Takshashila Working Paper - Dominant Economic Narratives in the Post-Pandemic World

This working paper was presented by Anupam Manur at the Takshashila Conference on Understanding the Post-Pandemic World held on February 8, 2023.

A. Introduction

Narratives can be powerful in determining human actions. In economics, the deterministic role of narratives is under-researched and inadequately studied. Narratives are ultimately stories – a story or an account of series of related events or experiences, whether it is true or fictitious.

The narratives that people engage in – either by word of mouth, through the media or increasingly, through the social media – can affect economic outcomes. Whether fact or fiction, stories that people tell influence our decision-making in our daily economic lives – how much to buy, where to invest or whether to save, and when aggregated, narratives can change the course of the economy. This is the premise of Robert Shiller’s book on Narrative economics. Shiller argues that the understanding of economic narratives and how they change has the potential to improve our ability to “predict, prepare for, and lessen the damage of financial crises, recessions, depressions, and other major economic events” (Shiller 2019).

The idea of self-fulfilling prophesies, which are a strong manifestation of the power of narratives, is quite common in economics. It occurs when the adoption of a particular belief by enough people in the society leads to the belief becoming a reality. Asset bubbles are based on a mass belief in the story that the price of the particular asset – whether tulips or real estate or tech stocks – will always go up. On the other end, recessions can also be a self-fulfilling prophesy, as it is playing out in the United States in 2022-23. John Maynard Keynes’s animal spirits, or the emotional decision making in the economic realm, are ultimately driven by narratives.

However, narratives are also subject to feedback loops. They are as much shaped by the world and the economy as they shape it in turn. Stories about economic collapse are not born in a vacuum, nor do they gain traction when all the economic indicators are pointing in the right direction. Narratives might not be the causal factors behind business cycles, but can catalyse, aggravate, and exacerbate economic swings.

The world is changing, as it always does. The narratives at play in 2023 is very different from a decade and a half back. The events in this time horizon – the great recession, eurozone debt crisis, the rise of authoritarian governments, Brexit, the pandemic and finally, the Russia-Ukraine war – all have a bearing on the current narratives in circulation. Understanding these narratives can help us make sense of and predict the economic pathways.

In this essay, we will look at some of the dominant narratives of the day in the context of the international world order. A couple of points to note early on – these narratives may or may not be translated into policy actions or at least not a comprehensive policy. Even if it translates to a policy, there’s no comment here about its effectiveness. For instance, despite the strengthening narrative of deglobalisation and retreating trade, trade between the US and China has not decreased rapidly nor have companies been in a rush to move out of China. It has resulted in some policy moves though.

B. Impeded Globalisation

We now find ourselves in a world-order that can be described as “impeded-globalisation” or “slowbalisation” or “deglobalisation”. Before we look at the narratives or even predictions of what is to come, here’s a look at trade openness in the world up to 2021.

Source: (Irwin 2022)

Globalisation is captured by the trade openness index, which is defined as the “sum of world exports and imports divided by world GDP”. It shows the relative importance of global trade in the global economy and as the chart shows, this has declined slightly after the 2008 financial crisis. The data here doesn’t show the effects of the Russia-Ukraine war, but the probability of a further decline is rather high.

While global trade has generally grown higher than global output in the past few decades, that is no longer the case now. While global output was relatively steady, global trade has been weak, even before the effects of the pandemic.

In absolute terms as well, global trade declined significantly in 2020 when the pandemic hit, recovered thereafter and slumped again in 2022 close to decadal averages. “This severe downturn was the result of international trade being negatively affected by not only the generalized decline in global demand but also enhanced cross-border restrictions and port closures and other logistical disruptions” (UNCTAD 2022).

Source: (UNCTAD 2022)

Looking at data compiled by World Data Monitor on goods imports volume, which is a good proxy for internationally contestable market access, reaffirms the story of shrinking trade. The measure of market access in the years before the financial crisis grew at 4.5-5% for industrialised economies and 12% in emerging markets. The number reduces to 1.5-2% and 4% respectively in the years 2011-19 (2022).

