards, Section 232 national security tariffs on steel/aluminium, and especially Section 301 tariffs aimed at China, as a necessary step to correct the trade deficit it has with its trade partners. In the second term as well, the same logic continues as he has imposed reciprocal tariffs extensively on all trading partner countries of the US. On the other hand, the proposed One Big Beautiful Bill is a budget-reconciliation package that shapes the fiscal deficit and therefore the supply of treasuries. The US trade policy at the moment tries to compress external deficits and potentially limit the dollar liquidity outside of the US. Meanwhile, its fiscal policy choices (if they come into effect) can expand into more issuance of Treasury Securities.

Typically, investors flock to dollar debt as a safe haven from financial uncertainty, boosting the currency’s value. Based on this, the dollar should have appreciated by about 5 per cent. Instead, its value fell by more than23 3 per cent over the next 10 days, following the April 2nd, 2025 announcement by the US to impose tariffs upon its trading countries. During the first 100 days of the Trump administration, the dollar’s value fell as much as 10 per cent. The first-order impact24 of this trade policy is that fewer imports mean fewer dollars flowing out of the US through trade, and all else equal, translates to a shortage in the global supply of dollars. This asymmetry is a problem when the US dollar is on one side of 88 per cent of foreign exchange trade25 that happens annually the world over. This could lead to a reduction in the supply of dollars, while the demand for them continues to grow. However, due to policies that undermine global economic cooperation - such as the weaponisation of dollars, tariffs and the general unpredictable nature of the Trump administration - confidence in US leadership has weakened. Trump-era policies have accelerated the search for alternative payment systems,26 reserve diversification, and local-currency trade. The impact on the credibility of the institutions27 could lead to a reduction in dollar demand as well, leading to a new equilibrium. In this equilibrium, the dollar might remain as the major reserve currency, but countries might actively hedge against it.

If the US growth outlook continues to worsen and inflation expectations rise, the attractiveness of US assets to foreign investors might diminish. Moody’s evaluation28 (global credit rating agency) from May 2025 warns of a scenario, albeit unlikely, wherein global investors could seek to rapidly exit US assets.

The US has shown a greater willingness to weaponise its economic strength, whether it’s through tariffs or sanctions, in order to impact the way central banks look at the dollar as a security. Reserve currency status can only be diminished when there are credible substitutes. Based upon these dimensions, no alternative comes close. Even as some diversification occurs, the dollar continues to dominate reserves, global payments, and collateral markets because the costs of exit remain high and network effects stay powerful.

Does India Need a Rupee Trade Settlement Mechanism?

The increased trade flow and the gradual opening of the economies to foreign capital have benefited the developing economies in becoming the centres of economic growth. However, with an increasingly multipolar economic order, the question arises whether the current international monetary system reflects the realities of the global economic order. This demands a revisit to the economic governance structures, especially the centrality of the US dollar29 in the global monetary system. While the US dollar might continue to remain centre stage, there are increasing efforts to de-monopolise the dollar30 to abstract macroeconomic benefits from the evolving system.

What are the Benefits of Rupee Internationalisation?

In order for India to internationalise its currency, it needs to create deep and liquid financial markets. To increase the demand for the rupee, an economy should have wide trade networks to support the use of the currency both as a unit of account as well as a medium of exchange. Just like the value of a product or service rises as more people use it, if the demand for rupee increases, it will become more global. The demand for a local currency increases with that country’s increasing share in world exports, and the proportion of its exports to countries that are not issuers of global currencies. Along with that, a country’s macroeconomic and financial stability, such as high GDP growth rates, as well as low and stable inflation, are key factors in determining a currency’s attractiveness. Along with increasing demand, the country has to match the expected demand with the ability to provide rupees on an international stage, with strong supply-side factors supporting it. This requires adequate domestic financial market depth, and provides borrowers and investors with access to a range of financial instruments which are backed by the country’s real economic activity and sovereign fiscal position.

