Policy Responses to India’s LPG Supply Crisis

| AUTHOR | Anupam Manur, Anisree Suresh |

| DATE | March 18, 2026 |

| DOCUMENT | Takshashila Report 2026-07. |

| VERSION | Version 1.0, March 2026. |

| CATEGORIES | Economic Policy West Asia Iran |

Executive Summary

India’s Liquid Petroleum Gas (LPG) supply is facing a shortage due to the effective closure of the Strait of Hormuz and disruptions in West Asia. With nearly 60 per cent of India’s LPG demand met through imports and over 90 per cent of those imports routed through the Strait of Hormuz, India faces an unprecedented energy crisis. This situation, compounded by limited domestic production and negligible strategic LPG storage capacity, warrants immediate policy intervention.

The government’s immediate responses have focused on demand prioritisation, supply augmentation, and import diversification. Some of these measures, such as directing refineries to maximise LPG output and imposing booking restrictions, have helped stabilise availability but have also generated second-order effects. These include acute shortages in the commercial sector, rising black-market activity, disruptions in food services, and broader economic spillovers affecting inflation, employment, and small businesses.

In the medium term, diversification of import sources offers partial relief but is constrained by longer routes, higher freight costs, and blending requirements specific to India’s consumption patterns. Internally, pricing and subsidy structures need reform to allow consumer LPG prices to reflect market prices while keeping subsidies via DBT for genuinely vulnerable households.

The long-term solution lies in reducing structural dependence on LPG itself. This requires a transition towards a diversified cooking energy mix, including piped natural gas, electric cooking, and bio-based fuels, alongside investments in strategic reserves.

Why is India Facing an LPG Crisis?

India is facing a Liquid Petroleum Gas (LPG) shortage due to the ongoing crisis in West Asia, which began with US and Israeli strikes against Iran on 28th February, 2026. The conflict in the region has effectively closed the Strait of Hormuz, the narrow chokepoint between Iran, Oman and the UAE, through which 90 per cent of India’s LPG imports pass. India’s LPG shortage amid the current West Asian crisis stems from multiple vulnerabilities in the system. First, while the demand has doubled, 60 per cent of its demand is met by imports. Second, 90 per cent of the imports are routed through the Strait of Hormuz, which adds to the geopolitical vulnerability. Lastly, India has very limited storage capacity for LPG, which would have served as a buffer in times of crisis.

In January 2026 alone, India imported 2.192 million tonnes of LPG and produced 1.158 million tonnes.1 India’s LPG consumption has doubled in the past decade, from about 15 million metric tonnes (MMT) in 2012 to around 31 MMT in 2025. As of January 2026, India has around 332.1 million active domestic LPG connections including 104.29 million subsidised connections under Pradhan Mantri Ujjwala Yojana (PMUY).2 With the introduction of the PMUY, the consumption has doubled. India consumes roughly 2,700 thousand metric tonnes (TMT) of LPG every month, while domestic production contributes only about 1,036 TMT.

Unlike LPG, India’s reliance on crude oil imports through the Strait of Hormuz is only around 40 per cent. For petrol and diesel, India operates 23 crude oil refineries with a total refining capacity of about 248–256 million tonnes per year. These refineries process over 220 million tonnes of crude oil annually, converting imported crude into fuels such as petrol, diesel and aviation fuel within the country. India imports crude from multiple regions rather than relying on a single supplier. Also, crude oil inventories and refinery storage provide a temporary relief as refineries can continue processing stored crude oil. India has roughly 30 million barrels of crude reserves, or 77 per cent of total capacity in its three underground caverns, which is approximately equal to seven days of strategic cover against India’s daily imports of 4.76 million barrels.3 Along with that, the commercial inventories held by Indian Oil, BPCL, and HPCL have reserves of roughly 65 days, reaching a combined national total of 72 days’ worth of strategic reserve. This reduces the geopolitical uncertainties affecting petrol and diesel availability in India.