There are several compounding factors that can explain the relative decline in global trade. Some of these are structural reasons, such as China rebalancing its economy to reduce dependence on exports, and the weakened supply chains due to the pandemic-related lockdowns and the war. Some of it, however, can be attributed to the shifting dominant narratives. The United States, under President Trump, kickstarted the global trade war by embracing the “America First” paradigm and the world reacted. Tariffs were raised, rules of multi-lateral organisations were broken, export bans introduced, and a clear preference for economic decoupling from other countries and the need for “strategic autonomy”. In the rest of this section, we will explore some of these themes.

In terms of narratives as well, the term deglobalisation is gaining traction. “In the four years before the pandemic, the Factiva database records on average 850 media mentions of the term deglobalisation. Since 2020 deglobalisation has been mentioned on average 4,534 times per year—from 1 January 2022 to 20 November 2022 this term has been referred to 7,323 times in media outlets around the world” (Evenett 2022).

1. Increased protectionism

Amongst Trump’s many rhetorical campaign promises, putting America First was the agenda item that unfortunately got translated into policy action. In policy terms, this meant putting up trade barriers – increasing tariffs and quotas and increasing non-tariff barriers. Increased tariff by the US on steel and aluminium imports to rectify China’s export dominance and dumping snowballed into a global trade war.

The initial round of anti-dumping duties, tariffs and retaliatory action soon became outright protectionist policies, as the United States and India launched Make in America and Make in India respectively (other countries have their own versions). These protectionist policies typically included increased tariffs, subsidies to domestic industries, export subsidies, tougher licensing requirements, and various non-tariff measures. In India and the US, this was largely justified using the standard arguments of protecting/encouraging domestic industry, protecting jobs, and even countering China.

Other narratives that underscore the protectionist tendencies is the campaigns by policy makers beseeching their citizens to buy local products, as against imported goods. This is a soft mechanism to get consumers to pay higher for goods, which are manufactured domestically by appealing to their patriotism/nationalism/regional affiliations. “Vocal for Local” was a popular slogan in India that ties in with the “Make in India” campaign. Iterations of these were found across the world in the latter half of 2010s.

In the quest for making locally and protecting domestic producers, consumer interests have taken a backseat. There’s a visible increase in prices of electronic products after the levying of tariffs on electronic imports. This is justified as the consumer sacrifice for enabling self-sufficiency.