The exchange rate pass-through effect refers to the extent to which changes in exchange rates are reflected in the prices of traded goods and services. A high pass-through means that currency depreciation quickly raises import prices and inflation, increasing the cost burden for import-dependent economies like India.

While internationalisation is a gradual and lengthy process, India can benefit from rupee trade settlements with its trading partners. However, the immediate objective of undertaking local currency trade settlement is multifold. Firstly, to reduce the country’s reliance on US dollars, and hence decouple the economy from the shocks and policy decisions of the global currency-issuing country (to the extent possible). Secondly, to contain the impact of the exchange rates31 of a global currency (mostly the US dollar) on the country that is undertaking trade under dollar denominations.

By diversifying some volume of trade away from the dollar, India can reduce the cost of transactions as there are little to no currency conversion costs. Although gradual, this mechanism will have the potential to expand trade opportunities and could also be used to facilitate capital-account transactions. Invoicing and international trade settlements with oil-exporting countries, or countries with which India has trade deficits, will reduce India’s current account deficit,32 which in turn reduces the burden of maintaining large foreign exchange reserves.

Using the dollar as a foreign policy coercion tool has encouraged countries to look for viable alternatives to minimise the risk. Emerging economies like China and India are trying to make use of this opportunity window. While the dollar’s dominance as a global currency is unlikely to end - given that it’s costly for any country to operate without it - emerging-market currencies will increasingly seek to de-monopolise33 the dollar. It does not, however, threaten the USD’s premier position since local currencies are not fully convertible or freely usable by anyone anywhere.

The International Monetary System currently comprises a handful of currencies that have attained internationalisation - including global currencies such as the US dollar and the Euro - with emerging-market currencies also entering the landscape alongside. The important determinants of currency internationalisation are the economic size, including trade networks, macroeconomic stability and policy support. For this, emerging markets require deeper financial engagement and the liberalisation of the capital account, with internationalisation occurring as a by-product of the reform agenda.

There are many benefits a country would gain from internationalising its currency: the more a currency is used, the more networks it builds, and is typically strengthened, which showcases a nation’s strength in the global system. A country with an internationalised currency benefits from macroeconomic policy autonomy, relatively low borrowing costs and seigniorage revenues, while countries without key currencies operate within the constraints of balance of payment positions34 and bear the costs of adjusting to changing global economic conditions. Seigniorage revenue,35 the revenue a government gains from the status of its currency, is an interest-free loan to the government; at the same time, it lowers the interest cost for the country’s borrowers. It also modulates uncertainty resulting from being able to price exports and imports, and to hold assets and liabilities in the domestic currency.

The Rupee Trade Settlement Mechanism has gained much attention in the last few years, especially with the Reserve Bank of India (RBI)’s scheme of July 2022,36 that comprised a comprehensive framework for permitting rupee settlement for external trade. Under this scheme, the RBI allowed 22 countries to set up Special Vostro Rupee Accounts (SVRAs) to settle payments in local currencies. Indian traders pay in rupees for all imports, which are credited to the Vostro accounts of the corresponding banks of partner countries. Indian exporters are paid from the balances in designated Vostro accounts.

RBI also set up an interdepartmental group (IDG) on the internationalisation of the rupee, and submitted its report in October 2022, recommending a roadmap for the same. The IDG commented37 that “INR has the potential to become an internationalised currency as India is one of the fastest growing countries, and has shown remarkable resilience even in the face of major headwinds.”

However, the internationalisation of a currency is a long pathway ahead for India, as it’s a slow process, and will involve bilateral and multilateral local currency trade settlement mechanisms using the Indian Rupee.

Framework to Analyse the Success of the Rupee Trade Settlement Mechanism

To assess where opportunities lie for India’s Rupee Trade Settlement Mechanism (RTSM), this paper presents a structured framework to evaluate the right conditions under which the RTSM can thrive and be sustainable in the long run.