On the other hand, India’s long-term LPG storage capacity is around 140 TMT.4 India has commissioned two LPG underground rock caverns with a storage capacity of 80 TMT at Mangalore and 60 TMT in Visakhapatnam. When the country consumes roughly 90 TMT of LPG every day, these reserves can only cover two days’ worth of consumption. While refineries and import terminals may have some LPG storage facilities, given that it must be stored under pressure or at very low temperatures, building large storage facilities is far more complex and expensive than storing petrol or diesel. India, therefore, relies more on an LPG system which directly flows from sources to customers, rather than one based on stockpiling.

Effects of the LPG crisis

Inflation Effects

The Union government increased the prices of domestic non-subsidised LPG by Rs 60 (7 per cent increase) and that of commercial LPG by Rs 130 per cylinder (6.5 per cent increase), following the shortages. The RBI had projected 2025-26 to be a non-inflationary year with an optimistic estimation of Headline inflation at 2.1 per cent.

However, due to the effects of the war, the February CPI inflation was at 3.21 per cent, and March CPI numbers might end up in the range of 3.3 per cent to 3.5 per cent.

‘Fuel and Light’ is given a weight of 6.84 per cent in the CPI basket. Assuming a pass-through rate of 30 per cent to 50 per cent, the hike in LPG prices alone can contribute to about a 0.1 to 0.15 per cent increase in CPI. However, taken along with the increase in oil and gas prices, the effect will be much higher. Every USD 10 per barrel increase in average crude prices could raise CPI inflation by 40–60 basis points, assuming a full pass-through into retail fuel prices. Given that Brent crude has increased by about USD 35 to around USD 102, this could potentially raise CPI by about 1.4 to 2.1 per cent. Even if the government orders oil companies to absorb the losses and allows for only a partial breakthrough of 30-40 per cent, CPI could increase by 0.5 to 0.8 percentage points.

Thus, this paper estimates that from a CPI inflation rate of 3.21 per cent in February, the CPI rate could touch 4.2 to 4.5 per cent with the combined effect of oil, gas and LPG in the coming few months. For 2026-27, CPI could remain at elevated levels of 4.5 per cent and above, which is within RBI’s comfortable range of 2 to 6 per cent, but will fundamentally shift the monetary policy outlook from non-inflationary to cautionary.

Further, restaurants and accommodation services carry a weightage of 3.5 per cent in the new (2024) CPI series and given that these sectors are facing an LPG crisis along with a shortage, this will increase prices as well.

Food Services Hit

Restaurants and food services have been severely affected by the LPG shortage, rationing, and price rises. With the government invoking the Essential Commodities Act to allocate natural gas according to its priorities, commercial gas supply has been slashed by about 30-50 per cent.5,6 This has led to a spate of closures of restaurants in big cities and has adversely affected smaller vendors as well.7 Many establishments now operate “half-kitchens,” serving only limited menus that do not require long, high-flame cooking. Functioning restaurants have added a “LPG crisis” premium to the food prices, which further squeezes customers’ pockets.

The closures, hike in prices, and limited menus are bound to turn away customers, which can affect the bottom line of the restaurants, forcing them to lay off temporary, informal workers.

The LPG shortage has hit food delivery apps as well, as restaurants are running limited menus and are prioritising eat-ins over delivery. While the share price of Zomato and Swiggy both fell sharply in the last two weeks, the effect is more dire on gig workers relying on delivery services as their main source of livelihood. Orders on the apps have fallen by 50 - 60 per cent.