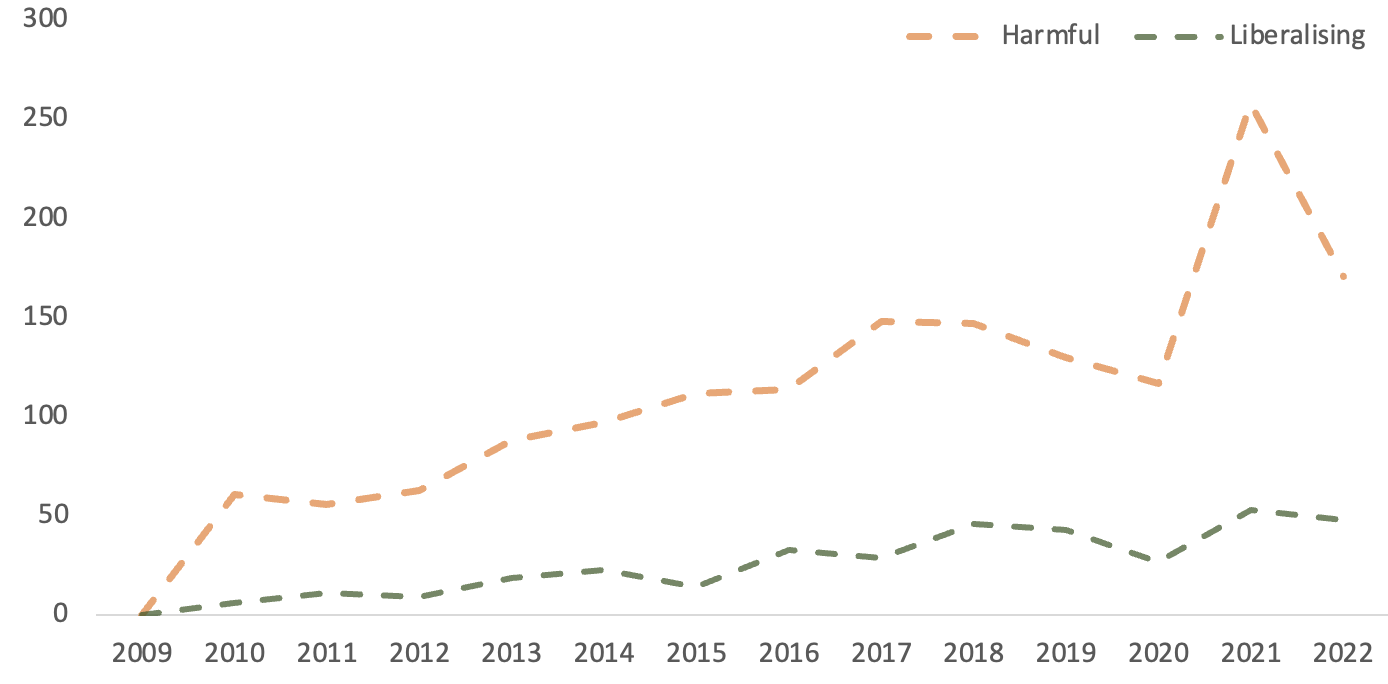

As the chart below shows, there’s a steady increase in the number of harmful interventions in trade in the world since 2009. The huge spike in 2021 is pandemic related.

Figure 3: Number of Harmful and liberalising trade interventions (World)

Source: Chart prepared by author based on data by Global Trade Alert

Figure 4: Not all countries are equally culpable. The US and India had the highest number of harmful trade interventions.

According to the Global Trade Alert, nearly 15 per cent of the total trade protectionist measures implemented at the global level directly or indirectly impact India’s merchandise trade.

In the case of India, import measures have been undertaken either with the objective to promote government’s flagship ‘Make in India’ program or address the issue of inverted duty structure prevalent in certain sectors (such as electronics). Other measures were in response to the dumping practices adopted by trade partners.

Text and chart source: RBI Bulletin (2020)

2. Global Supply Chains Resilience and Strategic Autonomy

The pandemic saw many factories staying idle due to local lockdown measures and staff shortages, while shipping containers stood still or moved slowly due to cross-border restrictions, port closures and other logistical disruptions. The global production model based on efficiency optimisation models of distant suppliers operating on a “just-in-time” delivery model seemed inadequate to deal with the new challenges posed by the pandemic and subsequently, the war. The reliance on foreign suppliers for life-saving material, such as masks and sanitisers, ventilators, production equipment, and even drugs suddenly seemed like a terrible setup. According to the Essential Goods Monitoring Initiative, by mid-April 2020 a total of 71 customs territories had imposed some type of export control on medical goods.

The threat of weaponization of trade further strengthened the arguments for self-sufficiency. Noting the resort to export bans at the onset of the COVID-19 pandemic, prior attempts to limit the export of Rare Earth minerals, as well as the use of bilateral trade measures to show disapproval of the foreign policy and other stances of foreign governments have made policy makers to look at globalisation with increased suspicion.

Export controls on food items that led to soaring global food prices gave further credence to the narrative of developing self-sufficiency and decreased economic dependence. Russia’s five month-long blockade of shipments of Ukrainian grain through the Black Sea is a case in point. Since the invasion of Ukraine, 171 measures to restrict, discourage, or ban food exports have been implemented worldwide (Evenett 2022).

