EU ReArm’s Arms, Legs and Nerves

| AUTHOR | Anushka Saxena |

| DATE | February 23, 2026 |

| CATEGORIES | Defence |

The success of the 2030 European rearmament plan depends on the fiscal and political decisions made by participating Member States. Particularly, decisions made in the political corridors of Berlin and Warsaw will likely result as critical drivers of land power on the continent.

Germany’s “Zeitenwende” has evolved from a reactive 2022 announcement into a sustained, long-term modernisation programme. On November 28, 2025, the German Bundestag approved a consolidated defence budget of €108.2 billion for FY 2026, which includes the regular Einzelplan 14 and the dedicated Special Fund (Sondervermögen).

In the German federal budget, Einzenplan refers to the defence budget, which includes the financing of the German Armed Forces and the Federal Ministry of Defense (BMVg). It is one of the largest departments in Berlin, and includes expenditures for personnel, operations, procurement, and research & development.

This funding is directed toward making the German Bundeswehr (armed forces) the “strongest conventional army in Europe,” with massive investments in heavy armour, integrated air and missile defence (IAMD), and cyber capabilities. A critical legislative milestone is the “Bundeswehr Planning and Procurement Acceleration Act” (BwPBBG), which aims to reduce the bureaucratic delays that have historically plagued German military acquisition.

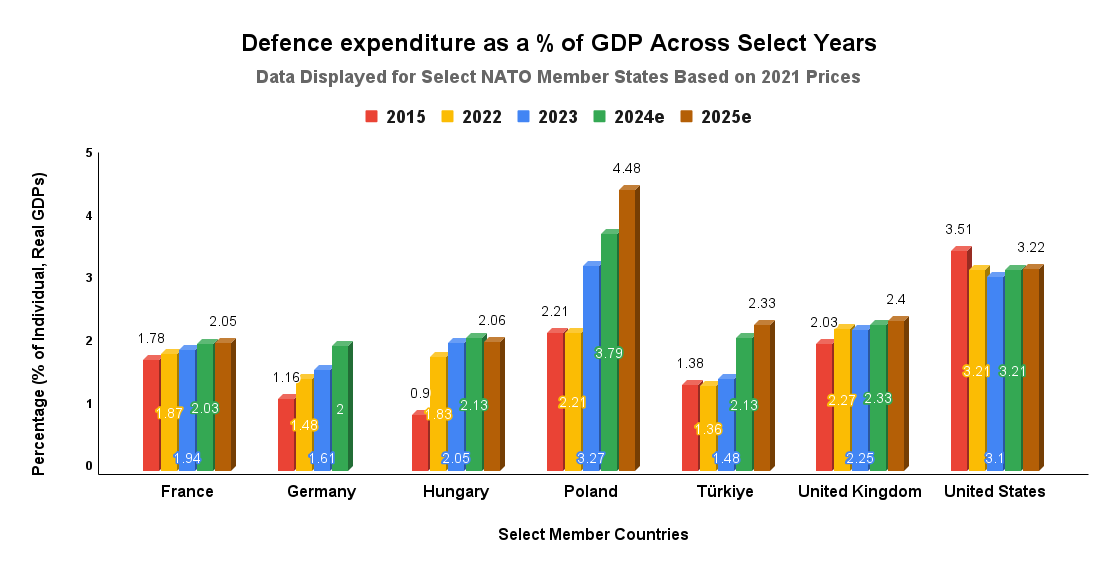

Poland, meanwhile, has emerged as the alliance’s eastern military hub, with a defence budget reaching 4.7% of GDP in 2025 (see Figure) and a target of 5% by 2026. Warsaw’s strategy is characterised by an unprecedented scale of procurement outside of traditional European channels, most notably through massive contracts with South Korea for K2 tanks and K9 howitzers. Poland’s “East Shield” (Tarcza Wschód) project, a €2.6 billion initiative to fortify the border with Russia and Belarus, represents its commitment to rearmament. For fulfilling such requirements, Warsaw has also received the largest allocation of SAFE financing among EU member states.

Poland’s massive buildup is likely creating a new power pole in Europe, as the country’s land forces are projected to surpass those of Germany, France, and the UK combined by 2030. However, this rapid expansion relies heavily on debt and EU financing, including through an additional Armed Forces Support Fund, an extra-budgetary mechanism established to enable quick and massive procurement outside of standard fiscal constraints.

Further, even though rearmament and an increased defence spending themselves may be supported by Poles, they do not necessarily wish to actively engage in warfighting, as evidenced by declining support for conscription, especially among younger populations.

As per a survey conducted by Security Radar (a vertical of the German Friedrich Ebert Stiftung foundation) in 2025, 75% of the surveyed Polish population supports higher defence spending by the government. At the same time, a survey by the Polish newspaper Rzeczpospolita reveals that less than 40% of the surveyed Polish population supports mandatory conscription. The sentiment of opposition is especially high among groups that are highly likely to be called up, such as individuals in their 30s (59%) and Generation Z (58%).

EU ReArm is not without challenges, and must look to India as a reliable defence partner to offset member states’ unique hindrances, and their many divergences.