Industrial Slowdown and MSMEs Affected

Manufacturing Hits: Industries such as stainless steel (Jindal Stainless), ceramics (Morbi), and glass manufacturing have already scaled back production due to the expected increases in input prices and the LPG shortage. While some MSMEs and industries have shifted to electric heating, small fabrication and foundry units in industrial hubs like Ambattur (Chennai) and Coimbatore are finding it difficult to cope.8

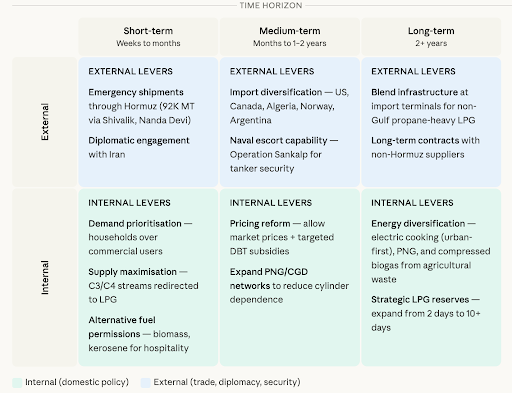

Policy Options

India’s policy options cover the short-term, medium-term, and long-term time horizons. They can also be classified as internal or external facing policy options.

Short-term

Demand Prioritisation

India has taken a series of immediate measures to ease the LPG shortage. Given that around 85–87 per cent of India’s LPG consumption is in the domestic (household) sector, the government has prioritised LPG supplies to households over those to commercial and industrial consumers. However, this has led to a massive fuel shortage for these non-household segments across India.9 The Government of India has also ordered refiners to maximise LPG production, and has made active efforts to diversify its LPG imports. While many of these measures have led to a 17.7 per cent slump in LPG consumption in India in the first half of March 2026, many of the stabilisation measures were only able to improve the situation by a narrow margin.10 While prioritisation of households makes sense as nearly 330 million households use LPG for cooking, it can also have negative consequences for businesses. Nearly 90 per cent of commercial kitchens use LPG for running their business. Some of the bigger commercial kitchens can substitute LPG with electric cookers, but a majority of small and medium establishments will find it hard to endure. Nearly 10,000 establishments were expected to shut down across Tamil Nadu alone.11 Lakhs of small roadside vendors will either have to pay a premium in the black market or shut down.

As expected, a thriving black market has emerged for LPG cylinders, where a domestic gas cylinder is being sold at Rs 2000-3000 per cylinder (as against the listed price of Rs 950), and a commercial cylinder is sold for Rs 6000 (against Rs 1800).12 A 25-day minimum booking gap has been introduced as a demand management measure in urban areas, and a 45-day minimum in rural areas. However, due to panic buying, daily bookings have increased from the average of 55.7 lakh to 88.8 lakh on 14th March 2026.13 Despite the extension in the booking period, India’s virtual demand spiked by nearly 60 per cent. Given that India is facing a 25 to 30 per cent deficit in its LPG supply, this further exacerbates the supply shortage.

Permitting alternative fuel sources for commercial establishments has reduced some dependency on LPG as well. The government allowed commercial kitchens to use biomass, kerosene, and RDF pellets as temporary fuels.

Internal: Supply Prioritisation

The LPG Control Order issued on 8 March 2026 directed all refineries to maximise LPG yields and channel the entire output of C3 and C4 hydrocarbon streams, comprising propane, butane, propylene, and butenes, exclusively to three Oil Marketing Companies - Indian Oil Corporation Ltd (IOCL), Bharat Petroleum Corporation Ltd (BPCL), and Hindustan Petroleum Corporation Ltd (HPCL) for domestic cooking gas. This measure has been claimed to increase domestic LPG production by 25 to 30 per cent, as shown in Table 1.14

External: Continued Diplomatic Engagement with Iran

This is one of India’s most effective short-term levers for the continued safe passage of tankers through the Strait of Hormuz. Emergency shipments, such as Shivalik and Nanda Devi, two Indian-flagged LPG carriers, have crossed the Strait of Hormuz, carrying more than 92,000 metric tonnes of LPG to India since the Strait’s effective closure. However, it is just 5 per cent of India’s monthly imports, barely equivalent to 1-2 days of India’s consumption.

| Category | Amount (TMT) | Notes |

|---|---|---|

| Total Monthly Demand | 2280 | 2700 is the usual monthly consumption in India. However, the consumption fell by 15-16 per cent in March 2026. |

| New Domestic Production | 1295 | 1036 TMT + 25 per cent boost in domestic production. |

| Safe Imports (Non-Hormuz) | 166 | 10 per cent of the normal 1664 TMT import volume |

| Emergency Shipments | 92 | Shivalik and Nanda Devi Cargo Arrivals through the Strait of Hormuz15 |

| Existing Cavern Reserve | 140 | Visakhapatnam has a strategic cavern reserve for LPG (60 TMT capacity)+ another strategic cavern reserve was expected to be operational in Mangaluru by mid 2025 (80 TMT capacity). |

| Total Available Supply | 1693 | Sum of all of the above |

As per the rough estimate in Table 1, if India consumes 76 TMT per day and currently has approximately 1693 TMT in supply, this might provide a supply buffer of 22 days. There are efforts to receive staggered batches of LPG from diverse sources such as the US, Norway, Algeria, and Nigeria, which provide a vital supply of gas to prevent the system from running dry.

Medium-Term

External: Diversification

Indian buyers have begun sourcing LPG cargoes from outside the Middle East, including the US, Canada, Algeria, Norway and Argentina. Contracted imports from the US are expected to provide certain relief. However, this diversification comes with two challenges. The first and foremost concern is the distance, as shipments from the US typically take around 40 days to reach India, whereas shipments from West Asia used to take less than 10 days. This means India’s alternative options remain volatile as these shipments depend on the availability of Very Large Gas Carriers (VLGCs).

Second, India has been relying on West Asian suppliers due to its specific blend requirements for LPG. India imports preblended LPG to meet the country’s butane-heavy requirements, which is largely produced in West Asia. The gas produced in other countries, such as the US, is propane-heavy and requires additional infrastructure at either the exporting or importing terminals to alter the blend as per requirements.16 Currently, this infrastructure is not widely available on either side, which limits the ability of alternative sources to replace the current suppliers on a larger scale. Thus, diversifying to the Atlantic Basin requires finding suppliers willing and able to meet India’s specific demand profile, or India will need to make the necessary infrastructure tweaks at its import terminals.

Internal: Rationalising Pricing and Subsidies in the LPG Market

India employs two primary gas pricing mechanisms: the Administered Price Mechanism (APM) and prices determined by market forces. While the APM was revised during 2023 to better reflect market conditions, it is still a controlled pricing mechanism by the government, which aims to balance consumer and producer needs. According to an estimate by IEA, 64 per cent of India’s domestic gas supply in 2024 was priced as per APM. Additionally, 29 per cent fell under the HP/HT-deepwater price ceiling, and only 7 per cent enjoyed full pricing and marketing freedom.

In reality, the Union Government attempts to control the pricing mechanism a lot more. Between 2020 and 2023, the Union government continued to modulate the effective price to consumers for domestic LPG and paid compensation for under‑recoveries to oil marketing companies rather than let price float freely. A large one‑time compensation of Rs 22,000 crore was paid to OMCs in FY 2022‑23, specifically to cover LPG under‑recoveries, indicating that retail prices were held below economic cost.

In August 2023, for instance, the Union Government announced a Rs 200 cut in LPG prices for all households (on top of PMUY subsidies), and prices were then kept unchanged through 2024-25 despite rising costs. This created sustained under‑recoveries of roughly Rs 41,000 crore that the government planned to cover via a compensation fund.

A 2025 government press release shows that by late 2025, the “effective price” of a cylinder was being held at Rs 853 for regular consumers and Rs 553 for PMUY beneficiaries, even though the economic cost was around Rs 950, again confirming de facto price control through subsidies and administrative modulation rather than a formal statutory cap.17

These forms of price control distort the market signals that would automatically encourage conservation and rationalisation of use. When LPG is artificially cheap, there is no incentive for households to economise, such as using shorter cooking times, batch meals, or considering induction cooktops.

Second, it creates a massive fiscal burden. The Rs 30,000+ crore in compensation to oil companies is money that could fund PNG infrastructure or renewable cooking alternatives. Third, it encourages diversion and black-marketing. When the subsidised domestic cylinder is far cheaper than the commercial one, there is a strong incentive to divert domestic cylinders to commercial use.

The reform proposal would be two-fold: Allow consumer LPG prices to reflect market prices, while keeping the subsidies via DBT for the genuinely vulnerable households. This would mean that the price of LPG would rise during shortages even for subsidised households, such that there is a better signalling mechanism. Simultaneously, set a limit to the number of subsidised cylinders that a household can receive - e.g., 10 cylinders, after which prices float to the market prices.

Long-Term

Internal: A Diversification Strategy

A country of India’s size cannot find itself excessively reliant, for its cooking needs, on a single imported fuel passing through a single strategic chokepoint. India needs to diversify its energy sources for household cooking. Readying India’s cities for better piped natural gas (PNG) delivery has to be a policy priority. The gas in PNG is also imported, but it is less vulnerable than LPG for a few reasons. First, India’s domestic production of natural gas is much better - out of India’s current requirement of 189 MMSCMD (million metric standard cubic metres per day), 97.5 MMSCMD is produced domestically.18 Second, of the 48 per cent imported, the source diversification is much better. Qatar is the dominant Gulf supplier, but India also has long-term LNG contracts with the US, Australia, and others that do not transit Hormuz.

Further, the government has already mandated Compressed BioGas blending into the City Gas Distribution network (1 per cent in FY26, rising to 4 per cent by FY28). This can be further increased in the long run. India has massive agricultural waste feedstock. This is a genuinely domestic, renewable cooking fuel source that complements electric and PNG.

The more significant diversification strategy has to be electric, especially in urban areas, for the economically better-off. The economics of electric cooktops are compelling in terms of cost savings, energy efficiency, and resilience. For a family of four, electric cooking was estimated to be 37 per cent cheaper than non-subsidised LPG and 14 per cent cheaper than piped natural gas in FY2024-25. A gas burner can lose close to 60 per cent of its heat to the surrounding air, so only about 40 per cent of the energy you pay for actually goes into cooking, while an induction hob can use around 90 per cent efficiently. To deliver the same useful heat as a single LPG cylinder, an induction stove would consume roughly 78 units of electricity. Even at a relatively high household tariff of Rs 8 per unit, this comes to about Rs 624, implying potential monthly savings of nearly Rs 300 compared with LPG.

More importantly, electricity is generated domestically. India’s grid runs primarily on domestic coal, and increasingly on domestic solar and wind and therefore has neither import dependence nor forex outflow. The big problem with electricity, however, is reliable, continuous, good-quality power, which is absent in large parts of India, especially in rural areas. Lack of reliable power supply, fluctuations and outages, peak demand problems, and even cultural and culinary habits would mean that electric cooking cannot fully replace gas.

Therefore, this paper recommends that urban Indian households have electric cooktops as the primary source, with LPG/PNG as a secondary backstop option. From a policy perspective, continuing electrification of rural areas and working on grid reliability and capacity remain paramount. Encouraging rooftop solar and redirecting a part of the gas subsidy to rooftop + electric hardware would make the switch easier.

Increasing India’s Strategic Gas Reserves

India has recently decided to have strategic LPG reserves with the commissioning of the HPCL Mangalore cavern in late 2025, alongside the existing Visakhapatnam facility, India now has roughly 140 TMT of deep-storage LPG capacity.19 These storage facilities account for less than two days of consumption. LPG reserves are technologically complex and expensive as they require specialised high-pressure or cryogenic storage. It cost Rs 854 crore to build the 80 TMT LPG cavern in Mangalore. Given India’s cooking fuel may be dominated by LPG for a while and its high import dependence, ideally India needs a minimum 10 days strategic gas reserve, with a cost of around Rs 9607.5 crore.

Conclusion

India’s success in expanding LPG coverage has created a system that is efficient under normal conditions but vulnerable under stress. The government’s prioritisation of households over the commercial sector has inevitably redistributed scarcity within the system. While the immediate policies need to be prioritised to mitigate the situation, this also offers an opportunity to rethink India’s energy consumption. Medium-term strategies such as import diversification and infrastructure upgrades may improve flexibility. However, the deeper lesson from the crisis is that, as a long-term strategy, a gradual but deliberate shift towards a more diversified fuel mix, combining LPG with electricity, piped gas, and biofuels, can mitigate these risks in the future. At the same time, expanding strategic storage and improving domestic infrastructure can provide critical buffers during future disruptions.

Footnotes

“India LPG Shortage: West Asia War and Hormuz Shipping Disruption,” Business Standard, March 11, 2026.↩︎

Petroleum Planning and Analysis Cell (PPAC), Ministry of Petroleum and Natural Gas, Government of India, accessed March 18, 2026.↩︎

Aditya Sinha and Navin Vijay, “The Strategic Petroleum Reserve Question,” The Sunday Guardian, February 11, 2023.↩︎

“About Us,” Indian Strategic Petroleum Reserves Limited (ISPRL), Ministry of Petroleum and Natural Gas, Government of India, accessed March 18, 2026.↩︎

“Explained: The Essential Commodities Act and its Relevance in the 2026 Energy Crisis,” The Indian Express, March 12, 2026.↩︎

Somit Sen, “LPG shortage: 20% commercial piped gas cut hits hotels, food chains in Mumbai,” The Times of India, March 15, 2026.↩︎

Aadrika Sominder and Deep Saxena, “LPG shortage across restaurants and street vendors in India: Entrepreneurs struggle to keep restaurants running,” Hindustan Times, March 11, 2026↩︎

Sanal Sudevan, “Industries shift to electrical heating amid LPG shortage,” The New Indian Express, March 16, 2026↩︎

Ashwin BM, “LPG crisis: Hoteliers say 25 eateries shut in Bengaluru; more may close if supply isn’t restored in 2 days,” Deccan Herald, March 15, 2026.↩︎

Press Trust of India, “LPG consumption slumps 17% in March on war-related shortages,” The Economic Times, March 17, 2026.↩︎

“Iran War LPG Disruption Hits India Restaurants,” CNBC, March 10, 2026.↩︎

Pushkar V, “Commercial LPG cylinder price in Bengaluru climbs to Rs 6,000 on black market,” Deccan Herald, March 11, 2026.↩︎

Press Information Bureau, “Inter-Ministerial Briefing on Recent Developments in West Asia: Citizens requested to avoid panic bookings of LPG Cylinders,” Ministry of Petroleum & Natural Gas, Government of India, March 14, 2026.↩︎

Hardeep Singh Puri, “Statement by Union Minister for Petroleum and Natural Gas Shri Hardeep Singh Puri in Parliament on Measures Taken to Address Global Energy Supply Disruptions Arising from the Conflict in West Asia,” Press Information Bureau, Ministry of Petroleum & Natural Gas, Government of India, March 12, 2026.↩︎

Saptaparno Ghosh and M. Kalyanaraman, “Two Indian vessels carrying LPG cross Strait of Hormuz safely: Shipping Ministry official,” The Hindu, March 14, 2026.↩︎

Nisha Manav, “Caught in crossfire: India faces LPG supply crunch,” Maritime Research Opinions, Drewry Shipping Consultants Limited, March 16, 2026.↩︎

Upstox News Desk, “Govt likely to compensate oil retailers for LPG losses, may use excise duty gains,” Upstox, July 10, 2025 (Updated March 17, 2026).↩︎

Press Information Bureau, “Government’s highest priority is to ensure uninterrupted Domestic LPG supply; Domestic LPG production increases by about 31%,” Ministry of Petroleum & Natural Gas, Government of India, March 14, 2026.↩︎

Standing Committee on Petroleum & Natural Gas (2024-25), Eighteenth Lok Sabha, Ministry of Petroleum & Natural Gas: Demands for Grants 2025-26, Second Report New Delhi: Lok Sabha Secretariat, March 2025.↩︎