A 2x2 analytical framework based on two key variables:

Exposure to US Trade uncertainty38 (External Geopolitical Factor) - Determines the extent to which countries are exposed to market uncertainty due to US tariff pressures.

Bilateral trade balance with India (Internal Factor) - Represents how stable, liquid, and reliable the rupee is perceived as a medium for trade settlement.

These two variables were selected because they are both highly important and highly uncertain, making them critical determinants of RTSM success. They are mutually exclusive; meaning that one does not directly determine the other, but they interact meaningfully in shaping trade settlement decisions.

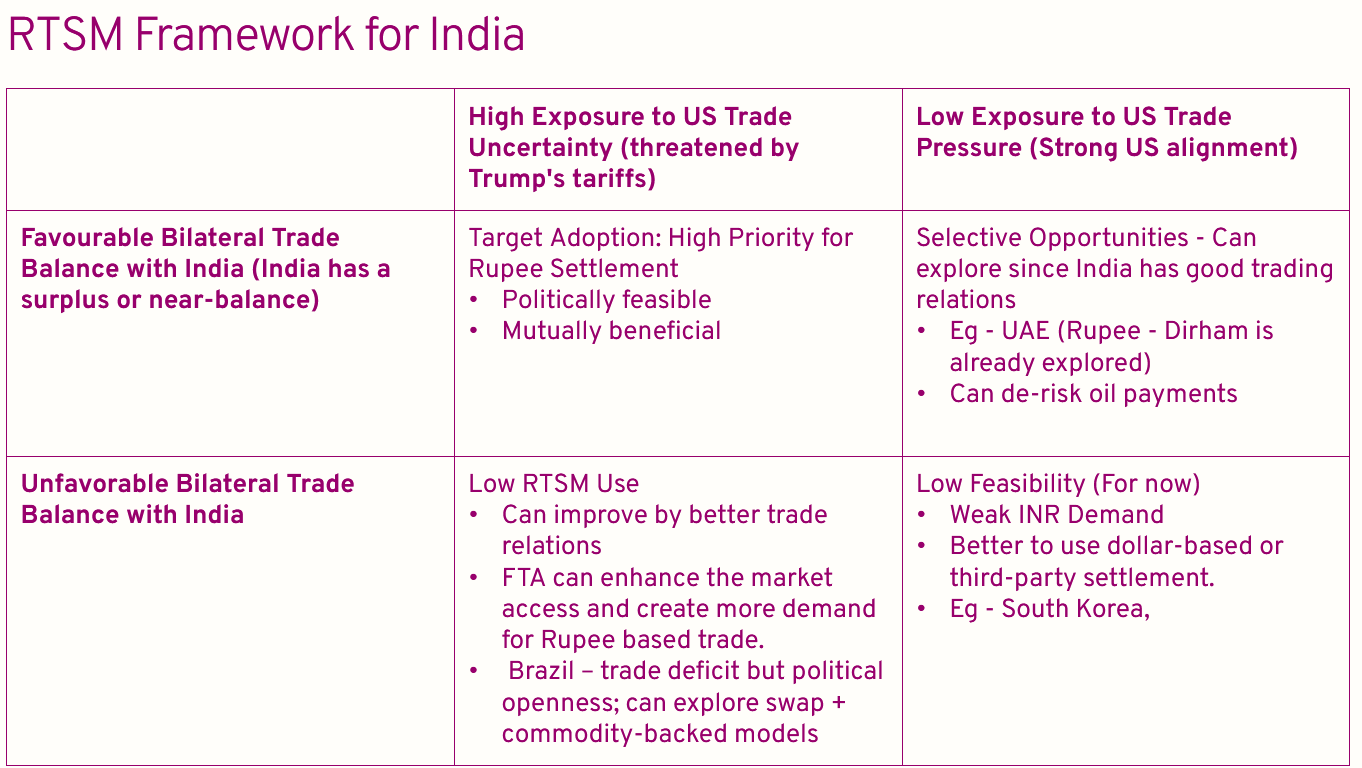

Scenario 1: High Exposure to US Trade Uncertainty, with Higher Favourable Trade with India

This is a scenario where there is an incentive for countries to adopt RTSM, as it is feasible due to the favourable trade volume. However, there are currently very few countries that face strong dollar pressure and with whom India has a favourable bilateral trade balance.