The focus shifted from efficiency in production models to resilience, especially backed by friendly government policies. The push to bring supply-chains or large parts of it to domestic shores in the name of resilience is accelerating. India’s PM called for Atmanirbhartha or self-reliance. “Japan’s covid-19 stimulus includes subsidies for firms that repatriate factories; European Union officials talk of ‘strategic autonomy’ and are creating a fund to buy stakes in firms. America is urging Intel to build plants at home” (The Economist 2020).

Contractor (2022)sees 4 ways in which the supply chain resilience is likely to develop, all of which represent an increase in cost per unit:

“(1) an increase in the number of suppliers for the same component or item (or lower likelihood of reliance on one sole-source foreign supplier),

(2) geographical diversification of supply sources to more than one country,

(3) propinquity of supply sources, in terms of both geographical and political “distance”, and

(4) Increase in inventory levels at the point of use”

The narrative is best summed up by Rana Foroohar: “Countries now want more redundancy in their supply chains for crucial products such as microchips, energy, and rare earth minerals... All these shifts suggest that regionalization will soon replace globalization as the reigning economic order. Place has always mattered, but it will matter more in the future… Counting on autocratic governments for crucial supplies was always a bad idea. Expecting countries with wildly different political economies to abide by a single trade regime was naïve” (Foroohar 2022, 141, 145).

However, wanting to decouple from the world or increase self-sufficiency does not happen on its own. Enter industrial policy.

3. The Return of Industrial Policy

How can governments ensure that companies will produce at home instead of importing from elsewhere? The reasons for importing in the first place were that it was expensive to manufacture locally (either because of high cost of labour or land or some raw material or poor infrastructure & business environment, etc). Governments went about attempting to make it more attractive for firms to produce domestically by getting Johnny Q taxpayer to foot the bill. The Biden administration, for instance, has run with the “Make in America” campaign by building an intricate subsidy program with even local content sourcing rules. The US is spending $465 billion on building semiconductor chips at home and developing climate technology. In response, China might double down on its subside programme.

Other countries do not want to be left behind. South Korea is offering domestic car manufacturers subsidies for electric vehicle manufacturing. The Japanese government has committed $500 million in funding for semi-conductor research. European politicians are waiting to rewrite some of the EU’s rules to expand federal funding for domestic industries.

India has launched a Performance-Linked Incentive scheme, which is a rebranded version of the classical import-substitution + export incentives scheme, replete with local content sourcing requirements.

4. Friend-shoring

“Friend-shoring is another idea that has entered trade policy zeitgeist. At its core, friend-shoring seeks to reallocate production and sourcing away from unreliable, geopolitical rivals towards allies thought less likely to cut off sought-after raw materials, parts, and technology” (Harput 2022). In a speech delivered by Janet Yellen, US Secretary of the Treasury, the emphasis is on friend-shoring: “Working with allies and partners through ‘friend-shoring’ is an important element of strengthening economic resilience while sustaining the dynamism and productivity growth that comes with economic integration. Friend-shoring is about deepening relationships and diversifying our supply chains with a greater number of trusted trading partners to lower risks for our economy and theirs.”

India wants to be one of the destinations for friend-shoring and is attempting to attract American businesses moving out of China into India, with the promise of mitigating the geopolitical risk.

5. The Decline of the WTO

Since 1995, the WTO oversaw the biggest expansion of international trade. However, in the space of a few years, the organisation has become nearly toothless and global confidence in the machinery is waning. The financial crisis of 2008, the rise of autarkic nationalism, China's challenge to the hegemony of American power, and finally the weakening of supply chains caused by the Covid-19 pandemic have all questioned the virtues of globalization, threatening the WTO with obsolescence (Le Monde 2022).

Whether it was Trump’s selective raising of tariffs or Biden’s industrial policy, the US is in clear violation of an organisation that it has helped nurture over the years. Given that some of the clearest violations of WTO rules are done by the most powerful player in that ecosystem, the confidence of the rest of the world in the ability of the WTO to oversee a smooth return to a rules-based global trading order is weakening.