Countries facing strong uncertainty due to US tariffs typically export more to India than they import, creating rupee accumulation risks, while countries with balanced trade face little incentive to exit the dollar system. Turkey is an illustrative example here; it faced US tariffs (e.g. on steel) and holds a substantial India trade surplus (USD 2.7 billion in 2024-25). Such countries have both a motive and a means to use rupee settlements.

Scenario 2: Low Exposure to US Trade Uncertainty; However, Higher Balanced Trade Volume with India

Since there is a significant amount of balanced trade, which signifies the feasibility of the same, the demand might be low, as there is no external geopolitical element pushing for alternatives.

Examples: Bangladesh, Sri Lanka, Nepal, Bhutan. These are India’s neighbours or friendly partners (minimal US trade risk) with large exports to India, making rupee receipts useful. Bangladesh and Sri Lanka, are good options here. In 2023-24, bilateral goods trade between India and Bangladesh was around USD 12.9 billion,39 with India’s surplus around USD 9.3 billion. Sri Lanka also runs a surplus to India (USD 2.69 billion surplus in 2023-24) and is not US-targeted, and indeed has opened rupee Vostro accounts with India. Nepal and Bhutan, though smaller, similarly have India export surpluses and close ties to India.

However, with increased trade uncertainty and de-monopolisation of the dollar, the demand might increase.

Scenario 3: High Exposure to US Trade Uncertainty, with an Unfavourable Trade Balance with India

These partners may want alternatives owing to sanctions or due to trade pressure, but the rupee settlement becomes unstable if the partner cannot deploy accumulated rupee back into Indian goods or assets.

Examples: Russia and other sanctioned states. Russia faces Western sanctions (high US-exposure) and, in 2023, became a major source of imports for India. However, India’s exports to Russia are limited, so rupee usage is constrained. Iran (US oil sanctions) likewise fits: they have strong incentives to avoid the dollar but little bilateral trade to absorb rupees. India imported around USD 61.4 billion from Russia in 2024, and runs a deficit of USD 57 billion. This creates rupee accumulation40 problems on the Russian side, unless India provides reliable utilisation channels.

Scenario 4: Low Exposure to US Trade Uncertainty with Lower Chances of Rupee Absorbability

These countries will have very little reason to exit the US dollar system, and lack rupee usability as India doesn’t have good trading relations with them. Even if India offers an RTSM infrastructure, its feasibility is extremely low.

Examples: Countries like Saudi Arabia and South Korea. They have little incentive to exit the dollar system (strong US ties) and limited ability to recycle rupees (large Indian imports).

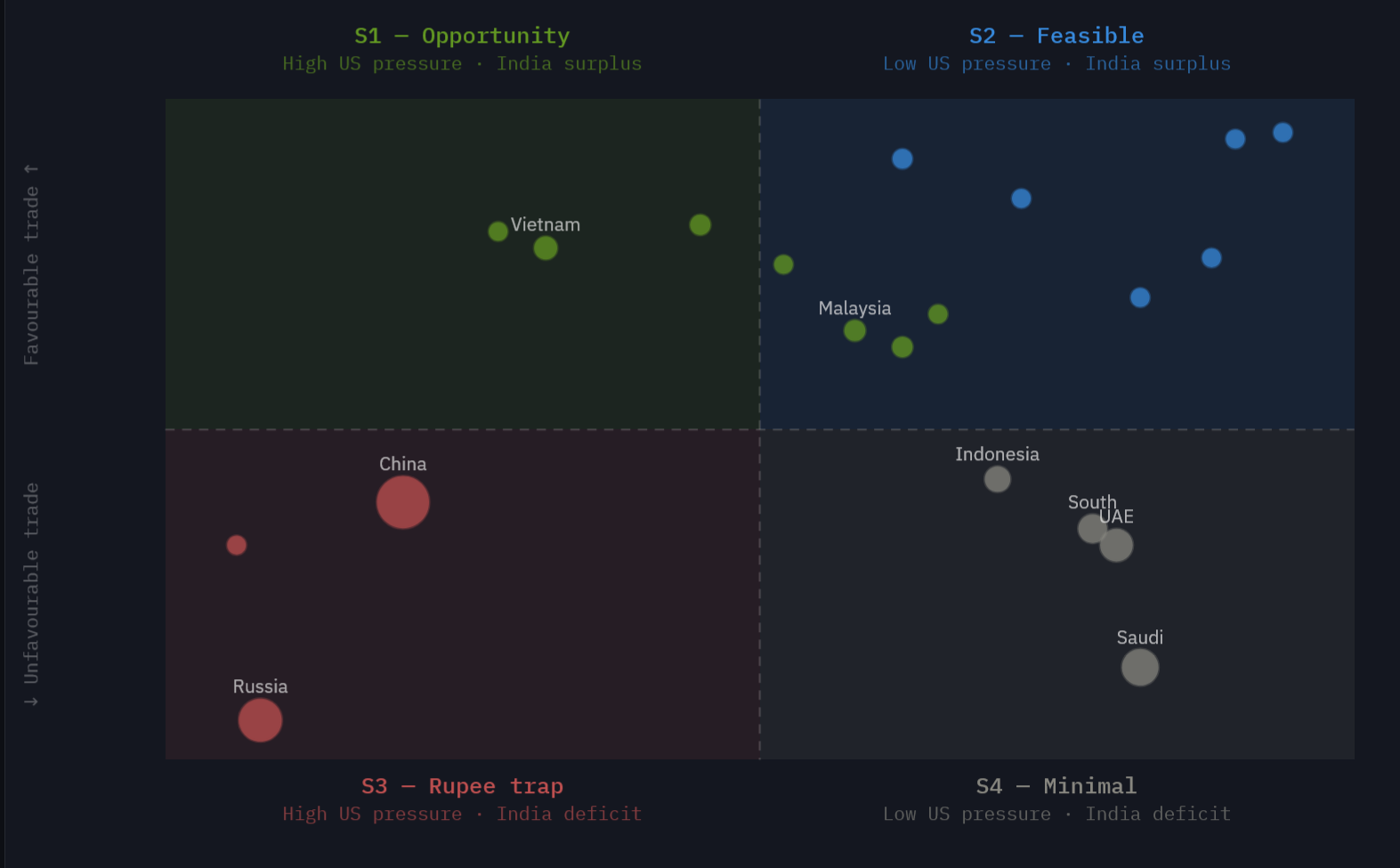

Where Does Opportunity Lie for India?

While the first quadrant is an opportunity option for India, as it has both the demand and supply options. This allows for a Market-Driven Expansion,41 which is the most sustainable, scalable, and beneficial for India’s long-term economic and financial stability. Unlike the scenario where countries are forced into rupee trade due to Western sanctions or trade pressures, market-driven expansion ensures that trade settlement in rupees occurs owing to economic incentives, and not just because of external coercion alone. Scenario 2 is also a great option for India, as India has a favourable trade balance there and India can develop RTSM with those countries, given the current geoeconomic order.

X axis: US trade exposure - left = High US pressure such as tariffs/sanctions, right = Low US pressure. Y-axis: Bilateral trade balance - top = Favourable where India has trade surplus, rupees can circulate, bottom = Unfavourable where India has trade deficit, rupee accumulation risk. Dot size = bilateral trade volume.42

Policy Pathway for a Market-Driven Adoption of RTSM

Transitioning India’s Rupee Trade Settlement Mechanism (RTSM) towards a market-driven expansion necessitates a multifaceted policy approach. This strategy aims to address existing barriers and leverage economic opportunities to enhance the rupee’s role in international trade.

Scenario 2 works only if trade volumes are large enough. India needs to sign FTAs with countries with which it has a trade surplus, such as neighbouring countries.

Even willing firms won’t shift invoicing if they fear INR liquidity shortages during stress. Establishing offshore rupee bond markets - such as Masala Bonds - allows foreign investors to invest in Indian assets without currency exchange risks, thereby increasing rupee liquidity abroad. Expanding bilateral swap agreements with key trading partners ensures the availability of rupees for trade. This increased financial integration can enhance currency stability and acceptance.

India can implement fiscal incentives for exporters who opt for INR invoicing. Tax rebates or reduced GST rates for such transactions would enhance the attractiveness of rupee settlements.

Also, offering preferential forex rates can mitigate exchange rate risks, making rupee invoicing more competitive. These measures align with the principles of export-led growth, where financial incentives stimulate domestic production and international trade.

India must offer smooth trade facilitation through faster customs clearances and smoother logistics handling. If India emerges as a key trading hub, it’s easy to incentivise its trading partners for RTSM.

India should also offer easy exit options if a country doesn’t want to continue conducting its trade through RTSM.

Conclusion

India’s RTSM should be viewed as part of a broader effort to adapt to a more fragmented and uncertain global monetary environment. The rupee is unlikely to replace the dollar, but it does not need to. By pursuing a patient, market-led strategy focused on favourable trade relations, India can reduce external vulnerabilities and expand the rupee’s international role. This paper emphasises the prioritisation of increasing trade density, integrating payment systems, providing liquidity backstops through swap lines, expanding trade finance in rupees, and thereby gradually improving usability.

Footnotes

“Emerging Markets,” World Economics, accessed March 12, 2026. Link.↩︎

Organisation for Economic Co-operation and Development, “Development Centre,” OECD, accessed March 12, 2026. Link.↩︎

World Bank, The Growth Report: Strategies for Sustained Growth and Inclusive Development, (Washington, DC: World Bank, 2008). Link.↩︎

European Parliament, “The International Role of the Euro and the Dollar in a Multipolar World,” ECTI IDA(2025)773690, 2025. Link.↩︎

European Parliament, “The International Role of the Euro and the Dollar in a Multipolar World.” Link.↩︎

Reuters, “Central Banks Favour Gold Over Dollar in Reserves - WGC Survey,” Reuters, June 17, 2025. Link.↩︎

Robert Triffin, Gold and the Dollar Crisis: The Future of Convertibility, (Princeton, NJ: Princeton University Press, 1960). See also: International Economics Section, Princeton University, Essays in International Finance, No. 132. Link.↩︎

Robert Triffin, Gold and the Dollar Crisis: The Future of Convertibility, (Princeton, NJ: Princeton University Press, 1960). See also: International Economics Section, Princeton University, Essays in International Finance, No. 132. Link.↩︎

Federal Reserve Bank of St. Louis, “Monetary Gold Stock, United States,” FRED Economic Data, accessed March 12, 2026. Link.↩︎

Barry Eichengreen, “Hegemonic Stability Theories of the International Monetary System,” in Can Nations Agree? Issues in International Economic Cooperation*, ed. Richard Cooper et al. (Washington, DC: Brookings Institution Press, 1989). Link.↩︎

Central Intelligence Agency, “Iran Sanctions and Reserve Seizures,” CIA Reading Room, accessed March 12, 2026. Link.↩︎

Patrick H. Carleton, “Freezing of Libya’s Assets,” American University International Law Review, (1986). Link.↩︎

Scott R. Anderson, “INSTEX: A Blow to US Sanctions?,” Lawfare Media, 2019. Link.↩︎

FXC Intelligence, “China Cross-Border Transactions, January 2025,” FXC Intelligence, 2025. Link.↩︎

Economic Times, “US Sanctions 6 Indian Firms Over Iran Oil Trade; USD 220 Million in Deals Under Scrutiny,” Economic Times, 2025. Link.↩︎

International Monetary Fund, “IMF Data Brief: Currency Composition of Official Foreign Exchange Reserves (COFER),” IMF, December 2024. Link.↩︎

OECD, Global Debt Report 2025: Sovereign Debt Markets in Emerging Market and Developing Economies, (Paris: OECD, 2025). Link.↩︎

A fiat currency is a type of money that has no intrinsic value but is declared legal tender by a government. Its value is derived from the public’s trust and confidence in the issuing government and the stability of the economy. Unlike currencies backed by a physical commodity like gold, fiat money is not redeemable for anything of intrinsic value.↩︎

Bank for International Settlements, BIS Papers No. 136: Gaining Momentum - Results of the 2021 BIS Survey on Central Bank Digital Currencies, (Basel: BIS, 2022). Link.↩︎

Dennis Ip, “Monetary Hegemony and the Digital Currency Landscape,” Boston University International Law Journal, 42, no. 2 (2024). Link.↩︎

Congressional Research Service, “Section 301 of the Trade Act of 1974: Origin, Evolution, and Use,” CRS Report R45529 (Washington, DC: CRS, 2019). Link.↩︎

SIEPR, Stanford University, “Trump’s Tariffs Lead Investors to Question the Future of the Dollar,” Stanford Institute for Economic Policy Research, 2025. Link.↩︎

Kiuchi Takashi, “The First-Order Impact of US Trade Policy on Global Dollar Supply,” NRI (Nomura Research Institute) Media Journal, June 13, 2025. Link.↩︎

Bank for International Settlements, BIS Triennial Central Bank Survey: Foreign Exchange Turnover in April 2022, (Basel: BIS, 2022). Link.↩︎

Carla Norrlof and Alexandre Kindel, “Dollar Diminished: The Unmaking of US Financial Hegemony Under Trump,” International Organization, (2025). Link.↩︎

Carla Norrlof and Alexandre Kindel, “Dollar Diminished: The Unmaking of US Financial Hegemony Under Trump,” International Organization, (2025). Link.↩︎

Moody’s Ratings, “Moody’s Rating News: United States of America,” Moody’s, May 2025. Link.↩︎

Anupam Manur, “De-Dollarisation,” Takshashila Institution, 2023. Link.↩︎

Georgios Georgiadis, Helge Müller, and Ben Schumann, “Dollar Dominance in Trade Invoicing and Exchange Rate Pass-Through,” Journal of International Economics 135 (2022). Link.↩︎

Export Credit Guarantee Corporation of India, “A Primer on Rupee Trade Settlement Mechanism,” ECGC Research Article, accessed March 12, 2026. Link.↩︎

Ibid.↩︎

Press Information Bureau, “RBI Framework for Invoice Settlement of Imports and Exports in Indian Rupee (INR),” Ministry of Finance, Government of India, July 2022. Link.↩︎

Reserve Bank of India, “Report of the Inter-Departmental Group on Internationalisation of the Indian Rupee,” RBI, October 2022. Link.↩︎

Jongrim Ha, M. Ayhan Kose, and Franziska Ohnsorge, “One-Stop Source: A Global Database of Inflation,” IMF Working Paper WP/24/189 (Washington, DC: International Monetary Fund, 2024). Link.↩︎

Puja Thakur, “India-Bangladesh Trade Flows: Smooth Government-to-Government Relations,” Financial Express, 2024. Link.↩︎

Financial Express, “90 Per Cent of India-Russia Trade in Local Currency Now,” Financial Express, 2024. Link.↩︎

Anisree Suresh, “Rupee Trade Settlement Mechanism Framework: Interactive Dashboard,” accessed March 12, 2026. Link.↩︎