6. Ballooning debt

The unprecedented nature of the pandemic and the forced deep recessions in many countries through lockdowns required an equally unprecedented level of government action to recover. Expansive fiscal action taken during the pandemic to save lives and to save livelihoods did not take into account budget constraints. Even traditional fiscal hawks supported an expansionary fiscal policy. Debt ballooned. In 2020, total global debt rose by 30 percentage points of GDP, to 263 percent of GDP—the largest single-year increase since at least 1970

Source: (IMF 2022)

“This increase was broad-based, evident across government and private debt, domestic and external debt, and the majority of countries. In EMDEs, total debt went over 200 percent of GDP, and in advanced economies, total debt exceeded 300 percent of GDP in 2020”. (Kose, et al. 2021). Emerging markets which had weaker macroeconomic fundamentals have borrowed heavily and debt crises have begun to spring up – Sri Lanka and Pakistan, for instance.

7. Renewed interest in concentration of economic power

The consumer welfare standard that was at the heart of competition policy across the world since the 1970s has now been superseded by other concerns – strategic, nationalistic, and the prevention of concentration of market power. The earlier idea was that market dominance is not necessarily bad in and of itself and therefore did not require government intervention. However, using that dominance to cause harm was seen as justification for government/regulator intervention.

In the information age, however, the narrative has changed to cutting the size of big-tech companies and reducing their market power with or without clear evidence of harm. Regulators across the world are hounding big tech companies purely for their size and dominance. The narrative against big tech firms are usually around these lines:

By their size, dominance, deep pockets and the existence of network effects, they are a threat to smaller players in the market. These can also act as barriers to entry.

They play a gatekeep function and thus have disproportionate power and influence. They get to pick winners and losers based on opaque algorithms

They have disproportionate influence on the political system and their ability to shape the discourse

There’s an element of nationalism here as well – foreign big tech firms versus local small shops narrative.

C. Conclusion

The world order, which was under a gradual change after the 2008 financial crisis, has catapulted into a new shape after two epochal events – the pandemic and the Russia-Ukraine war. Given the rapid expansion of trade, easy capital flows across the world, and relatively easier movement of people in the 2000s, one could be forgiven for assuming that a liberal, rules-based order and globalisation were here to stay.

The dominant narrative now, even in countries which were prominent proponents of free trade in the past couple of decades, is that of self-sufficiency and self-reliance, decoupling, supply chain resilience, and import substitution.

This forces the question whether economic narratives have taken a backseat? In the grand scheme of things, the dominant narratives that shape policy tends to be that of security and culture/race/religion than economic narratives.

D. References

Shiller, Robert. 2019. Narrative Economics: How Stories Go Viral and Drive Major Economic Events. Princeton University Press.

Irwin, Douglas A. 2022. Globalization is in retreat for the first time since the Second World War. October 28. Accessed February 6, 2023. https://www.piie.com/research/piie-charts/globalization-retreat-first-time-second-world-war.

UNCTAD. 2022. Impact of the COVID-19 Pandemic on Trade and Development: Lessons Learned. Geneva: United Nations.

Evenett, Simon J. 2022. What Endgame for the Deglobalisation Narrative? Global Trade Alert.

Reserve Bank of India. 2020. "Efficacy of Import Measures: An Analysis of Select Commodities." RBI Bulletin.

CPB Netherlands Bureau for Economic Policy Analysis. 2022. World Trade Monitor. July. Accessed January 2023. https://www.cpb.nl/en/world-trade-monitor-july-2022.

The Economist. 2020. "Has covid-19 killed globalisation?" The Economist, May 14.

Foroohar, Rana. 2022. Homecoming: The Path to Prosperity in a Post-Global World. Crown Publishers.

Harput, Halit. 2022. Will Friend-Shoring Deliver? Zeitgeist Series Briefing#3, Global Trade Alert.

Contractor, F.J. 2022. "The world economy will need even more globalization in the post-pandemic 2021 decade." Journal of International Business Studies 53: 156–171.

Le Monde. 2022. "The decline of the WTO, a threat to global stability." December 28.

Author: